Coffee is one of the most important smallholder cash crops in Papua New Guinea. It accounted for US$156 million of export earnings, 13% of agricultural export revenues, and 1.4% of total export revenues in PNG in 2021. According to the PNG Rural Household Survey 2023, approximately 55% of sampled households in the highlands produce coffee.

During March and April 2024, the International Food Policy Research Institute (IFPRI) collaborated with the University of Goroka (UoG) to conduct gender-differentiated focus group discussions with coffee producers in Simbu and Eastern Highlands provinces to better understand the challenges and opportunities associated with coffee production and marketing in PNG. We completed 24 focus groups, each with 10 community members, discussing production, input usage, sales volume, production shocks, pest control, labour needs and market access.

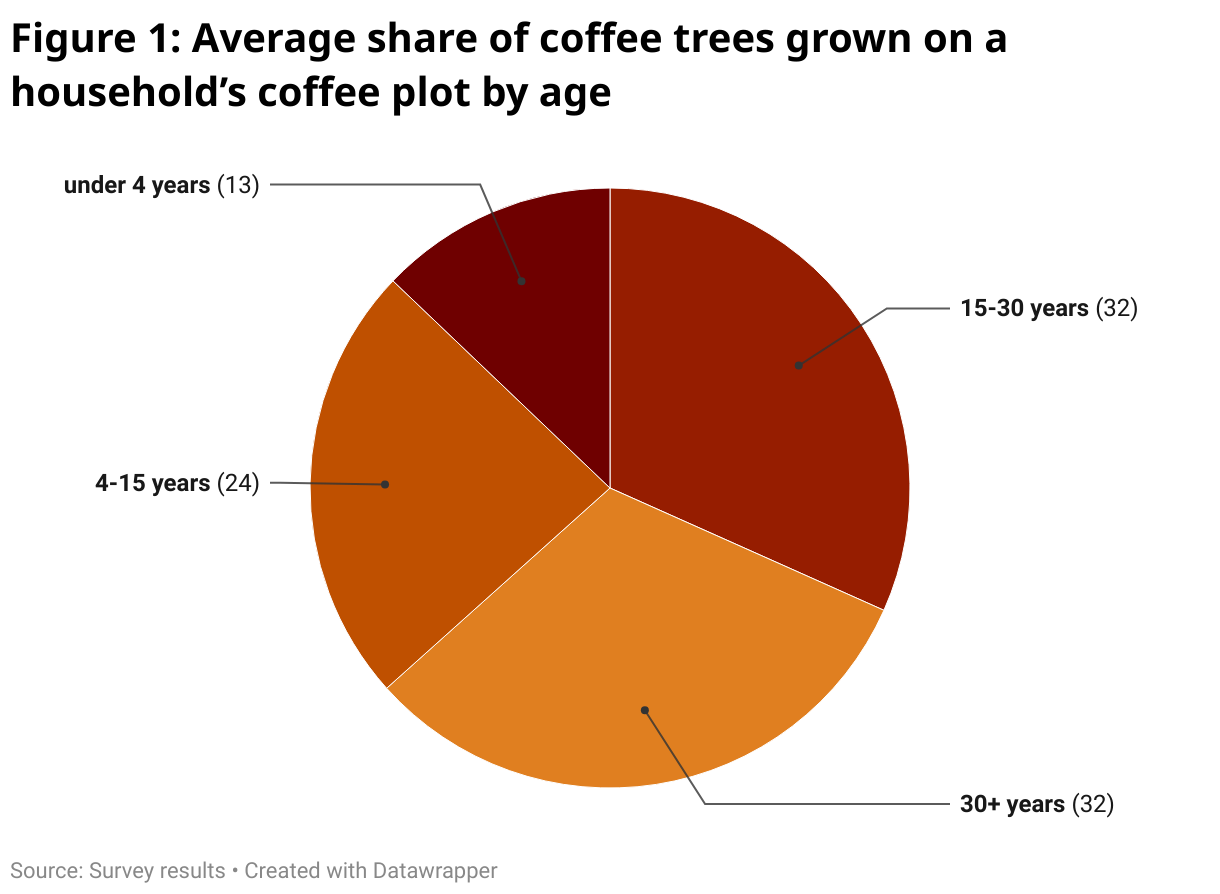

Sampled communities varied with respect to coffee-production scale, pest management, and marketing channels. On average, households reported owning two to three coffee gardens, with most trees aged 15 years or older. To calculate an approximate range of coffee yield per hectare, we asked producers to estimate the coffee yields of different-aged trees by drawing a line on the coffee-bean bags used to transport output to processors in town. Additionally, we asked focus groups to estimate the share of trees, by age, that are grown on an average household’s coffee block. Furthermore, we measured seven coffee blocks in seven different villages to count the number of trees by age category per one hectare area.

According to respondents, within a coffee block, a quarter of trees were aged between four and 15 years and equivalent shares were reported for trees aged between 15 and 30 years and above 30 years, respectively (Figure 1). Based on the dimensions and tree count of the selected blocks, we estimate that 3,000 to 4,000 coffee trees are grown per hectare of land. There are three harvest cycles for coffee within the focus group areas. For example, for trees aged from four to 15 years, the first harvest is the largest and constitutes about 50% of the overall yield, while the second and third harvests make up 30% and 20% respectively.

Given this, we measured the second-harvest yield of an average coffee tree (non-dwarf) in the Kofena community by picking and weighing the ripe cherries from three trees of different ages. For trees aged between 15 and 30 years, the second harvest yielded 0.63 kilograms of ripe red cherries. For the older trees (aged 30+ years) and younger trees (age four to 15 years) the weighed yield was 0.18 kilograms and 0.12 kilograms respectively. By considering the share estimates of first and third harvest for different-aged trees, along with the measured yield from the second harvest, we calculated the weight of red cherries harvested from each age category of coffee tree.

Using the conversion formula provided by World Bank 1986 and the PNG Coffee Industry Corporation (CIC) Handbook, approximately one kilogram of ripe red cherry yields 0.21 kgs of dry parchment (partially processed coffee beans). Based on the estimated red cherry yield, approximately 417 to 560 kilograms of dry parchment can be harvested per hectare in the focus group study area. Similar results were reported in the 2017 ACIAR report on coffee-based farming systems in the highlands of PNG, indicating that households in Bena and other Eastern Highlands Province districts produced an average of 522 kilograms and 386 kilograms of dry parchment per hectare per year respectively.

Compared to other countries such as Colombia and Indonesia (the second and eleventh largest producers of Arabica coffee, respectively), the estimated PNG parchment yield per hectare is substantially lower. For example, Colombia and Indonesia produce an average of 1,080 kgs (USDA 2023) and 937 kgs (USDA 2020) of dry parchment per hectare.

We identify low coffee yield as a significant challenge in the PNG highlands which is further exacerbated by pest infestations, particularly from Coffee Berry Borer (CBB), a small species of beetle that lives, feeds, and breeds inside coffee berries. Over three-quarters of the sample communities reported losing more than half of their harvest to berry borer infestations last season.

Lack of market access and price inconsistency pose another challenge for coffee producers. During the last harvest season (March to June 2023), dry coffee prices ranged between 3.5 and 7.0 PGK (US$0.90-1.81) per kilogram, with the highest price being paid at the onset and end of the season when coffee bean supply is relatively low. Most growers received a standard price per kilogram for their output irrespective of quality. However, communities associated with coffee associations or located near coffee processors benefited from extension services to improve output quality and negotiate quality premiums (an extra two or three PGK per kilogram) for their harvest. Furthermore, an overall low adoption of coffee certification in our sample suggests an important unrealised potential for achieving higher premium market values.

To overcome these production challenges, efforts should be directed towards improving yield and quality through improved farm practices and integrated pest management strategies. Having access to cost effective pest control solutions and guidance on the correct usage of fertilisers, soil management, and proper pruning practices are some crucial steps to boost production and control CBB attacks.

Establishing and providing financial support to coffee associations can strengthen market ties, enabling farmers to negotiate better prices. Encouraging direct contracts with international buyers could provide profitable market opportunities and financial incentives to ensure quality output, as seen in one village in our sample that directly supplied green beans to a US coffee roaster and received an average 11-13 PGK per kg.

While the Coffee Industry Corporation (CIC) and exporters like PNG Coffee Roasters and Monpi Coffee offer extension certification and provide support to coffee associations in accessing domestic and global markets, an additional opportunity to increase market value for PNG coffee is to identify areas where organic coffee certification can be ascertained. However, price premiums on organic coffee production must be built into a transparent production, grading, and marketing system that incentivises and rewards producers for high quality output.

The authors acknowledge Harry Gimiseve and Wendy Safi for assisting the team with focus groups; their contributions were essential for our improved understanding of coffee-farming communities.

Interesting work – I like the way authors have presented the information highlighting the business opportunity. Certainly, looking at the age distribution of trees, and the average yield of coffee that is in the lower end compared to other producers, there is a huge opportunity to invigorate the industry with new investment in the production system. As a under-storey forest plant in its natural setting, coffee is best grown as a component of a tree crop farming system. That could have additional benefits as it can extend income opportunities, spread risks and create a more conducive environment for smallholder farmers who need a regular income to stay connected with the farm and their community. A farming systems focus can also help spread new ideas on integrated pest management drawing on ways to improve crop hygiene, plant and soil nutrition and year round labour force utilisation to encourage more productive and sustainable farming.

An earlier ACIAR research study – https://www.aciar.gov.au/project/asem-2008-036 – recommended that intercropping with vegetable as a an alternative that should be investigated. A farming systems based studies, for instance can investigate viable components of a multiple enterprise farming system and innovative , context relevant ways to build on this important work. There are many ways such a study can incorporate other pressing issues of adapting to climate change and rural development challenges in enhancing child nutrition and gender equality.

In Canberra, we have two cafes (in Curtin and Duffy) that sell both the beans grown in the PNG highlands and a cup of coffee made from them. It’s direct action that supports those growers.

It’s also excellent coffee.