The goods and services tax (GST) is an important revenue source for Papua New Guinea. It was introduced in 1999 to replace the provincial sales tax and reduce import tariffs. Since 2012, GST has contributed 15% of national government revenue and 80% of provincial revenue. Given GST is a broad-based tax, it is also a good proxy for economic activity. In this post, I examine how GST has performed since 2010.

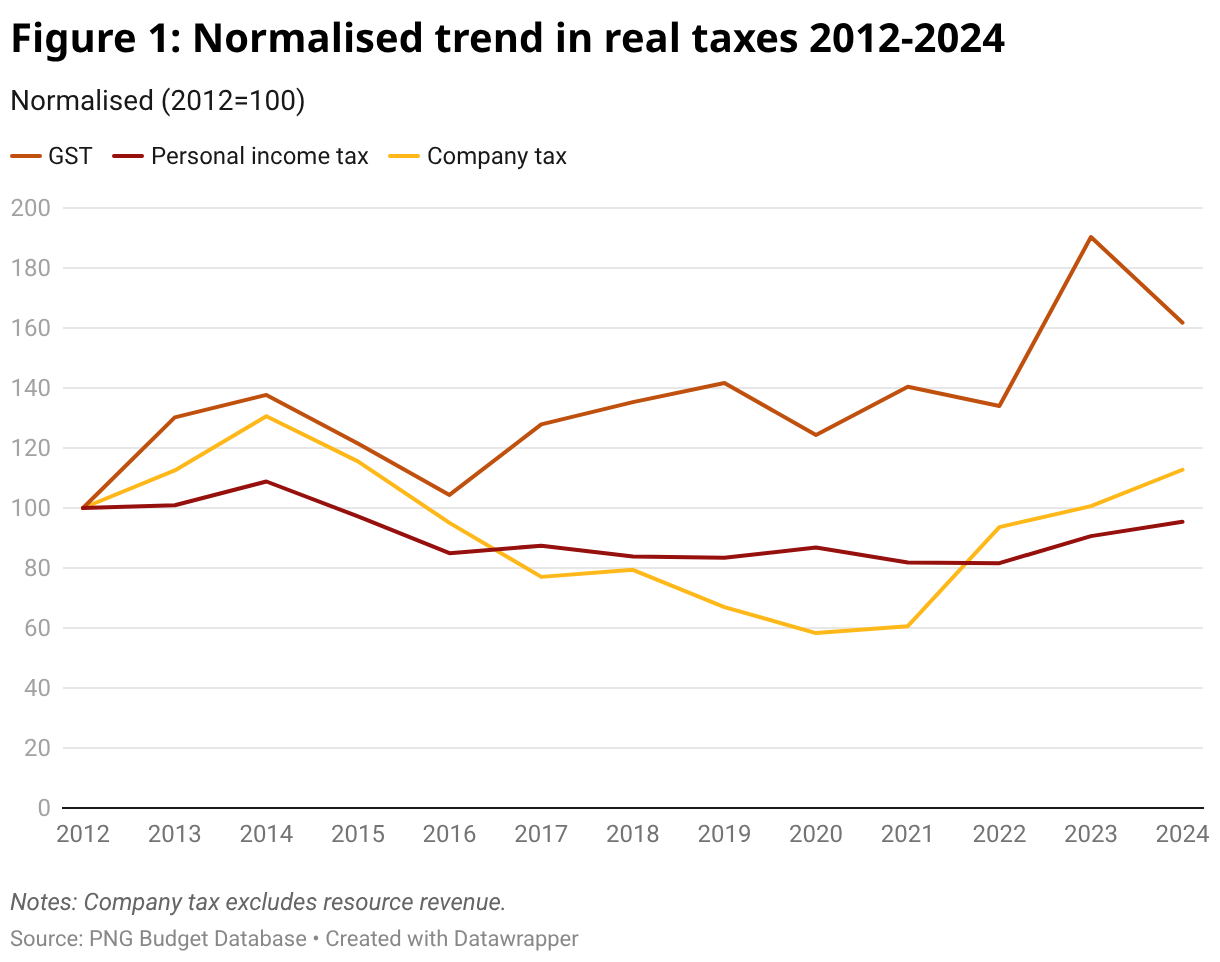

When the performance of PNG’s three broad-based taxes is compared, the divergence is striking. The chart below shows normalised trends, beginning in 2012, for GST, personal income tax and company tax (excluding taxes on resource companies). GST grew rapidly between 2012 and 2014 driven by the final years of the resource boom. A commodity price slump and drought caused GST collections to fall in 2015 and 2016 before recovering. GST fell again in 2020 due to the pandemic and then in 2022 due to the GST exemption on fuel. Treasury attributes the sharp increase in 2023 to the removal of the 2022 fuel exemption and improved tax compliance, and the fall in 2024 to the widespread riots and looting during Black Wednesday.

In contrast, company and personal income tax have performed poorly since 2012. Company tax peaked in 2014 at 31% above its 2012 level, but then it fell and, despite a subsequent recovery, in 2024 was 18% below its 2014 level. Personal income tax fell since 2014, and despite increasing since 2022, was still below its 2012 level in 2024. The stagnation in both taxes reflects the bust of PNG’s economy following the end of the resource boom in 2013.

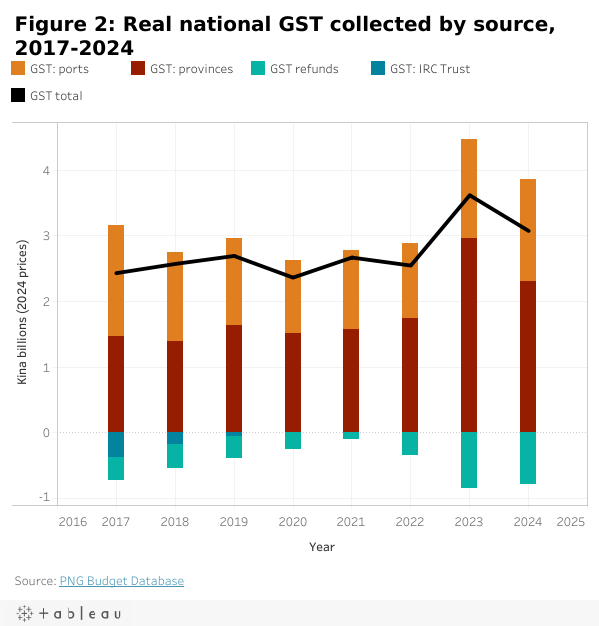

Why did GST do so much better than the other two taxes? GST is administered by PNG’s central tax agency, the Internal Revenue Commission (IRC). It collects GST on domestic sales in the provinces and receives GST collected at the international ports by the PNG Customs Service (GST on imports). Final GST revenue is realised after refunds are deducted and a share is retained in an IRC trust (only active up to 2019). Up until 2021, the IRC made GST refunds increasingly difficult to obtain, causing refunds to fall before they began increasing again.

Several reforms have also affected GST collections, most positively. In 2018, the GST zero-rated status for educational institutions was removed. The next year saw the GST zero-rated status also removed from suppliers to resource companies. In 2020, companies were prohibited from offsetting GST refunds owed against personal income and company tax obligations. Responding to inflation in 2022, GST on fuel products was exempted for six months. Then in 2024, firms were allowed to remit the GST they owed directly to the IRC (in the past, this would be paid to their suppliers who would then claim input credit). In 2025, basic goods were zero-rated.

As the figure below shows, GST collections at ports fell steadily between 2017 and 2022, before picking up in 2023, while GST collected in the provinces has increased since 2020, and has gone from being less than half of total gross GST collections to almost 60%. This doesn’t mean PNG has become less import-dependent. Rather, it reflects a rise in GST deferrals on imports, where GST is charged not when goods are imported but when they are sold by a retailer. According to budget documents, deferrals on import GST rose from K6 million in 2019, in real terms, to K317 million in 2022 (Treasury ceased reporting these from 2023). There doesn’t appear to be a limit to the size of import GST deferrals permitted.

Of the total that government receives, GST from imports and 40% of provincial GST is kept by national government. The remainder of provincial GST (60%) is remitted to the provinces. National government still retains the lion’s share of total GST collected, but its share is declining, from 72% in 2017 to 65% in 2024. Adjusting for inflation, GST retained by national government only increased by 10% in these years, whereas GST to provinces increased by 53% (total GST growth was 23%). So, although GST is the one broad-based tax that has performed reasonably well, it has brought only limited benefit to national government.

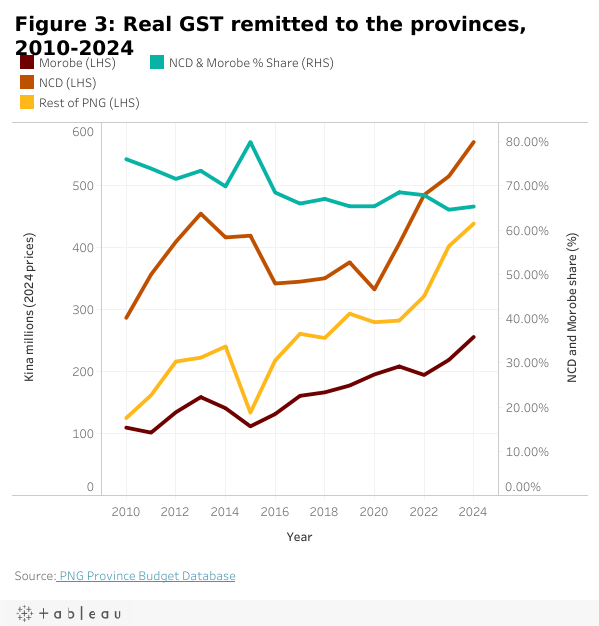

In the provinces, National Capital District (NCD) and Morobe have historically raised more than the others combined. But their share has fallen since it peaked in 2015 at 80%, to 65% in 2024. In fact, GST in NCD was larger than that collected in both Morobe and all provinces till 2016. These trends are positive, indicating GST outside PNG’s two main cities has grown over time.

All told, GST grew in a period when both company and personal income taxes stagnated. This growth has been broad based reflecting economic growth outside PNG’s two main cities. This has been great for the provinces, but not so good for the national government, which has had to contend not just with stagnant corporate and personal income tax but a declining share of GST over time.