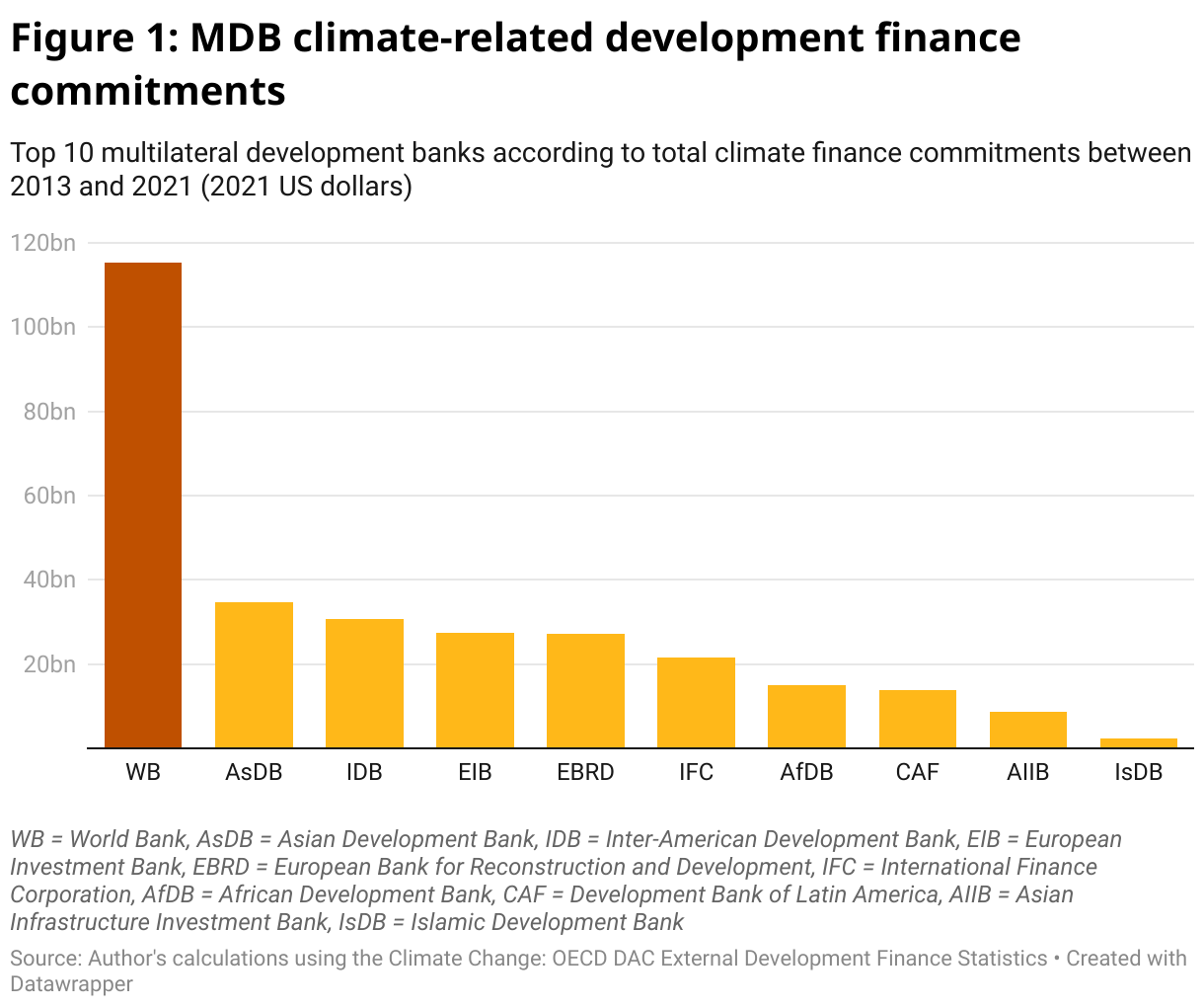

Multilateral development banks (MDBs) made 45% of all climate finance commitments between 2013 and 2021. Among them, the World Bank is far and away the single largest provider of climate-related development finance in the world (Figure 1) – MDB or otherwise. But size is not everything. While the World Bank’s climate finance commitments are highly concessional and focused on adaptation, other MDB peers commit a greater proportion of climate finance to least developed countries (LDCs) and as a share of their overall financing. The additionality of the Bank’s climate finance is also questionable, at least from publicly available data.

Concessionality is a key positive for climate finance committed by the World Bank: 46% of its total climate finance commitments made between 2013 and 2021 were considered concessional. This is partly due to the relatively large use of grants (11% across 2013-2021) by the Bank to provide climate finance. Only the African Development Bank (AfDB) provided a greater proportion of grant funding (17%), and the World Bank remains far ahead of the next most ‘generous’ MDB, the Asian Development Bank (AsDB, 4.8%).

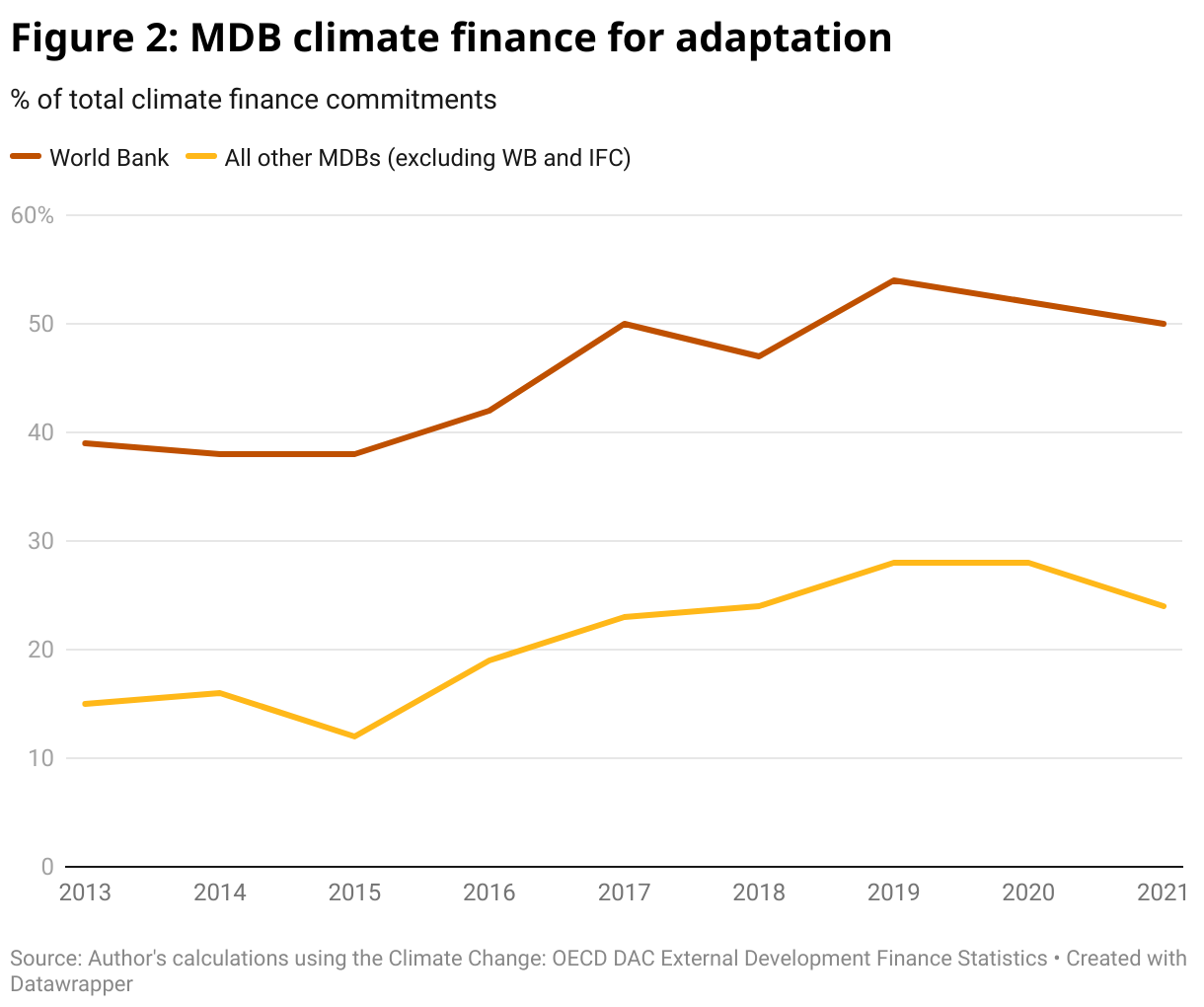

Another strength of the World Bank is the consistently high share of climate finance directed towards adaptation (Figure 2). From 2013 to 2021, commitments to adaptation grew relatively consistently and in total amounted to 47.6% of climate finance commitments from the World Bank. This comes very close to the Bank’s goal of allocating 50% of its climate finance towards adaptation, and is second only to the ratio achieved by the AfDB (49.5%). Success here seems to reflect clear linkages between economic development and adaptive capacity, as well as the advantages of the World Bank’s country-driven programming in responding to developing countries’ prioritisation of adaptation action.

The World Bank also provides a relatively high share of climate finance to countries that need it the most: 35% of its climate finance goes to Africa and another 47% goes to Asia, regions which have been identified as among the most vulnerable to climate change effects.

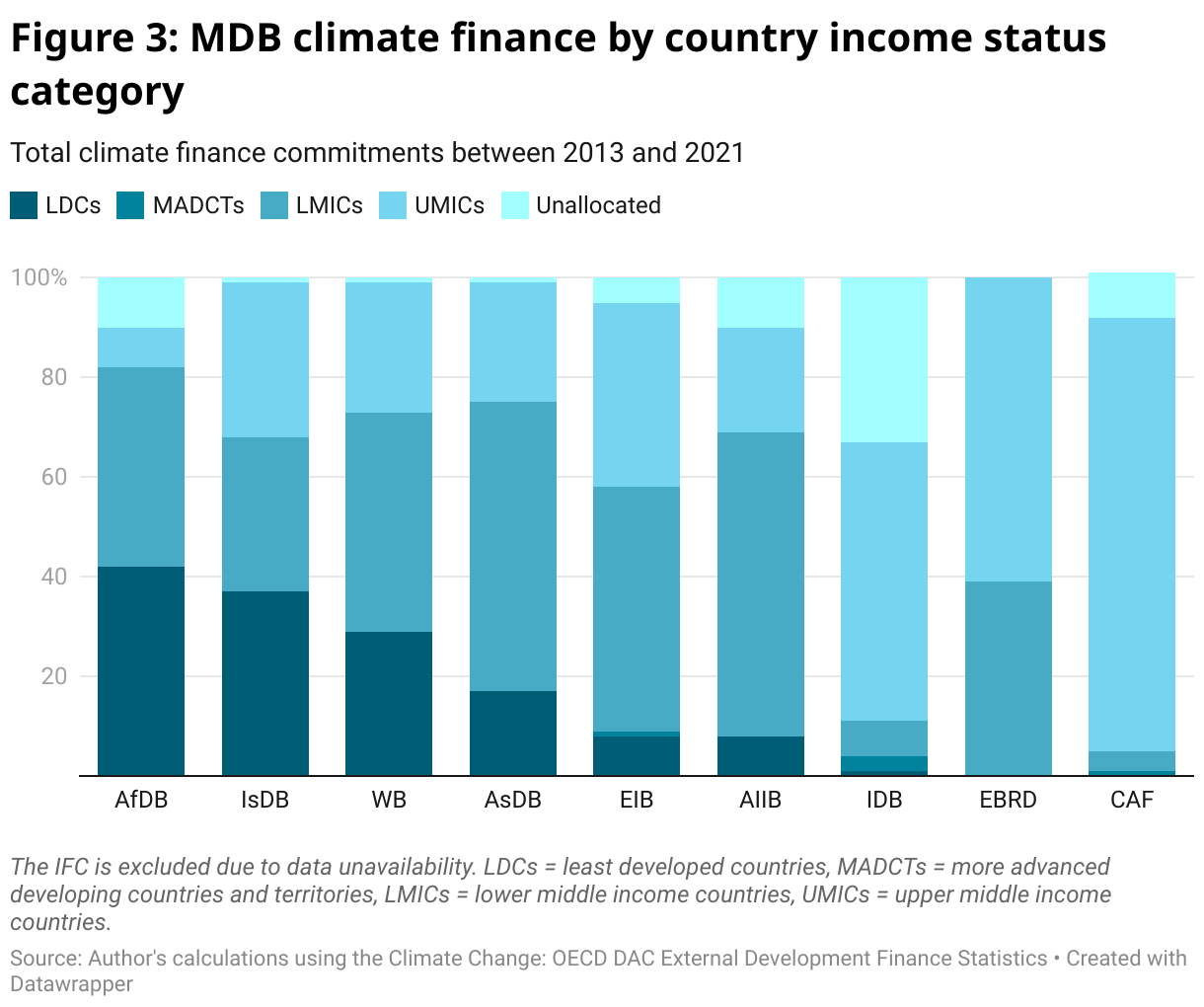

There is however still some room for improvement. While middle income countries undoubtedly require climate finance to decarbonise and adapt to climate change, LDCs have been promised less than 30% of total climate finance committed by the World Bank (Figure 3), despite being heavily exposed to climate change effects and more stringent fiscal constraints. In this respect, the World Bank falls behind peers including the AfDB and the Islamic Development Bank, but remains more targeted to LDC needs than other major MDBs including the AsDB and the European Investment Bank.

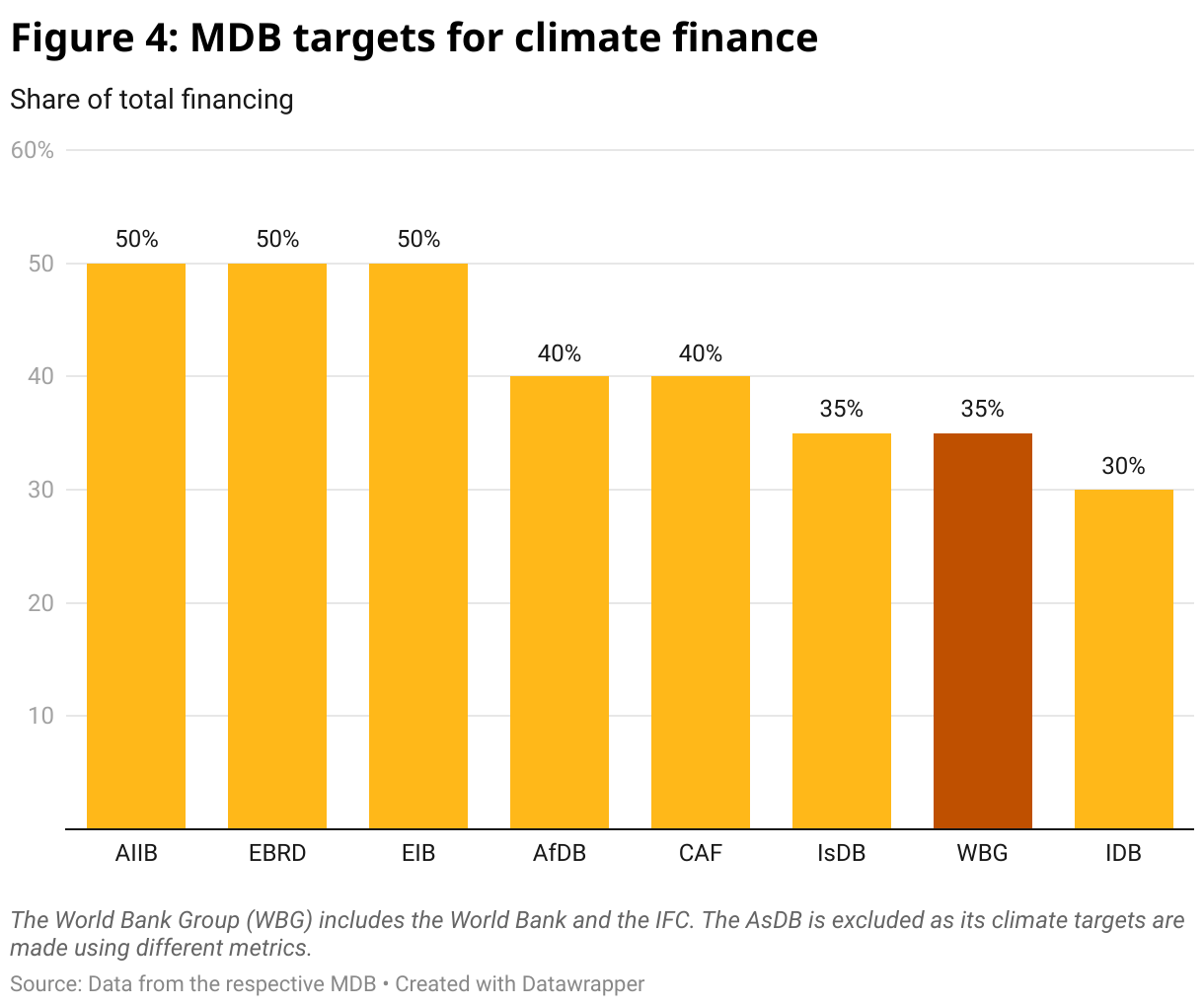

The World Bank also underachieves relative to its peers in the importance it places on climate action, as represented by the share of total financing. The Bank’s Climate Change Action Plan for 2021-25 has a goal of 35% of its development finance going towards climate action – an increase from the 26% average achieved in 2016-20. However, the Bank appears notably less aspirational than most of its MDB peers (Figure 4). While the AsDB’s goal appears larger at face value – with 75% of committed operations to support climate action over three-year rolling periods, and climate finance from its own resources to reach $100 billion between 2019 and 2030 – comparisons are difficult due to the different metrics in use (the AsDB is therefore excluded from Figure 4).

One explanation for the World Bank’s relatively unambitious target is the institution’s broad coverage across sectors like education and health as well as infrastructure, especially in comparison to other MDBs. This likely makes it harder for the Bank to prioritise climate action without reducing efforts in areas of development where synergies with climate action are less clear. Regardless, the implication is then that the Bank’s status as the largest climate finance provider is merely a function of its overall scale, rather than an overt emphasis in the institution on climate finance.

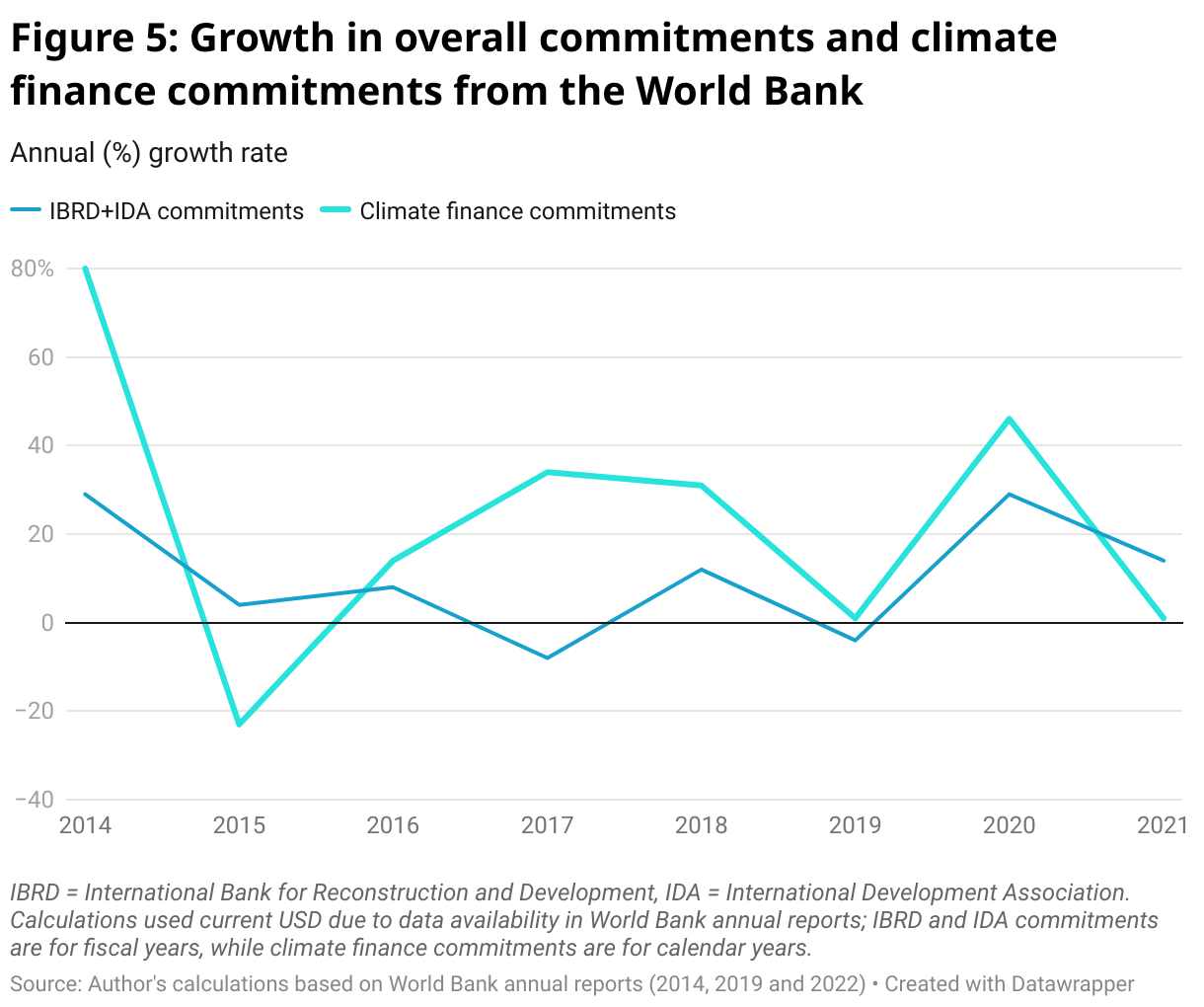

The additionality of the World Bank’s climate finance also remains unclear. The Bank’s climate finance commitments have grown faster than development finance commitments across the World Bank as a whole (Figure 5). It is difficult to establish whether this means that the Bank’s increased focus on climate has come at the expense of other development priorities; that the Bank has done a better job at identifying projects to fund that aid both development and climate action; or that more projects have been labelled climate-related without substantiation.

What, then, does this mean for the greater focus on climate change proposed in the World Bank’s evolution roadmap for its future operations? To do more and better on climate in the short run, the Bank’s first priorities should be to use new instruments to make better use of its existing capital, and improve transparency around disbursement rates and the effectiveness of the projects it finances. Moving forward, an explicit reference in the World Bank’s mission to climate change or global public goods more broadly, as well as a capital increase, would help ensure further climate finance from the Bank is genuinely new and additional.