Howard Bamsey has just been appointed as the second Executive Director of the Green Climate Fund (GCF). Bamsey is a distinguished Australian public servant, well-known internationally as an indefatigable climate change negotiator and also for his stint as Director-General of the Global Green Growth Institute, which happens to be headquartered, like the Green Climate Fund, in Korea.

He has quite a job ahead of him. While the GCF is technically about five years old, having been established by decision of the parties to the UN Framework Convention on Climate Change (UNFCCC) in December 2011, it’s really still in its infancy. It doesn’t have much pocket money, has to share a room with some competitive older siblings and doesn’t know what it wants to be when it grows up.

Pocket money

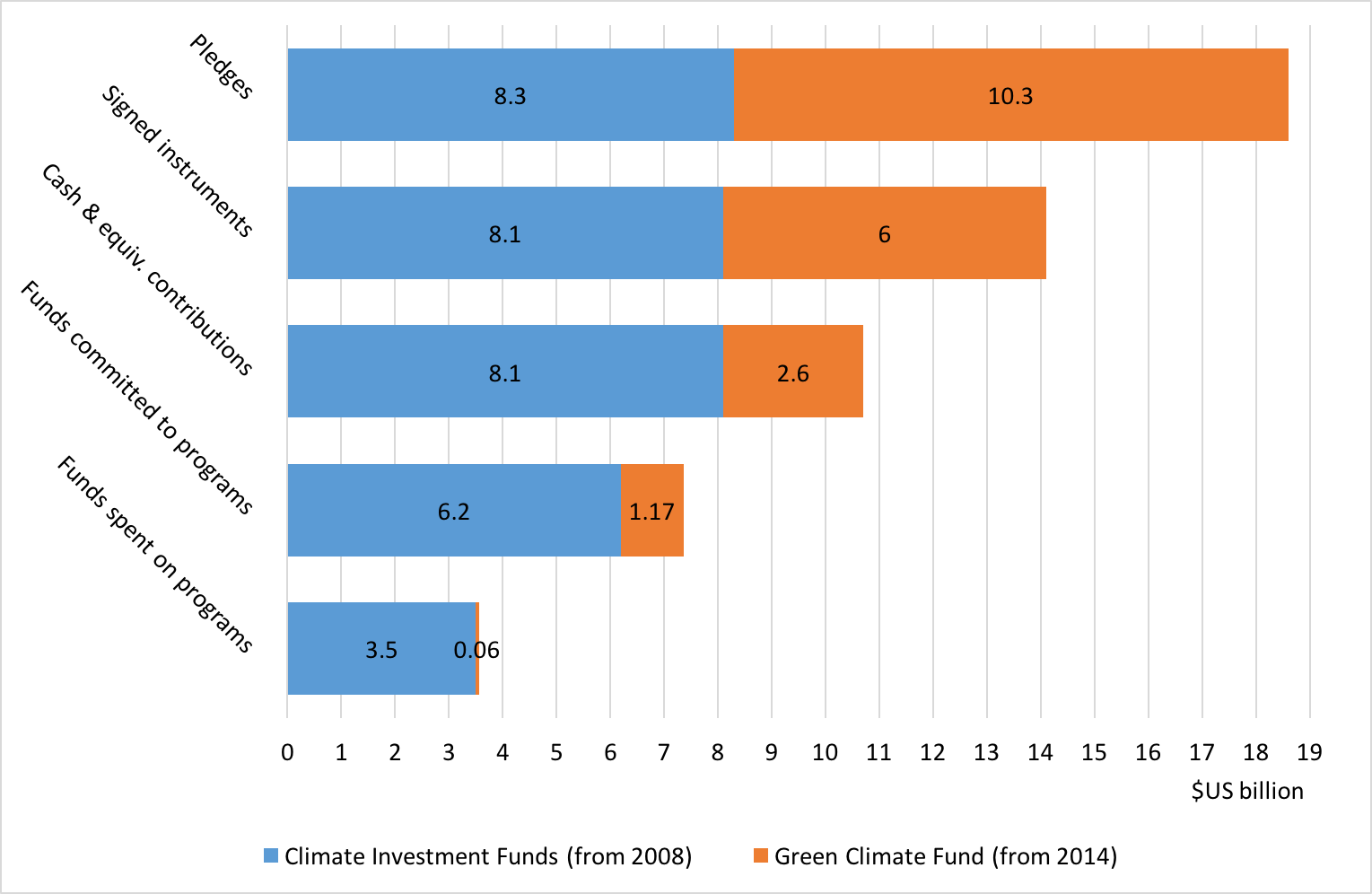

The GCF is not flush with money. The immediate problem isn’t a lack of pledges. It is often suggested that the amount of money pledged to it in late 2014, $10.3 billion to be allocated over several years, is derisory by comparison with the $100 billion per annum mooted in Copenhagen.[1] In fact, the GCF was and is not intended to be the vehicle for all this funding, or even a majority of it. It was always quite clear that GCF would hold only some small fraction of the aspirational total, with the rest coming from other development financing institutions, aid agencies and the private sector. The GCF sought $10 billion in initial resources in 2014, and promptly received it—rather a good outcome.

The problem is getting the pledges into the bank. So far, the GCF has been able to convert about $6 billion worth of pledges into signed instruments of commitment, but it can’t actually commit funds to programs until it has cash, or cash-equivalent commitments like promissory notes, to back them. At this point, the GCF has cash-equivalent contributions, and therefore a total commitment capacity, of only about $2.6 billion.[2] The GCF has frequently been criticised for the rate at which it is committing funds and had committed less than $170 million to programs up to mid-2016. However, following the last two meetings of its board, that figure has risen to almost $1.2 billion in grant and loan financing for 27 projects (another 30+ projects in the pipeline are worth a further $2.7 billion).[3] Considering its present commitment capacity, that looks like reasonable progress—at least from a simple money-in-motion perspective.

Older siblings

The GCF’s twin older siblings, born in 2008, are the Clean Technology Fund (CTF) and the Strategic Climate Fund (SCF), known collectively as the Climate Investment Funds (CIFs). The CTF finances large-scale mitigation projects and the SCF makes targeted investments in adaptation, reducing emissions from deforestation, and renewable energy. The CIFs collected pledges of $8.3 billion up to 2014, with commitments currently totalling $6.2 billion and expenditure $3.5 billion. Like the GCF, the CIFs are structured as World Bank trust funds (‘financial intermediary funds’, to be exact). They can channel resources to any of six multilateral development banks, though not to other agencies.

Unlike the GCF, the CIFs are managed by an administrative unit within the World Bank, and are not creatures of the UNFCCC. They operate under a ‘sunset’ clause which, though vague, is meant to ensure that they progressively cede the field to the GCF now that it exists.[4] The GCF, in other words, is meant to be a continuation of the CIFs under UNFCCC oversight, and in fact many of its features—including its ‘equal voice’ governance arrangements and its private sector window—are taken from the CIFs.

The three siblings combined have drawn pledges of some $18.6 billion to date.[5] Their current financial status is summarised in Figure 1.

Figure 1: Financial status of major climate funds

Data sources: World Bank reporting on financial intermediary funds; organisations’ web sites.

The CIFs should now, in principle, be closed to new pledges, which should flow instead to the GCF. Most future commitments to programs should happen on the GCF’s account, though the CIFs do have a little under $2 billion in remaining commitment capacity. However, the CIFs will continue disbursing substantial amounts of funding until somewhere between 2022 and 2024. They will spend around $1 billion a year on average over the next few years and then perhaps $600-700 million a year thereafter until exhausted. They will not disappear overnight.

In addition, to the annoyance of some observers, it appears that the board and management of the CIFs do not consider the sunset clause to have been triggered—see, for example, the headline of this and the general tenor of this.[6] Nor is it clear that the administrative and technical apparatus put in place for the CIFs within the World Bank, lean though it is, has yet been replicated within the GCF, or that the GCF’s governance arrangements would allow such an apparatus to operate effectively.

For these reasons, sibling rivalry is hardly to be ruled out. As was noted by the Independent Reference Group on the Independent Evaluation of the CIFs some time back (2014), ‘A strategic vision and high-level guidance are urgently needed to craft a working relationship between the CIF and the GCF’.[7] In the absence of this, small wonder that the recently released report of the Center for Global Development’s High-Level Panel on the Future of Multilateral Development Banking refers only dismissively to the GCF, and calls for the World Bank to be provided with some $10 billion per annum to support mostly grant-based investments in global public goods, including climate change mitigation.

Vocational quandary

Possibly the hardest question facing the GCF is what it is for. Hardest because this is a question that the CIFs did not manage to answer clearly, except to claim a special role in financing ‘transformative’ investments.[8] (The GCF uses the same term liberally in its puffery.) CTF investments have tended in practice to go where the more entrepreneurial staff of various multilateral development banks wanted them to go, and the allocation of SCF investments has been heavily influenced by considerations of inter-country equity. The GCF, which in principle will have more resources and a longer life, will need to avoid such distortions if it is to give substance to the ‘transformative’ claim and thereby carve out a distinctive role among the numerous sources of climate-related finance.

The problem is compounded by the fact that the GCF is expected to allocate half of its resources to adaptation, and the fact that any climate change fund operating under UNFCCC auspices is liable to be perceived, at least to some extent, as a reparations mechanism. Where funding is to be used for essentially local purposes, or is seen as compensation for unavoidable climate change, inter-country equity will naturally loom large. Indeed, this already seems to be happening, judging by the allocation choices made in relation to the first $1 billion.

The GCF essentially faces a choice between allocating its resources to a broad and somehow representative group of developing countries or allocating them to investments likely to have the greatest impact at the global level. On the mitigation side, surely it wants to do the latter, and the question is how to avoid resource capture by special interests. The obvious way to do that, though one that is unlikely to be unpalatable to the GCF’s constituency-based board, would be to run a series of reverse auctions—committing to purchase so many megatonnes of emission reductions from the countries able to supply them at the lowest cost. It would be up to countries, generally in partnership with multilateral development banks or other third parties, to develop the projects, programmes and related bids.

On the adaptation side, the benefits of GCF investments, no matter how effective, will for the most part not be global in nature. It could be argued that the GCF, and for that matter the CIFs, should never have entered the adaptation business—after all, the Global Environment Facility (GEF) deliberately avoided it at the outset, owing to the local nature of its benefits.[9] But the GCF’s adaptation mandate will not just go away, and could in fact usefully be pursued by interpreting it as a mandate to deliver adaptation capacity to as many people as possible, rather than as many governments as possible. For adaptation no less than mitigation, the reverse-auction allocation strategy proposed above would deliver the biggest impacts at the lowest costs, thereby increasing the chances that investments would be transformative. It hardly matters if all 1,000,000 people whose lives and livelihoods are protected by a flood control program happen to be in one country rather than 10. The total utility generated is the same.

In short, linking allocations to specified, large-scale outcomes and selecting suppliers on the basis of least cost would constitute a sensible way of homing in on transformative investments, and would be a genuinely distinctive strategy. Inter-country equity would go out the window, but there is no shortage of development agencies, funds and programs allocating climate-related finance on the ‘everybody gets a prize’ principle.

Welcome to the office

So these are the challenges Bamsey faces, together with his board—of which Australia’s Ewen McDonald is presently co-chair. He and the board will have to obtain more pledges and convert them more efficiently into bank deposits (while maintaining a measured, not frenzied, commitment rate). He and they will need to make up for lost time in working toward an accommodation between the GCF and the CIFs, and between the two underlying administrative structures. And, above all, he and they will need to give substance to the notion that the GCF, as one mechanism among many, has a distinctive and transformative role to play in climate change financing. And all that while working on reclaimed mudflats. Here’s hoping the pay is handsome.

Robin Davies is the Associate Director of the Development Policy Centre.

[1] All figures in this post are in US dollars.

[2] This is based on information published on the World Bank’s financial intermediary funds web page, which is said to be current as at October 2016. Similar information is contained in Annex III of this recent GCF board document. It should be noted that the GCF’s web site claims ‘signed’ contributions of $9.9 billion. It is unclear what this means, given that the World Bank as trustee recognises only $6 billion in signed contributions at this time. The GCF counts the whole US pledge of $3 billion as ‘signed’, though it is not in fact certain that it will materialise in full. See, for example, this statement of strong opposition from 110 Republican Members of Congress in November 2015, and this statement along the same lines from 22 Republican senators in March 2016.

[3] The GCF is able to provide grants, loans, equity and guarantees—and indeed must allocate some proportion of its resources in loan form since part of its contribution base has been provided as capital rather than grants.

[4] According to similar sunset clauses in the governance frameworks for the two CIFs, each fund will ‘conclude its operations once a new financial architecture is effective’. However, an escape clause allows that the CIFs might continue to operate ‘if the outcome of the UNFCCC negotiations so indicates’.

[5] This post considers only the CIFs and the GCF since they are by design, if not in reality, essentially the same mechanism and by far the most important dedicated multilateral climate change financing sources. There are many other, smaller multilateral climate change funds and programs, such as the Kyoto Protocol Adaptation Fund, the GEF’s Special Climate Change Fund, the Forest Carbon Partnership Facility, and so on. In addition, the GEF invests one-third of its resources, around $300 million per annum, in climate change mitigation activities.

[6] The independent evaluation of the CIFs conducted in 2014 found that they had not ‘clarified their interpretation of how and when to exercise the sunset clause, introducing uncertainty into their operations’ (p. VIII). The Independent Reference Group on the same evaluation commented that, ‘the lack of clarity on when the so-called sunset clause will be invoked … challenges the CIF’s legitimacy. Lack of alignment in the governance systems of the CIF and other UNFCCC related funds makes the issue complex, and yet it is surprising to note the lack of clarity on the sunset clause, given that both the CIF contributing countries and recipient countries are stakeholders and decision-makers of the GCF’ (p. XVII).

[7] See here, p. XVII. According to this GCF board document, an initial round-table ‘dialogue’ will be held with other climate finance delivery channels and funds in December 2016, and is intended to be held annually thereafter.

[8] On this point the independent evaluation found that, ‘Some projects are plausibly transformational; others lack a convincing logic of transformation and impact’ (p. XIV). The Independent Reference Group commented that, ‘the evaluation report’s descriptions of the failure of many investment plans to articulate a clear theory of change, the frequent lack of clarity regarding how subsequent projects fit together with each other and with other processes in a coherent strategy, and the gap between investment plan aspirations and project-level implementation … are causes for concern’ (p. XVIII).

[9] In an instance of mandate creep, the GEF later accepted a very limited role in the management of grant resources for adaptation.

Thanks for the very informative article. One question: how do you think Pacific countries would fare if the GCF does not adopt some kind of ‘inter-country equity’? My own view is that it would seem that their “numbers” – in mitigation (C02 reductions) or adaption (total # people saved) – would never really amount to an attractive proposal to the GCF. And that would discriminate against Pacific countries, who have very real and urgent climate issues to address.

Your thoughts appreciated!

Of course you’re right, Jay, that small states would be unlikely to get a bite of the GCF under any allocation arrangements that privileged tonnes of emissions avoided or numbers of people protected from climate-related harms, and therefore gave no weight to sovereignty. If an implementing agency (like the ADB!) were to find a clever way of sweeping them all under a single regional adaptation bid, and could get the costs low enough, maybe. Mitigation funding would certainly be beyond reach.

But I don’t think that’s such a terrible thing given that the GCF houses and will always house only a minority of the available funds. I think too much angst has been devoted to the question of how small states might access big funds. Perhaps it’s better to simplify life for the big funds, and let them try to give substance to the claim that their investments are transformative, while making separate and more local or regional arrangements for small island states.

Thanks for your response Robin. I certainly agree the GCF is only one avenue of climate finance support and the $100 billion everyone is looking for needs to come from many sources including the private sector, bilateral and multilateral donors. But the implied suggestion that Pacific can look elsewhere for climate funds generates several issues worth considering. Two issues that I find particularly compelling are:

1. The global community doesn’t really want more climate funds. You will recall a few years ago that many donors were criticised for their ‘proliferation of funds’. The criticism’s storyline was that there were too many special interest or regional funds were creating inefficiency for recipients. Perhaps to some extent that is why we ended up with one humongous global fund – the GCF. I don’t think this issue has gone away and for the foreseeable future there will be little appetite for setting up a ‘Pacific Climate Fund’.

2. The GCF offers a development opportunity that donors can rarely provide: direct access to climate funds. And provides them with a kind of self-determination they find very attractive. My discussions with Pacific leaders lead me to believe it is not just about the money, it is to some extent about independence.

I agree that the GCF’s ‘one fund for all’ approach is very ambitious. But the alternative ‘one fund for some’ is – at the moment at least – even less appealing.