Shoppers at Gordons Market, Port Moresby, Papua New Guinea

The Pacific: emerging from COVID, slowly

By Stephen Howes and Huiyuan Liu

19 October 2022

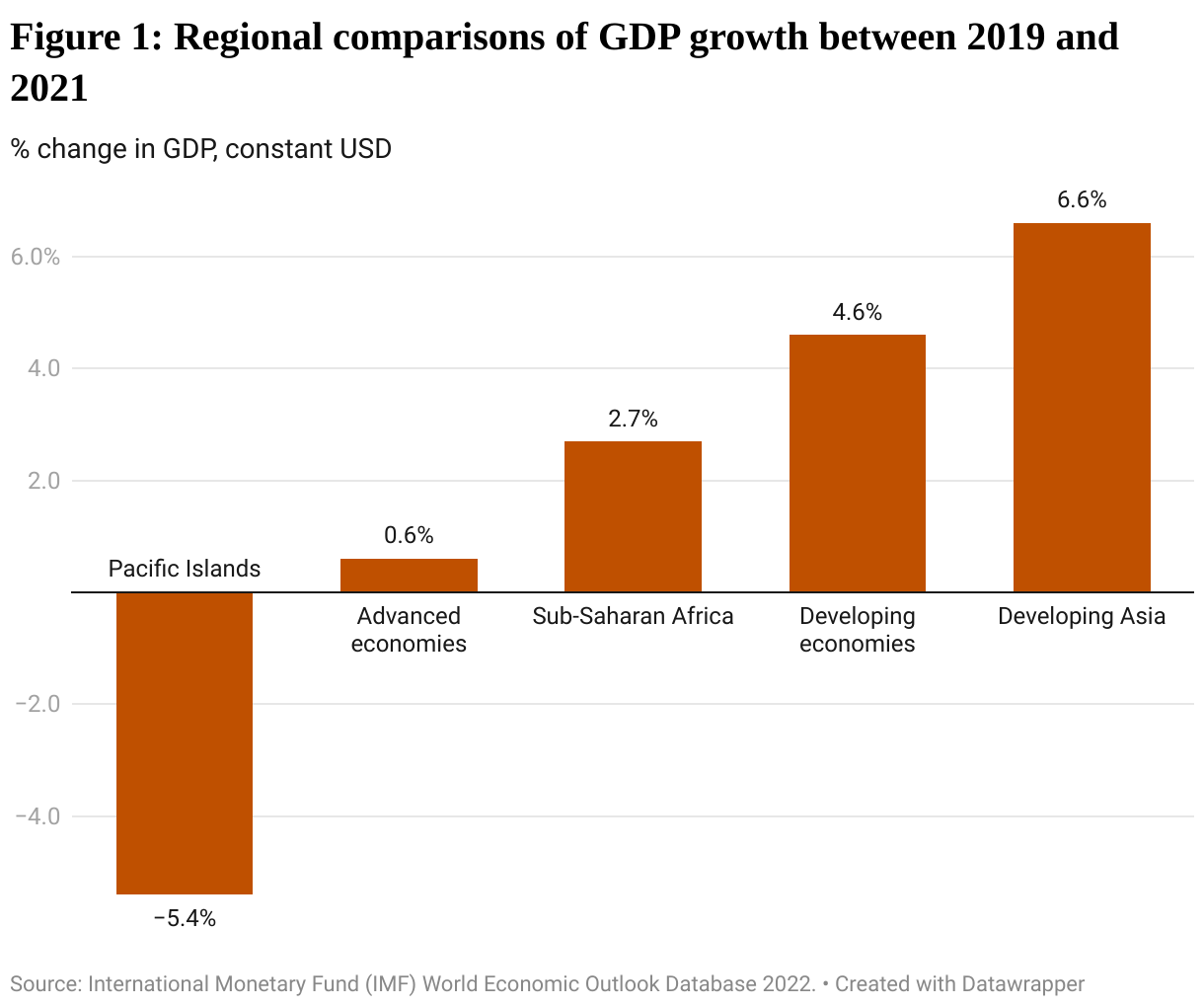

The impact of COVID-19 on the economies of the Pacific island region has been much more severe than on any other region or group of countries. The Pacific contracted by 5.4% between 2019 and 2021; other regions or groups at worst stood still and some managed growth despite the pandemic.

The tourism-dependent Pacific countries – Fiji, Palau, and Samoa – suffered staggering double-digit growth losses because of COVID-19. While other Pacific countries did not experience such extreme contractions, most of them still recorded negative or no growth.

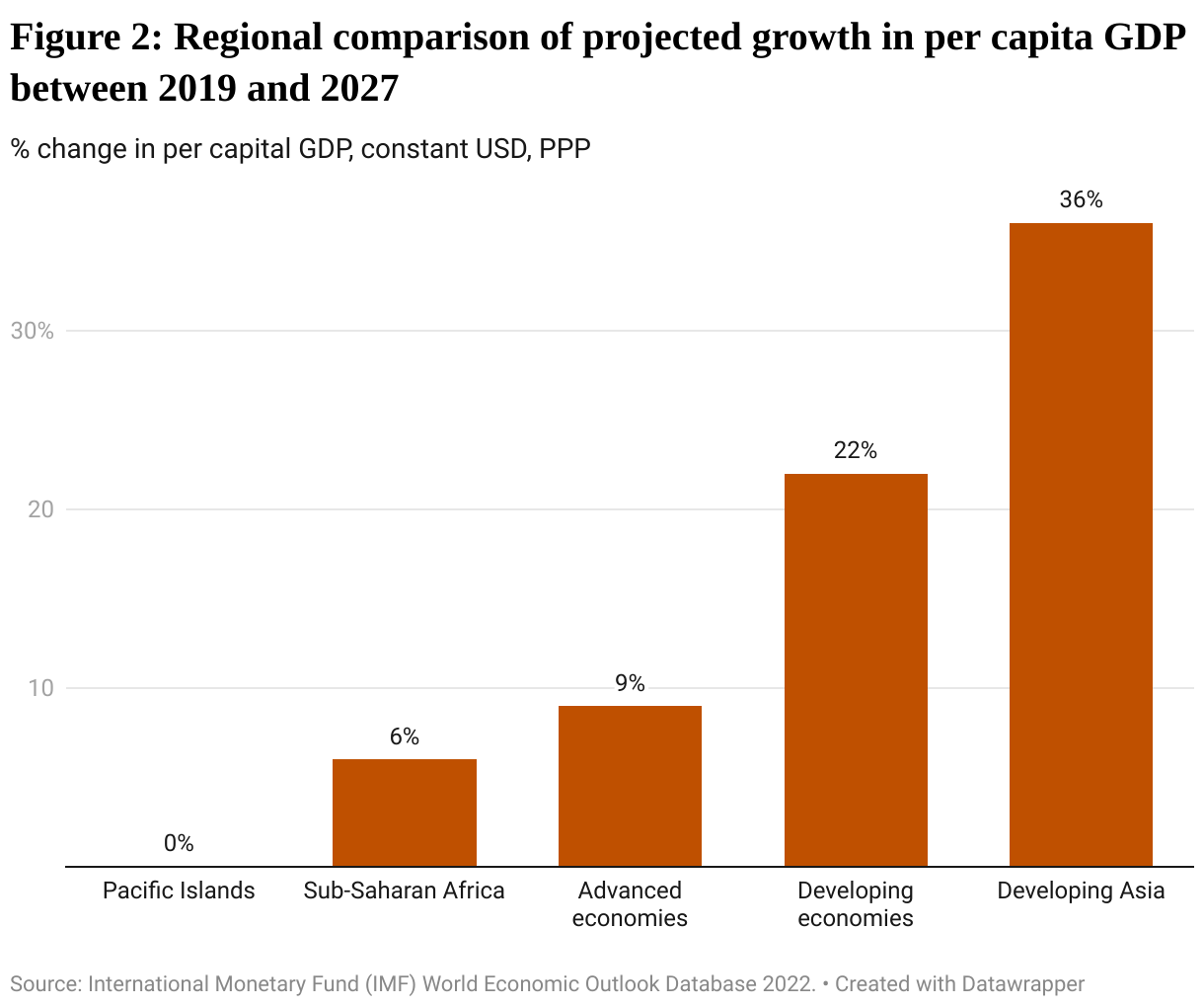

The IMF projects that the Pacific will grow on average at 5.3% over the next two years, bringing the region almost back to its pre-pandemic GDP level. This means the Pacific will have gone backwards in per capita terms, and have been outperformed by the rest of the world.

Moreover, there is no guarantee that the projected growth will be realised. In our new policy brief we identify the major risks to growth as the Pacific, like the rest of the world, enters a post-pandemic or ‘living-with-COVID’ era.

Our analysis shows that most Pacific Island countries have done well to contain debt increases and maintain strong external positions over the past two years – thanks to strong remittance flows, earlier rapid growth in fishing fees, and increased foreign aid. However, the Pacific economies remain vulnerable to exogenous shocks from potential COVID-19 outbreaks, inflationary pressures, and the prospect of a global slowdown.

Further outbreaks of COVID-19, both at home and abroad, could derail economic recovery. While half of the Pacific countries and territories had achieved the WHO 70% vaccination target by August 2020, three countries still have worryingly low vaccination rates – Papua New Guinea (3%), Solomon Islands (26%) and Vanuatu (42%). This puts a combined population of over 10 million people at high risk of further community outbreaks. Recurring outbreaks and COVID-19 policies outside the Pacific could also disrupt tourism recovery in the Pacific. An example is Palau. Despite reopening borders as early as April 2021, Palau’s tourism industry is still struggling to recover as tourists from East Asia, its main market, have been restricted or hesitant to travel.

Although domestic price levels in most Pacific countries increased only marginally in 2020 and 2021, inflationary pressures have started to be reflected in domestic price levels: the prices of most major commodities have skyrocketed due to global stimulus policies and the Russia-Ukraine war. While commodity exporting industries in some Pacific countries such as PNG and Timor-Leste have benefited from rising resource prices, most Pacific countries are commodity importers and, therefore, suffer.

Global inflation and other disruptions could cause the knock-on effect of a global slowdown as central banks raise interest rates to combat inflation. Major organisations such as the World Bank, IMF, OECD and ADB have all downgraded their growth forecasts and warn of a global recession. Pacific trade, tourism and remittances would all suffer if these risks are realised.

The biggest risk to post-COVID economic development in the Pacific, however, is a return to slow growth. As seen in Figure 2, current projections show no real growth in per capita income in the Pacific from 2019 to 2027, much worse than any other region. This suggests the prospect of a “lost decade” for many Pacific countries, as Alexandre Dayant and Roland Rajah of the Lowy Institute first warned back in December 2020.

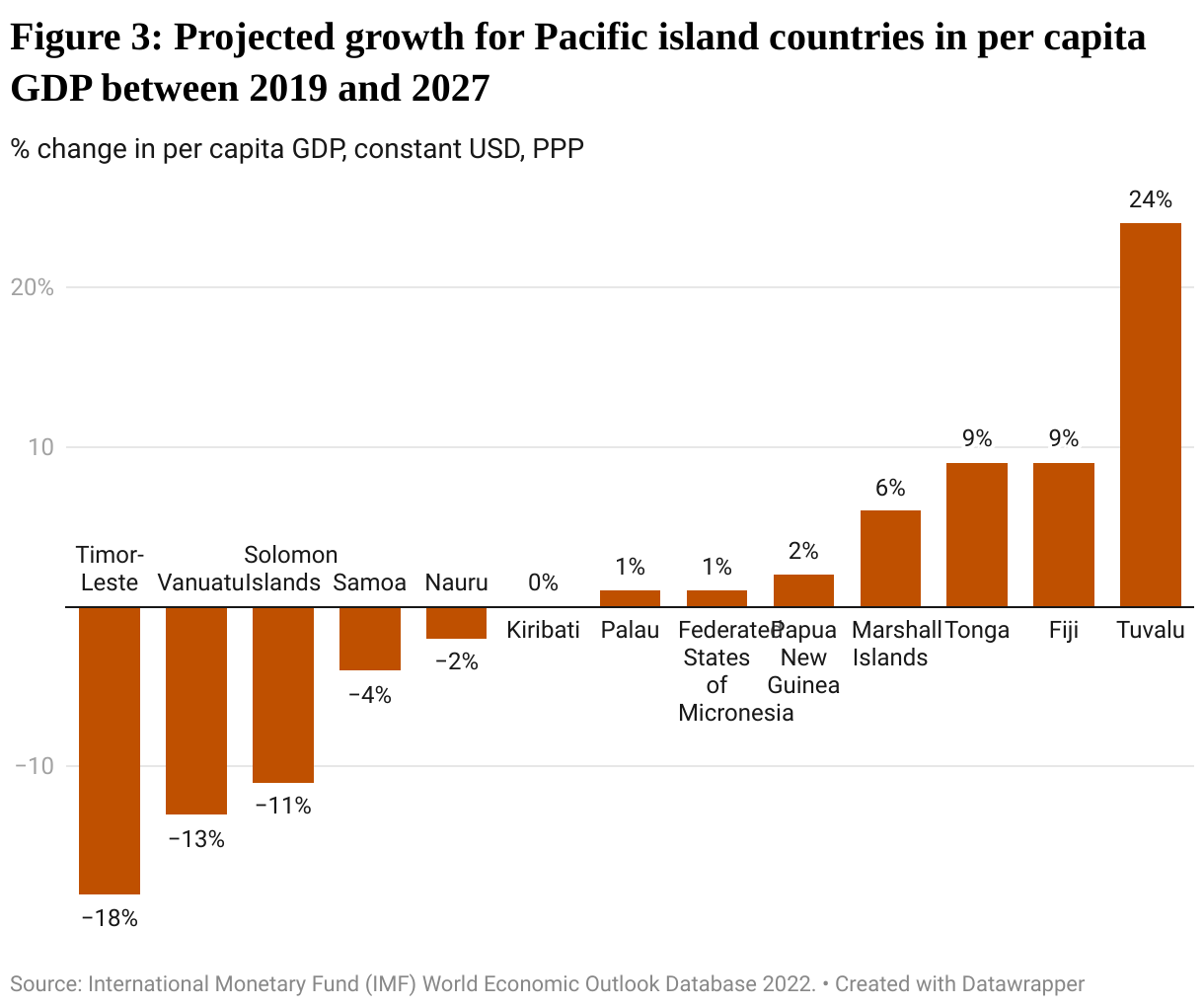

Timor-Leste, Vanuatu, Solomon Islands, Samoa and Nauru are projected to have lower GDP per capita in 2027 than they did pre-pandemic (2019). For Kiribati, Palau, Federated States of Micronesia and PNG, 2027 and 2019 levels are projected to be virtually identical. Marshall Islands is projected to show only 6% growth in per capita income, and Tonga and Fiji both 9% . Only tiny Tuvalu is projected to grow as much over this period as the average for all developing countries, 22%.

The prospect of Pacific countries being left behind again should be a wake-up call for the region’s policy makers. Given the dire outlook, aid directed to households will be important to help cushion the ongoing COVID blow, and labour mobility strategies will continue to make a lot of sense.

Above all, there can be no escaping the fact that the longer-term challenge of increasing trend growth rates via domestic economic reform and sound public investment has become more important for the Pacific than ever.

Read Devpol Policy Brief no. 22, ‘Emerging from COVID, slowly: a Pacific update’ by Stephen Howes and Huiyuan Liu.

Disclosure

This research was supported by the Pacific Research Program, with funding from the Department of Foreign Affairs and Trade. The views are those of the authors only.

About the author/s

Stephen Howes

Stephen Howes is Director of the Development Policy Centre and Professor of Economics at the Crawford School of Public Policy at The Australian National University.

Huiyuan Liu

Huiyuan (Sharon) Liu is a research officer at the Development Policy Centre, working in the area of economic development.