The savings target for Papua New Guinea’s Supplementary Budget is unclear. When announcing in August that there would be one, the Treasurer stated that [paywall] “the Government will ensure that the deficit will be lower than the deficit planned in the 2015 Budget”. This deficit is K2,272m, or 4.4% of GDP. Similarly, the Governor of the Bank of PNG said on 26 August that “the target deficit the Government is aiming for in the revised 2015 Budget, to be presented to Parliament in the October/November session, is a deficit not greater than the budgeted level.” Both these announcements would require savings of K2,545m – equivalent to the expected revenue reductions in 2015. The Secretary of the Treasury also stated that the cuts would be at least K1.6 billion, and up to K 2.6 billion, in a speech to the Brisbane Business Advantage meeting last month. The target of K2,545m is used as the reference point in this analysis. However, more recently, the Treasurer has stated [paywall] that the expenditure savings target is K1.3 billion. As this analysis shows, this turns out to be much more realistic.

The Treasurer’s August announcement also stated that “the 2015 National Budget priority areas of education, health, law and order, and provincial and district support grants will not be affected”. There have also been more recent statements that key economic infrastructure projects will also be protected, but this is not possible within the savings target, as revealed below.

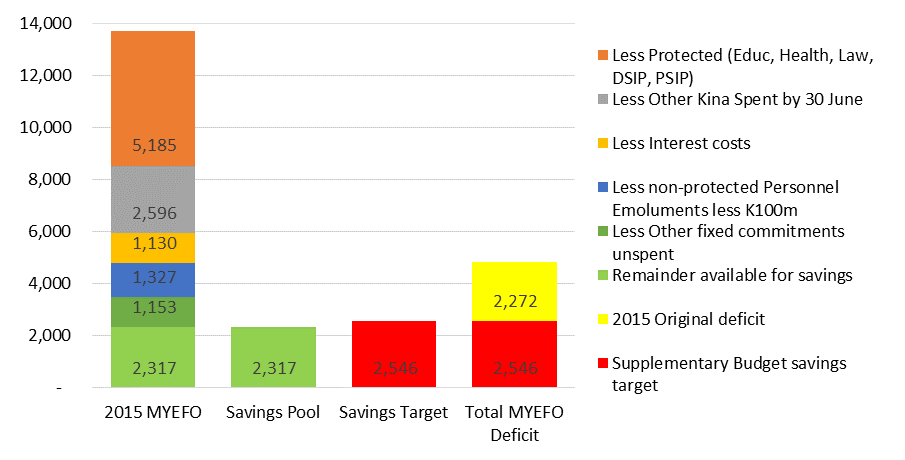

The attached spreadsheet examines the pool of possible savings – this represents the maximum amount of savings that theoretically would be possible after allowing for the policy areas that are “protected”, already spent or otherwise locked in. The starting point is the total Government of PNG domestic budget (excluding aid-funded projects) for 2015 of K13,708m. The value of the protected areas mentioned by the Treasurer (so, excluding infrastructure) amounts to K5,186m. The MYEFO indicated that K2,596m had already been spent outside of these protected areas. Interest costs are a fixed commitment and amount to a further K1,129m, which can’t be saved. As it is very difficult to get major savings from public sector wages this late in the year (let’s assume the maximum saving would be K100m), then another K1,327m is locked in through wage costs in non-protected areas. Finally, there are fixed commitments that the Government is obliged to fund, such as legal requirements under the PNG LNG project, certain grants to provincial governments, practical items – from payment of superannuation entitlements through to office accommodation – and items listed as priority commitments in the MYEFO (such as maintenance of national priority roads and national bridge maintenance). These commitments total K1,551m, of which a maximum of K399m had already been spent by the MYEFO, leaving at least K1,152m in remaining fixed commitments.

Altogether, the remaining funds available to find savings in the 2015 budget are K2,317m (the savings pool – shown in green in the graph below). This is less than the savings target of K2,545m – shown in red. Based on announced government policy, it is simply not possible to reduce the deficit back to the original 2015 deficit level. It is not realistic to stop all funding even in the identified “savings pool”. This would mean stopping all work on infrastructure activities, starving all non-protected agencies of goods and services funding, and not making an allowance for new pressures, such as the drought.

There are two implications of all of this. One, savings will have to be sought from within the protected areas. Indeed, there are several reports of cuts to education and health. Two, even with this, the K2.5 billion target looks out of reach. The most recent K1.3 billion target looks a lot more sensible. At the same time, the 2015 El Nino effect of frost and drought is clearly a major national disaster. The current allocation of funds (K30m) appears grossly inadequate. Indeed, quick calculations suggest that the level of drought relief provided in 1997 by the government and donors was equivalent to over K600m in 2015 terms. Even with a more effective and lower cost response, this is a big ticket item that is likely to require funding many times the current allocations. Smaller overall savings means a higher deficit, of 7-8% of GDP, as well as higher public debt levels.

2015 Supplementary Budget – remaining flexibility

Despite these challenges, a Supplementary Budget would be an important step towards building confidence in the management of the budget following the frightening losses in revenues shown in the MYEFO. It is appropriate that the Parliament authorises reductions in the initial appropriations given the major policy implications involved. Importantly, by lowering the appropriations, it helps ensure that there will be no blow-out in expenditures as part of the close of accounts in late December.

An even more important document than the Supplementary Budget would be the 2016 Budget Strategy. Under the Fiscal Responsibility Act [pdf], the government is obliged to release a Budget Strategy three months prior to the Budget (so by mid-August). This document should set out the priorities for the 2016 Budget and a medium-term fiscal adjustment path. The drop in resource and other revenues revealed in the MYEFO is not a once-off adjustment. Simply deferring capital projects will not address the underlying fiscal challenges revealed in the MYEFO. Major adjustments will be required on both the revenue and the expenditure sides, and these need to be set out over the medium-term. Encouragingly, the government now seems to have recognised [paywall] that its earlier target of a balanced budget by 2017 is unrealistic. (Less encouragingly, there was no “Concluding Statement” from the recent IMF Article IV mission, which could have improved transparency about the current challenges.)

The Supplementary Budget is an important accountability mechanism for ensuring that the Parliament makes the key decisions on how to reduce their earlier appropriations. But it should have come out in the first quarter of 2015 or, at the latest, at the same time as the MYEFO. Especially given its lateness, the savings sought should be modest. The really important document for now is a 2016 Budget Strategy that sets out a credible medium-term path for avoiding a fiscal crisis.

Paul Flanagan is a Visiting Fellow at the Development Policy Centre.