Picture this: a migrant worker is about to send US$200 home to the Philippines. They face a seemingly simple choice between two money transfer operators. One offers PHP59 per US dollar, matching the official rate. The other offers PHP56. This three-peso difference might appear minor but for their family it means receiving either PHP11,800 or PHP11,200 — a PHP600 gap that equals an entire day’s minimum wage in the Philippines. It could be the difference between meeting basic needs or falling short.

This small-scale scenario mirrors a massive national challenge. Every year, over US$650 billion in remittances are sent worldwide, sustaining millions of families by covering basic needs, healthcare, and education. A migrant sending money home might receive vastly different amounts depending on the transfer operator, with losses adding up to billions globally due to unfavourable rates. Greater transparency in remittance pricing is crucial, as even small cost reductions can profoundly improve financial stability for families and communities.

The Remittance Prices Worldwide (RPW) report by the World Bank has been instrumental in advancing transparency in global remittance markets. Launched in 2008, this quarterly report monitors the cost of sending remittances across 367 corridors and serves as a key reference for tracking progress toward the G20’s 3% cost reduction target. While RPW provides essential macro-level insights through quarterly updates, it can miss short-term price fluctuations that affect real-time consumer decisions.

This blog draws on my ongoing research tracking daily foreign exchange (FX) margins — the small percentage differences between official exchange rates and actual exchange rates used in remittance transactions — from Monito and Wise for five countries in the East Asia and Pacific region: the Philippines, Indonesia, Thailand, Vietnam and China. Over a four-week period, I tracked digital and cash rates across these platforms to explore how market competition, platform incentives and provider behaviour influence remittance costs. While Monito and Wise aim for transparency like RPW, their near-daily data offers finer granularity and can uncover pricing dynamics that quarterly averages obscure.

Despite the central role remittances play in many economies, research on how comparison platforms influence user behaviour remains limited. A 2024 working paper by Eduardo Nakasone, Maximo Torero and Angelino Viceisza finds that while 10–28% of migrants display habitual preferences, more than half are open to switching providers when given comparative data. This highlights the potential for platforms like Monito and Wise to promote competition and lower costs. Yet, the limited research in this space points to the need for more work to assess how these tools can most effectively support financial inclusion and transparency.

One striking pattern in the data collected is the variation in FX margins not just across countries, but within platforms. These differences often stem from promotional campaigns, money transfer operator platform partnerships and internal pricing incentives. In some cases, a provider appears cheaper on one platform and more expensive on another, depending not only on market competition but also on how frequently each platform updates its rates. This suggests that observed margin differences may partly reflect the timing of updates rather than active price changes, an issue also raised in joint Development Policy Centre and Asian Development Bank Institute research, which argues that averages often conceal meaningful differences beneath the surface.

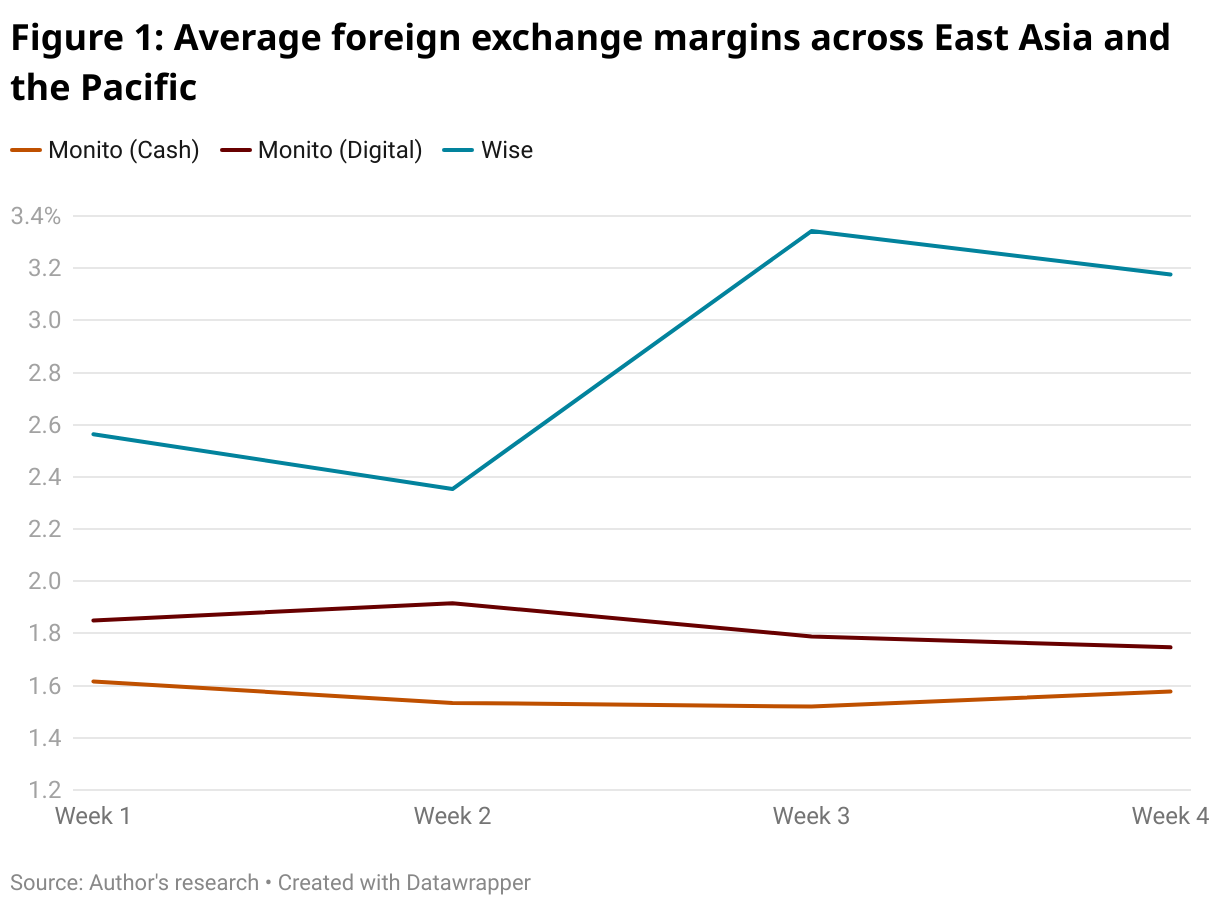

Foreign exchange margins also fluctuate over time and across providers. While this isn’t surprising — exchange rates shift regularly — the observed volatility can reflect more than external market forces. It can indicate how transfer firms hedge risk, respond to rate swings or apply strategic markups. As shown in Figure 1, Wise displayed both higher and more volatile margins than Monito, whose digital and cash rates remained relatively stable. Another key finding of this research was the variation in FX margins across countries within the East Asia and Pacific region. During the observation period, Wise’s overall margins ranged from 2.35% to 3.34%, with Indonesia showing the widest swing — from 2.37% to 3.41%. In contrast, Monito’s digital transfer margins in Thailand were more stable and consistently lower, fluctuating between just 1.28% and 1.96% over the same period.

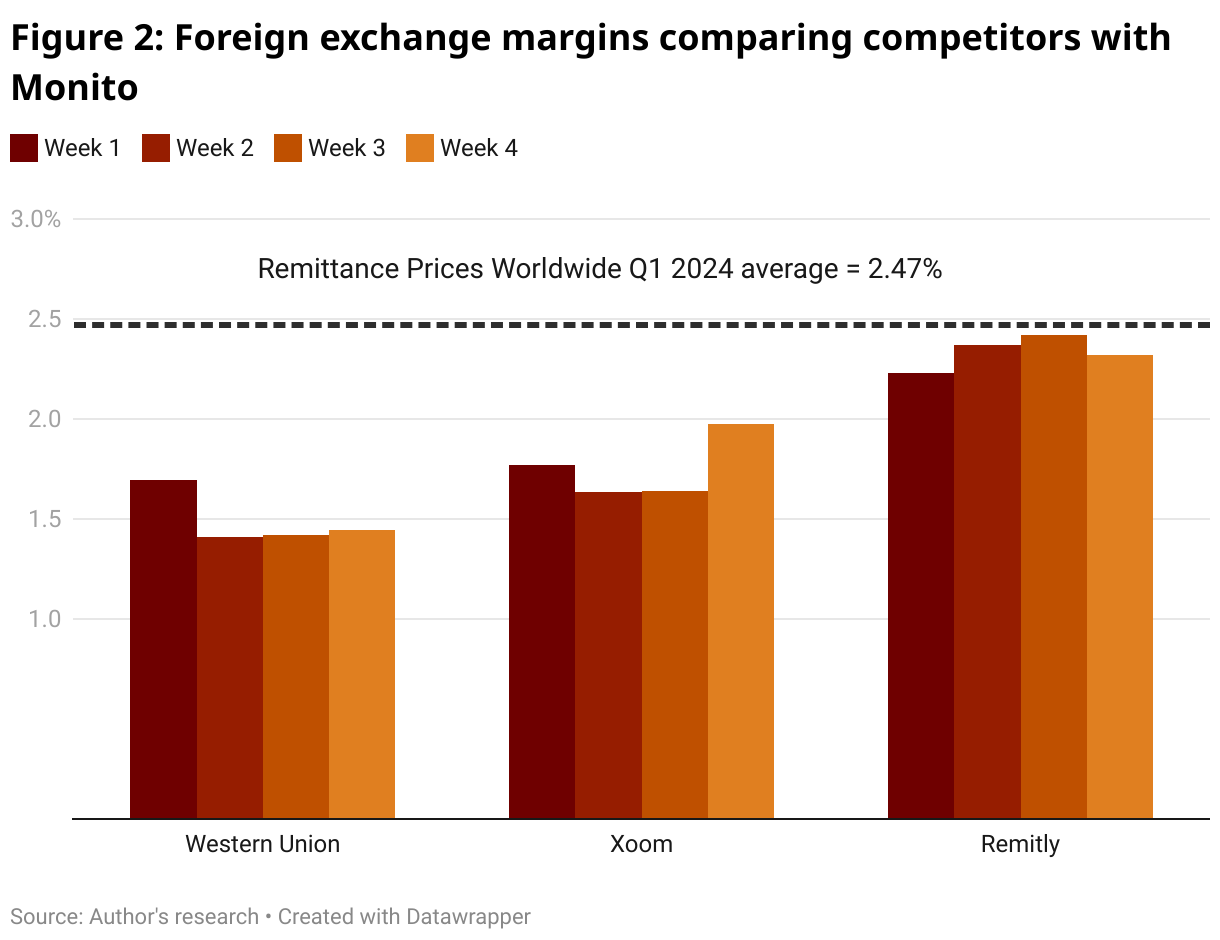

Zooming in on provider-level trends, Figure 2 reveals distinct pricing behaviours. Xoom’s margins showed more dramatic week-to-week swings, suggesting dynamic adjustment strategies, while Western Union maintained steadier, lower rates. Remitly hovered just below the 2024 RPW Quarter 1 global average of 2.47% for the three providers but stayed under the G20 (and UN SDG) target of 3% throughout the period — highlighting modest but meaningful progress toward affordability. Still, this variation shows that even providers meeting global benchmarks can employ different pricing models based on risk tolerance, target customers or platform-specific agreements. While these graphs offer a useful snapshot, more detailed visualizations (for example, provider-level box plots or scatter charts) could better reveal underlying dispersion and markups. Future iterations of this research will incorporate such views to unpack volatility in greater depth.

Ultimately, this analysis demonstrates that real-time, platform-specific tracking can complement RPW’s quarterly benchmarking by capturing rapid shifts in remittance pricing. This enhanced granularity, combined with comprehensive market analysis, gives us powerful new tools to drive down remittance costs. The impact is profound: every reduction in fees means more children can go to school, more families can afford healthcare and more communities can build resilient futures. In an interconnected world where over 200 million migrants support their families through remittances, making these transfers more affordable isn’t just about percentages — it’s about transforming lives.