Fiscal consolidation in PNG: revenue woes

By Alyssa Leng and Kingtau Mambon

17 March 2023

PNG’s 2023 budget is optimistic on the revenue front – by 2027 nominal revenue is expected to be over 40% higher than current levels, and the budget back in the black.

The past decade however paints a gloomier picture. Annual government revenue has oscillated around K10-11 billion (in 2013 prices) for most of the last decade, with revenue from key domestic taxes falling in real terms. Given PNG’s struggle to control expenditure, which we have written about in a companion blog, fiscal consolidation seems out of reach without better economic conditions and higher tax revenues as a result.

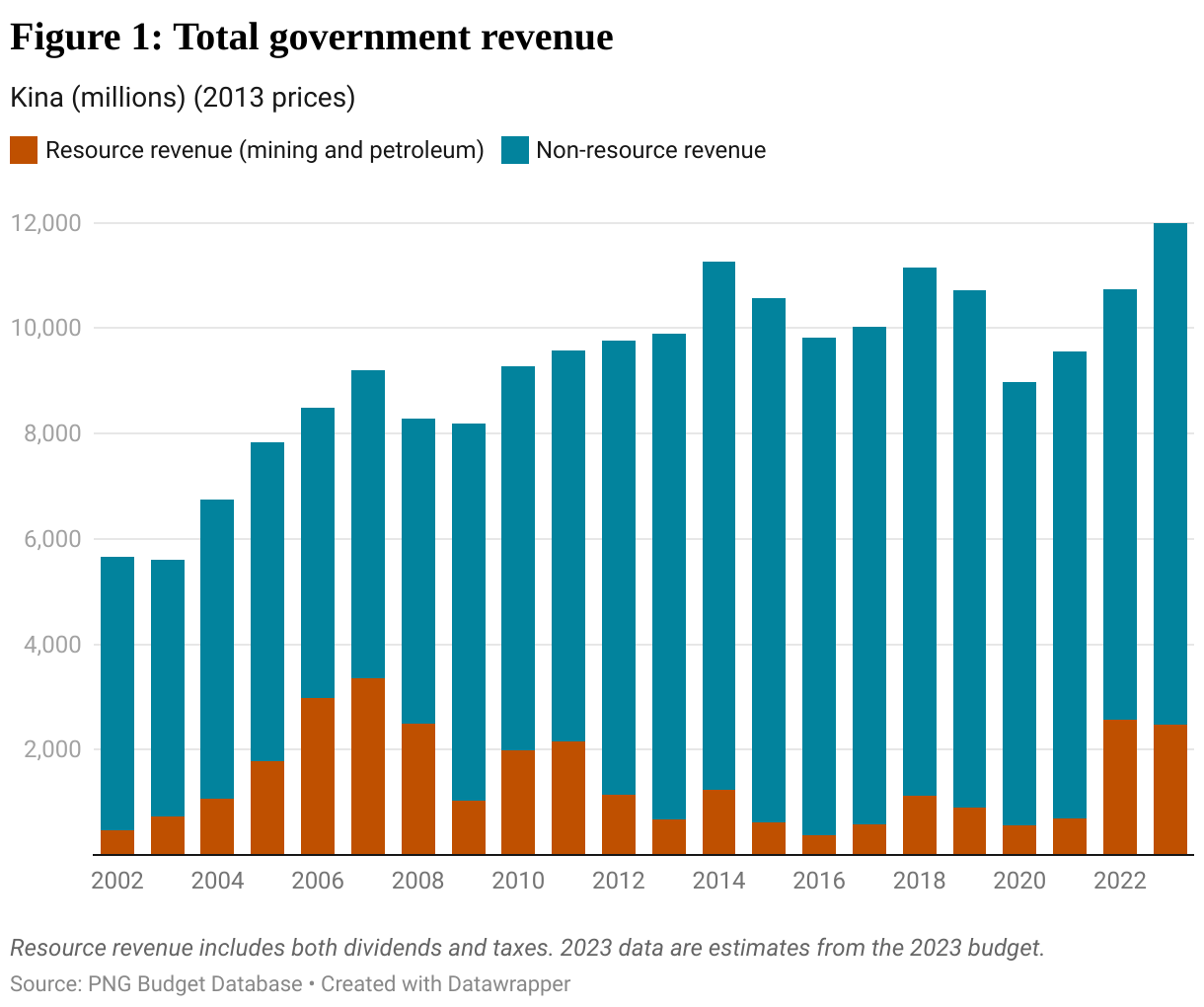

A lot of focus is usually placed on the challenges around resource revenue in PNG. But other sources of revenue matter too. Resource revenue has actually accounted for less than 10% of total revenue for most of the last decade, and is of course volatile, as Figure 1 shows. In comparison, income tax alone has contributed around 25-30% of total revenue over the last ten years, while GST and company tax brought in 17.7% and 12.2% respectively of total revenue in 2021.

Unfortunately, real revenue from each of these economy-wide taxes has stagnated at best and fallen at worst in recent years. Real personal income tax collections have declined relatively steadily since 2014 (Figure 2), in line with falls in formal sector employment. Personal income tax collections in 2022 are now expected to be close to 2011 levels in real terms.

Company tax collections have tumbled even more sharply in real terms from their peak in 2014 (Figure 3). While it’s unsurprising that a collapse in company profits flowed through to company tax collections as the non-resource economy contracted in 2015, it is striking that collections continued to fall in real terms even as growth in the non-resource economy resumed. The debt and extra capacity that firms took on in expectation of the boom continuing may have had lasting effects on firms’ profitability and therefore tax collections too. Similar to income tax, company tax revenue levels in 2022 are now expected to be at roughly the same level as they were in 2008.

Though GST collections have not grown significantly in recent years following super-rapid growth between 2011 and 2013, they have held relatively steady following initial declines in 2015 and 2016 (Figure 4). It could be that firms’ profits and therefore company tax collections are simply more sensitive to economic downturns than consumption and GST. An alternative explanation may be delays in the IRC providing firms GST refunds.

Aside from taxes, dividends have been paid out by PNG’s state-owned enterprises in just a handful of years in the last decade, including a payment in 2022 driven by high resource prices. All of this makes it relatively unsurprising that fiscal consolidation has eluded PNG over the last decade.

Unfortunately, the measures in the 2023 budget are unlikely to turn things around. The biggest revenue measure proposed was a 45% corporate income tax on licensed banks (worth K240 million in 2023). There are also some incidental revenue gains from a one-off increase to the excise duty on “anti-social drinks” (K30 million) and an increase in log export duties (worth K30 million in 2023). But none of these measures will tackle the structural decline PNG’s main tax collections have faced in recent years.

The K300 million that these measures will raise also fails to come close to providing the increase in revenue PNG needs. Together, they only account for less than 2% of total revenue in 2023 and will not even cover the K430 million revenue loss budgeted for 2023 from temporarily increasing the tax-free threshold for personal income tax (K280 million) and extending fuel excise exemptions until June (K150 million).

It is commendable that the PNG government is looking for new sources of revenue to fund crucial expenditure on health, education and infrastructure. But heavily taxing a key part of the financial sector which new players are just beginning to enter may buy revenue in the short term at the expense of longer term development.

The commitments made in the Medium Term Revenue Strategy to improve compliance and administration more broadly are a good start. Designing stronger tax regimes which ensure new resource projects contribute their fair share of tax, and using the Sovereign Wealth Fund to smooth resource revenue flows, would also help boost revenue without having to sacrifice development. Larger and more consistent dividend payments from state-owned enterprises would help too; the expected 2023 dividend from Kumul Petroleum is a good start, and should be maintained going forward.

At a higher level, revenue would also grow with improvements in economic conditions. Reforms that help unlock economic activity are therefore key. Making more foreign exchange available to let firms function optimally would be one obvious starting point. Directing government spending towards initiatives that generate jobs rather than enriching MP slush funds would be another.

There are certainly no easy choices. But the stopgap measures proposed in the latest budget are certainly not enough to bring an end to PNG’s budget deficits.

This is one of two blogs examining fiscal consolidation in PNG, using data from the PNG Budget Database.

Disclosure

This research was undertaken with the support of the ANU-UPNG Partnership, an initiative of the PNG-Australia Partnership, funded by the Department of Foreign Affairs and Trade. The views are those of the authors only.

About the author/s

Alyssa Leng

Alyssa Leng is a research officer at the Development Policy Centre.

Kingtau Mambon

Kingtau Mambon is currently undertaking a Master of International and Development Economics degree at the ANU Crawford School of Public Policy, for which he was awarded a scholarship through the ANU-UPNG Partnership.