Sometimes writing headlines is just too easy: “The new Porgera: old wine, new bottles” would have been a simple summary of the recent news that, following the passing of new legislation by the Papua New Guinea parliament, the Porgera gold mine reopened on 22 December 2023, and will pour its first gold in nearly four years in the first quarter of 2024.

To recap briefly, the Porgera mine opened in 1990, producing four million ounces of gold in its first four years of operation. Over the intervening 30 years it has had a chequered history, with the ownership of the Porgera Joint Venture (PJV, the operator) changing at least a dozen times (with the state’s interest shifting from its original 10% to 25%, then down to zero, and now to a majority position of 51%), and environmental, human rights and social issues bedevilling the mine.

The James Marape-led government declined to renew the special mining lease (SML) in 2020 and the mine closed. At the time, Barrick NL (BNL) was the majority partner in the PJV, owning 95% of the mine, split 50/50 between Barrick Gold and its Chinese partner Zijin Mining.

To restart the mine, Barrick and Zijin agreed to reduce their stake to 49%, allowing PNG interests to take the remainder: local landowners 10%, Mineral Resources Enga (MRE) 5%, Kumul Minerals Holdings Limited (Kumul), on behalf of the state, 36%.

The deal is claimed by Prime Minister James Marape as a win for his “take back PNG” campaign, and the equity split does look similar to arrangements in New Caledonia where local interests hold a controlling 51% in several mining and refining joint ventures. However, scant detail has been forthcoming since the new shareholding arrangement, and the commitment that PNG stakeholders and BNL would share the “economic benefits generated over the life of mine on a 53/47% basis” was announced nearly three years ago.

Barrick Gold Chief Executive Officer Mark Bristow said this represented “a fair deal anywhere in the world”, but it is not clear what it means. Will local interests receive 51% of the sum of dividends, royalties, compensation payments, wages, value in the supply chain, group taxes on salaries and wages of employees, and company tax over the life of the mine? In December 2023, Barrick said “this is expected to amount to more than [US$]7 billion over the mine’s projected 20-year life”. It would be a terrific deal if this were the case.

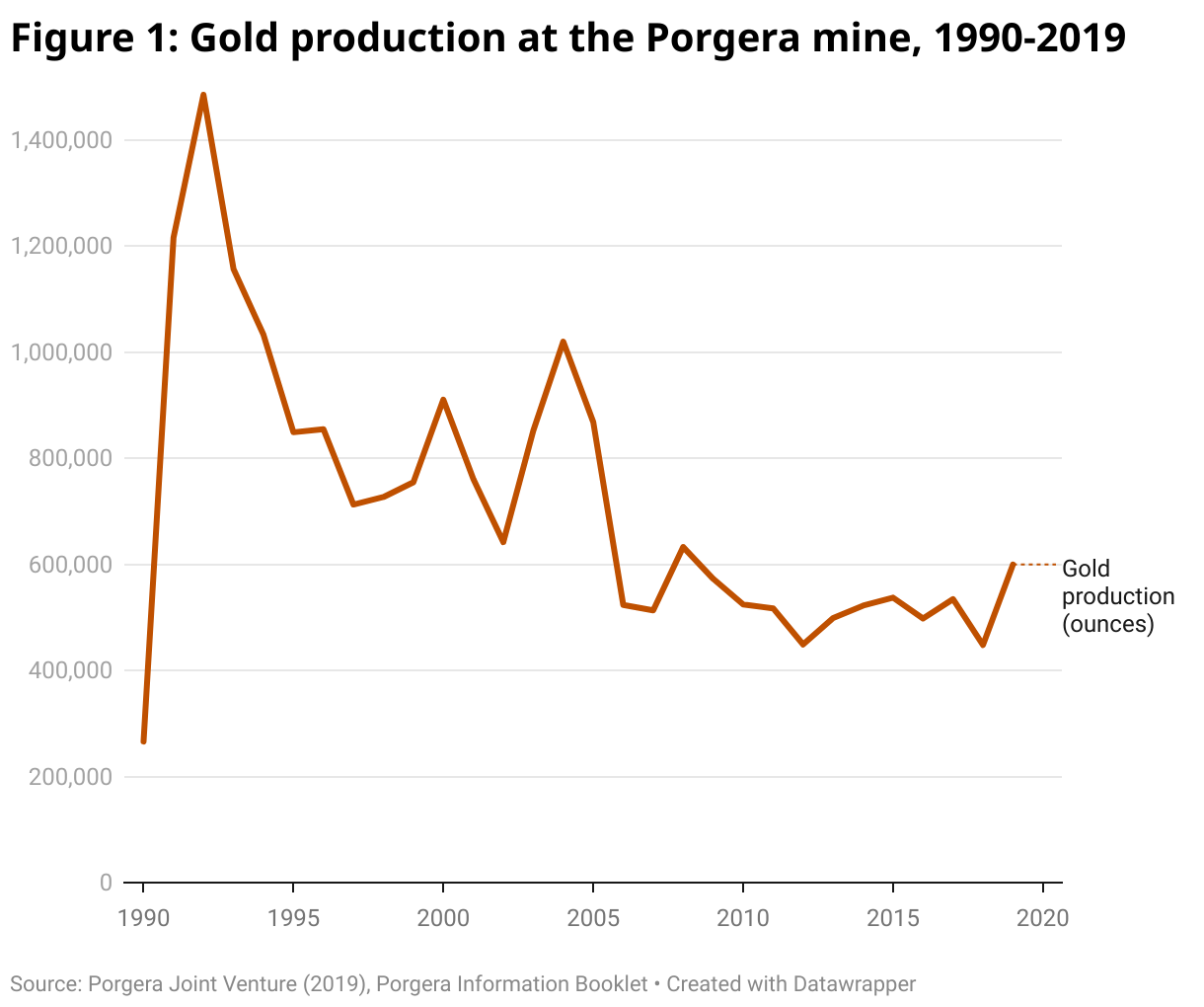

Earlier in 2023, Barrick said that the forecast was for production of 700,000 ounces per year. With an anticipated gold price of US$1,800 per ounce, this would value the PNG stakeholders’ share at over US$640 million, or over K2.5 billion, a year – a good deal more than the annual K1.1 billion contribution to the economy estimated in an INA report in 2020.

However, not so fast. During the last five full years of operation, the Porgera mine produced around 520,000 ounces per year, not 700,000 ounces. The higher figure was last attained in 2005 when Porgera’s published proven and probable reserves were twice as high as recent estimates suggest. The long-term trend is for a decline, not a reclaiming of the mine’s former glory (Figure 1).

In August there was a buzz of reports and excitement regarding the Development Forum – negotiations required under the Mining Act for major mining projects prior to the issuing of an SML. The “New Porgera” Development Forum opened in Wabag in September with the assumption that it would produce a set of agreements similar to those negotiated in 1989, and that the conclusion of the Development Forum would then allow for the issuing of leases and signing of final contracts.

Instead, the language around the Development Forum softened over the next week, and the forum then moved to Alotau, supposedly to avoid fighting in Enga. The outcome from Alotau was a commitment to an umbrella community development agreement to take on board submissions from stakeholders within the footprint of the mine (including the Hides powerline and the downstream riverine environment) as had previously been done for the ExxonMobil-led PNG LNG project.

A new SML was issued on 13 October 2023, together with a development contract between the PNG government and the new operator, New Porgera Mine Ltd. Meanwhile, key stakeholders like MRE were still in the process of presenting their negotiating positions.

The Mining (New Porgera) (Amendment) Act 2023 – an amendment to the existing 1992 Mining Act which passed parliament in November – paved the way for the reopening of the Porgera mine by providing a basis for the 46 compensation agreements between different landowners of the various leases that the mine at Porgera covers. The Act modifies the existing Mining Act to allow for the continuation of existing compensation agreements until such time as new ones are finalised and provides for the back-dating of any revised payment rates. Barrick and the state defend the Act as a legitimate streamlining of what have been drawn-out processes for other major developments.

The achievement of both Barrick and the PNG state – notably in the persons of Prime Minister James Marape, Kumul Chair Dr Ila Temu, Chairman of the State Negotiating Team Dairi Vele and MRA Chairman Jerry Garry – in effectively fast-tracking the necessary agreements is certainly noteworthy. However, the perspectives of the different parties on what success might mean have yet to be reconciled, and the relative lack of transparency around the details of the various agreements raises concern. These issues will be dealt with in a subsequent post.

This post is the first part of a two-part series on the reopening of the Porgera gold mine. Read Part 2.

Outstanding. Well presented

Commend you both for the insights; correct me if I am gone wrong here. Please can you both clarify where does the legitimate landowners of Porgera fits here. The land is own by the people of Porgera and where are their potions of their shares in all these deals. I see something is totally wrong in this mining deal done. I see no legitimate landowner representative being in any major stakeholders meetings and so forth……pigs and dogs have been benefiting since 1990 and its enough, lets be fair…we need to put it out clearer for the good of this God given beautiful people of Porgera Valley. Let them see some lights now, 30 plus years of living in no mans land and doing cowboy mining must come to an end. May the Mother Nature blessed those who have benefited over the past years and let go now so the poor legitimate land owners can enjoy the remaining of the mining.

Thank you for this platform so I can view my thoughts as a neighboring district of Laiagam.

Outstanding. Structured well.

The gold has been dug out since I was a child and the company doesn’t pay the payment for the environment damage. My appeal to PJV and Barrick to pay 10 million for this season of mining. I’m in POM. Please honour my word and take action hurry before such illegal happens again.