The reforms to superannuation spearheaded by Sir Mekere Morauta in 2000 are regarded as among the most important in Papua New Guinea’s history. Certainly, those reforms succeeded in stabilising the sector and ending the mismanagement and scams that were a feature in the 1990s.

But how have the superannuation funds performed since those reforms? That is a question that has received very little attention. In this article, we provide some initial analysis. To do so, we use the annual reports and published figures from 2008 to 2025 of the two superannuation funds that dominate the PNG market, Nambawan Super (NSL), whose members are predominantly in the public sector, and Nasfund, which has a mostly private-sector membership base.

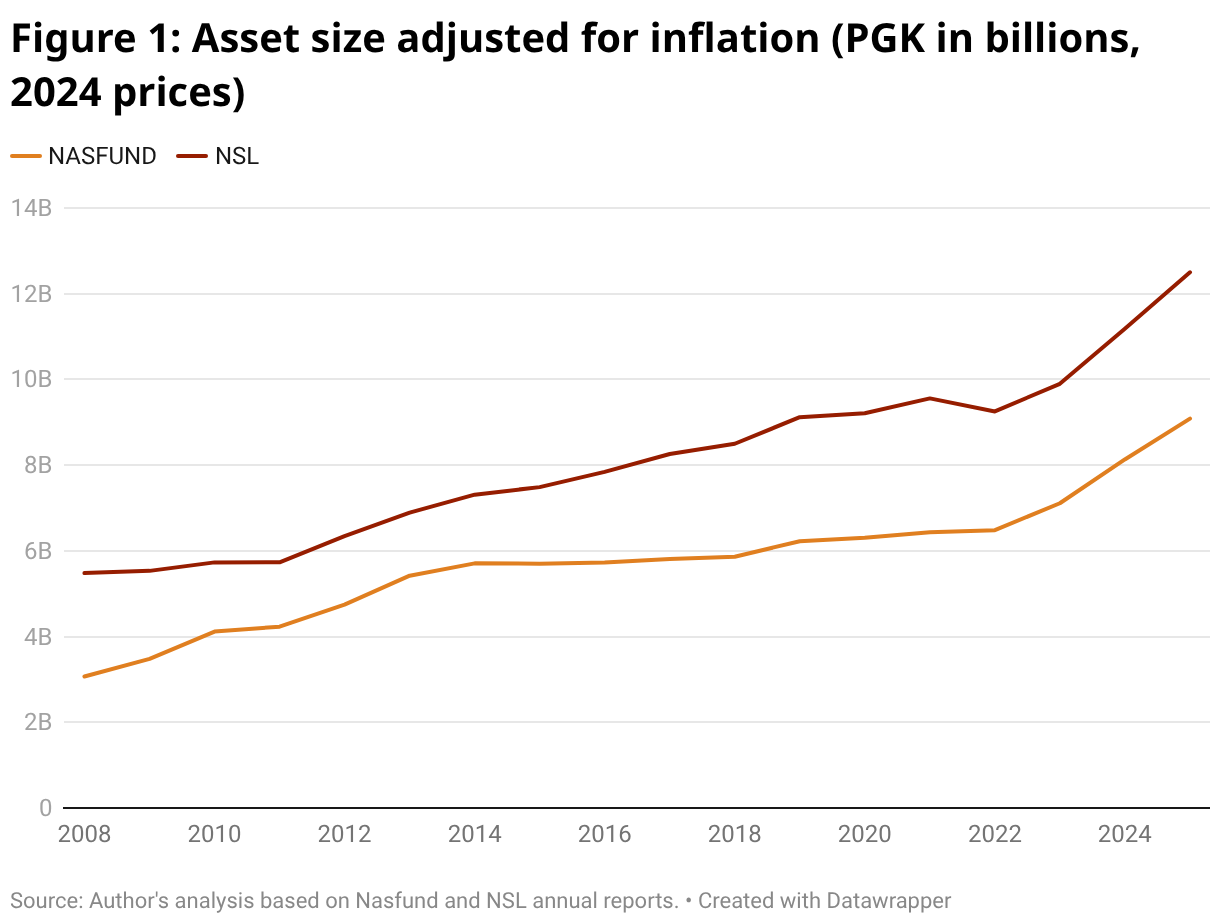

The asset value of both funds has grown impressively. NSL is larger, but Nasfund has grown faster: adjusting for inflation, Nasfund’s asset value grew at an annual average rate of 6.3% compared to 4.6% for NSL (or for the whole period of 2008 to 2025, 196% vs 128%). As a result, while NSL is still the dominant fund judged by asset value, its share of the combined value of the two funds is falling: from 64% in 2008 to 58% in 2025.

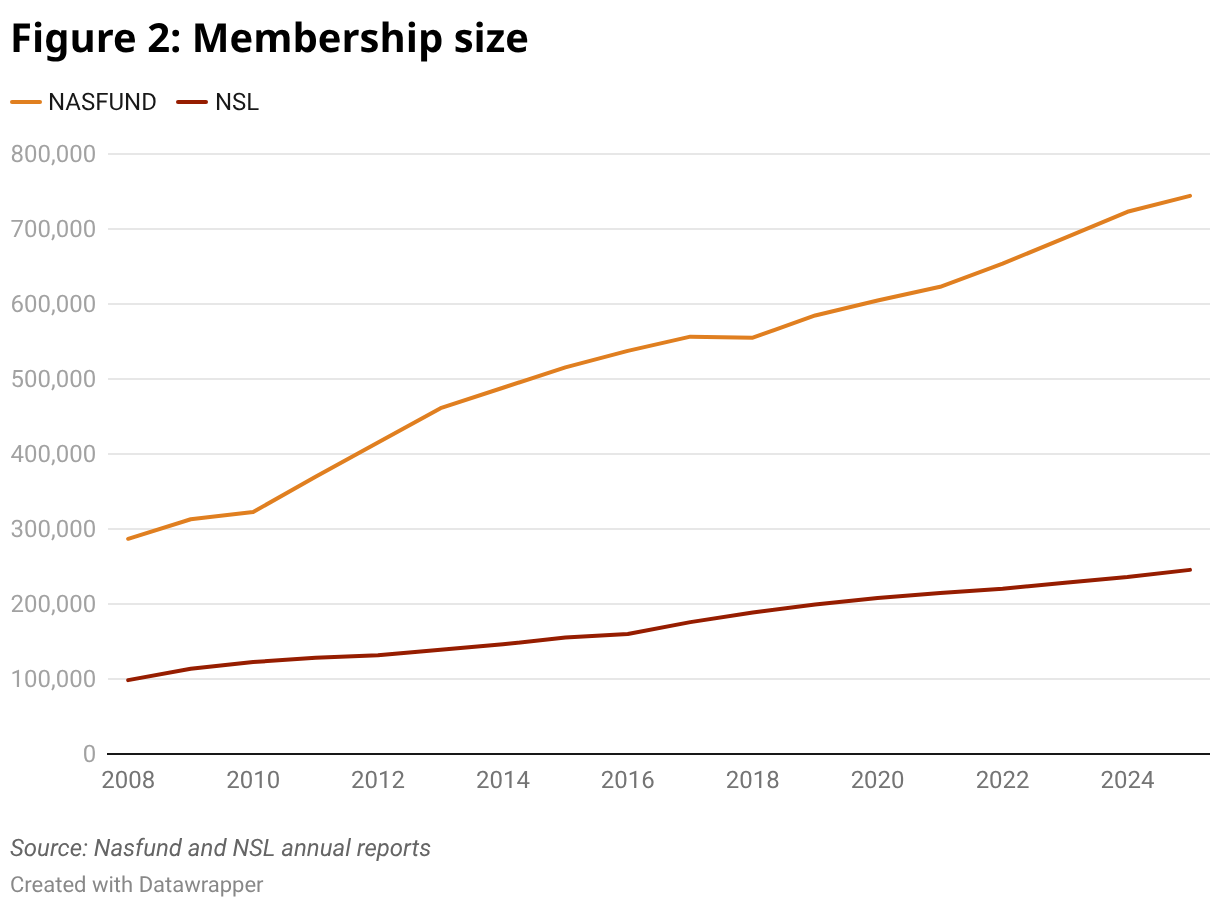

Membership numbers have also increased, as shown in the second graph. In terms of members, Nasfund is much bigger. Between 2008 and 2025, Nasfund’s membership grew by 159%, compared to NSL’s 148%. Nasfund’s market share in terms of membership has been roughly constant at 75%. It should be noted though that a single employee may have more than one superannuation membership if they change jobs, and that there are a large number of unidentified members.

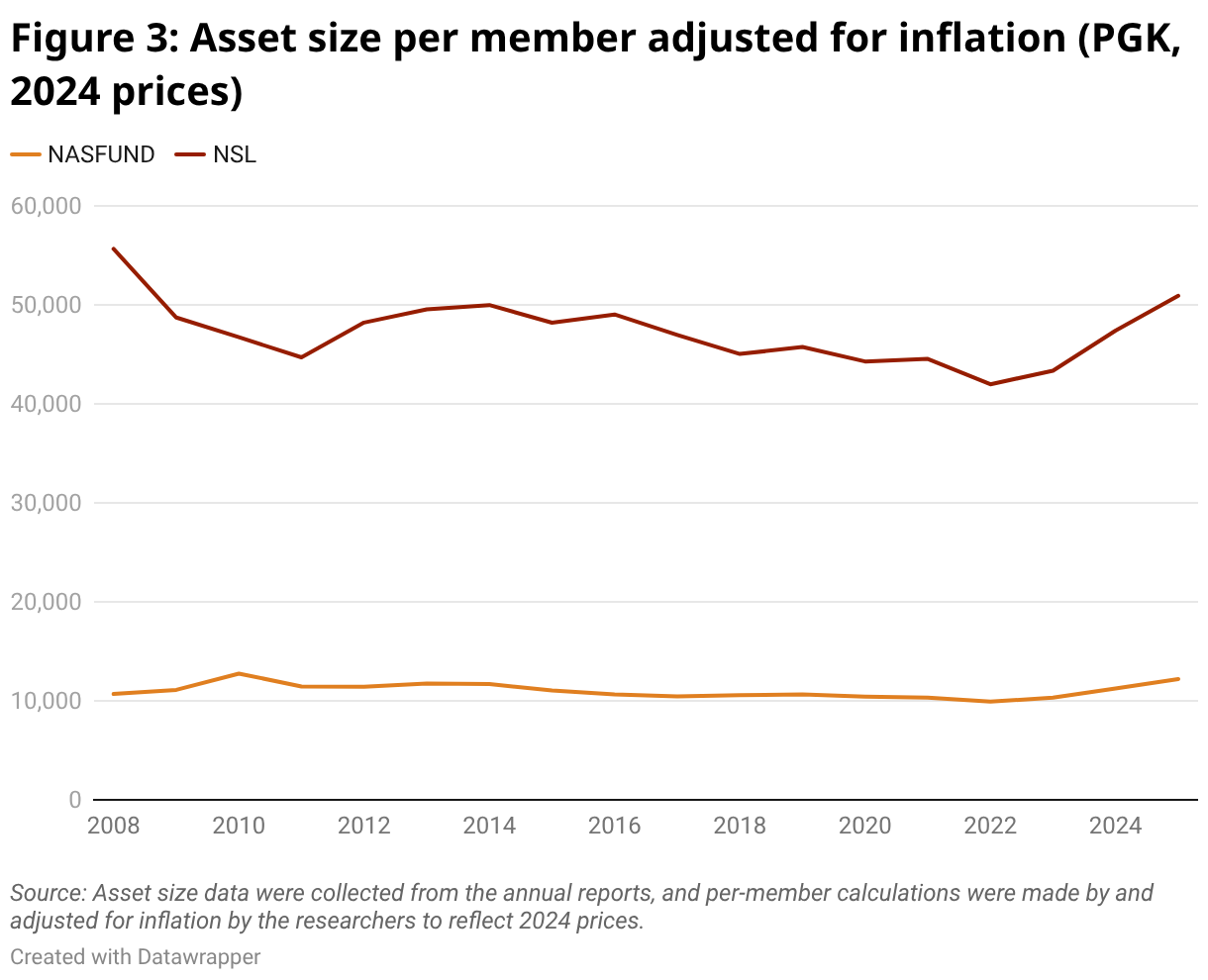

The membership growth has roughly matched the growth in assets. Adjusting for inflation, Nasfund’s asset value per membership account has been constant while NSL’s has actually fallen.

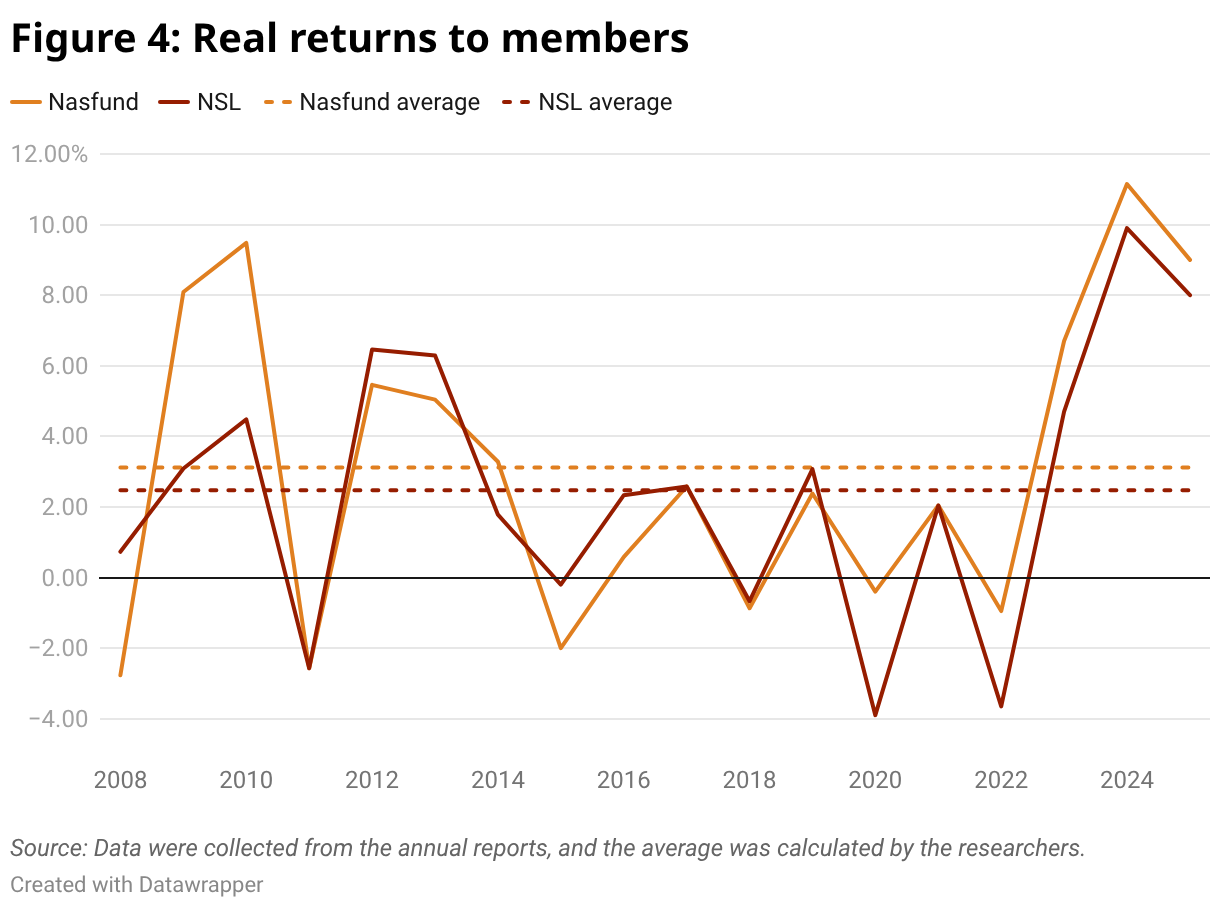

The best indicator of performance is the returns superannuation funds provide to their members. This is the “crediting rate” or “interest credited to members’ accounts”. It is calculated as gross investment earnings minus costs, adjusted for any change in reserves. To get the real return, we adjust for inflation (measured using the CPI). Real returns to members on average for the 2008 to 2024 period are 3.1% for Nasfund and 2.5% for NSL. By comparison, a 2018 Productivity Commission report (p. 6) reported Australia’s superannuation funds’ average annual net returns (that is, net of fees and taxes) as 3.5% after inflation for the last 21 years.

It is tempting to blame the somewhat lower returns of PNG’s superannuation funds on the weak economic performance of recent years, but the period we cover also includes the boom years. GDP growth between 2008 and 2024 averaged 4.3%. Most of the benefits of that have flowed offshore, but non-resource GDP growth (that is, growth calculated after taking out the resource sector, which is dominated by multinationals) grew by 3.7% between 2008 and 2024.

In NSL’s case, a huge burden has been its “unfunded liabilities”. At the end of 2024, the PNG Government owed NSL PGK1.1 billion in employer contributions from before the reforms (2024 Annual Report, p. 82). The lost opportunity for the fund to invest these monies on behalf of NSL members (mostly public servants) would be very substantial. However, unfunded liabilities should not affect returns to members.

Both funds would like to invest more offshore. The government-imposed limit on offshore investments, designed to support domestic investment, is 35%. However, constraints on foreign exchange availability mean that this limit is not actually binding. For example, NSL holds about 20% of its assets offshore (2024 Annual Report, p. 12). Allowing super funds to invest offshore up to the limit would help them improve returns.

Superannuation funds are also now significantly more heavily invested in government debt than they were previously. Only 10% of superannuation assets were invested in PNG government debt in 2010, but this increased to 40% by 2019 (see the IAG Phase One Report, Figure 17). This suggests a lack of domestic investment opportunities.

One option would be to remove the offshore cap and replace it with a minimum requirement for domestic investment. This would allow the super funds to substitute their government bond holdings for potentially more lucrative overseas assets (if foreign exchange availability was improved), while still keeping them focused on growing the domestic economy.

Another factor pulling down returns could be increasing administration and management costs. According to our calculations, both Nasfund’s and NSL’s costs more than doubled after inflation between 2008 and 2024. Nasfund’s costs increased by 112% and NSL’s by 187%.

A deeper problem might be the lack of competition in the sector. From this point of view, we welcome the 2024 announcement by the Bank of Papua New Guinea (BPNG), PNG’s central bank and superannuation regulator, that it was licensing PacSuper as a new entrant into the superannuation sector. However, superannuation choices in PNG are mainly made by employers, not employees. And employees have no influence on how their funds are invested (for example, more or less conservatively). Perhaps giving employees more choice would help. However, this would also increase costs, and at the current time employees with NSL are not allowed to transfer to Nasfund owing to legacy underfunding issues.

How PNG’s superannuation sector should be reformed is clearly a complex question. In 2021, BPNG set up a committee to look at superannuation reforms — the Superannuation and Life Insurance Review Committee. However, its report was never released.

Given that competition is difficult, if not impossible, regulation is needed. This should cover not only issues of propriety and risk, but also performance and cost management. Unfortunately, it is not clear if BPNG is exercising its role actively with respect to performance.

While there may be no simple way to further improve the performance of PNG’s superannuation sector, there is a clear first step — which would be to shine the spotlight on the performance of the two big funds.

There are only four superannuation funds in PNG: the two big ones we’ve been discussing, the new entrant PacSuper, and the small Defence Force Retirement Benefit Fund for members of the armed forces. It should be a simple matter for BPNG as superannuation regulator to compile the sort of comparative statistics we have presented in this blog for these four funds, or even just for the big two, and make them public. That would force both funds to defend their results, and to look for ways to improve.

No doubt Sir Mekere’s 2000 superannuation reforms were a success. But a new round of reform is needed to improve superannuation performance. It should begin with benchmarking.

I would not say that the ‘best’ indicator of performance is the crediting rate. The crediting rate is a lagging, discretionary figure declared by the board (Superfund). It is a policy decision, not a pure market reflection of the funds performance. It is no secret that both funds have been buoyed over the past decade by an unhealthy concentration of risk. Both funds are heavily reliant on BSP dividends and PNG Government Treasuries (T`Bills and GIS). This creates a circular dependency as the funds’ performance is tethered to the very government debt they are forced to buy because of FX shortages. True performance should instead be measured by Risk-Adjusted Return on Assets (ROA). The crediting rate model is outdated; most Australian supers have scrapped it for the benchmarking model, as the article suggests.

Great article. Please get in touch with me, i would like to share some white papers on super annuation reforms in PNG, written in association with ASFPNG. My mobile number is 7494 1110. Regards, Eric Kramer