The monetary policy statement (MPS) published by the Bank of Papua New Guinea (BPNG) in March this year places an unprecedented focus on the exchange rate, including a dedicated special feature article on the topic. While the exchange rate has been controlled by BPNG since 2014 when it moved from floating to rationing, the bank has never provided a formal justification of its approach. Nevertheless, the bank’s recent MPS and the special feature article indicate that concerns about depleting foreign currency reserves and potential inflationary effects of depreciation are significant factors behind BPNG’s reluctance to release more forex to the market. In this blog, we explore some of the views put forward by the bank in the context of the IMF program PNG has recently agreed to.

Foundationally, BPNG suggests in the special feature article that the “fundamental structural issue” that causes low inflows of foreign exchange into PNG is project development agreements negotiated between the government and resource companies. The bank also publicly criticises the government’s use of the Temporary Advance Facility, stating that it has resulted in high liquidity that has “render[ed] the implementation of monetary policy challenging” (MPS, page 15) and will allegedly lead to higher import demand in the foreign exchange market and declines in international reserves.

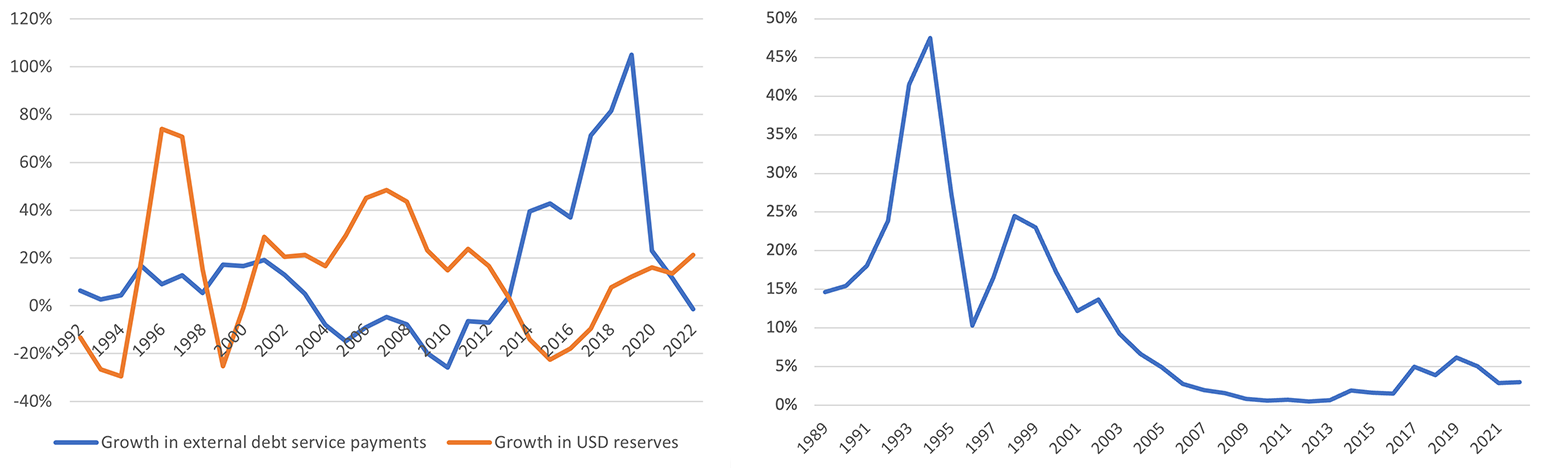

BPNG also notes in the special feature article that “the current level of reserves is still lower than the historical level achieved in 2012, and therefore the Bank is very cautious of running down the reserves” to supply more forex to the market. PNG did experience a long and significant decline in reserves after the boom (Figure 1). However, reserves are now at similar levels to 2012; when expressed in months of import coverage, reserves are almost twice as high as they have been historically. The latter phenomenon is due in large part to the import compression effect of rationing in recent years.

Figure 1: Total foreign exchange reserves held by BPNG

Left axis, USD millions; right axis, months of imports

Another risk that BPNG outlines in the MPS around supplying more foreign exchange is that “the recently accumulated reserve is pre-committed to meet the future demand for external public debt servicing”, following the government taking on more external debt. External debt repayments have risen significantly in recent years, surpassing the growth rate of reserves (Figure 2, left panel). However, it is also true that repayment liabilities remain small compared to BPNG’s holdings of foreign reserves (Figure 2, right panel). Even taking into account recent increases in debt servicing, the ratio remains lower than it has been since 2004, that is, before the boom began.

Figure 2: Growth in external debt servicing and reserves (left) and external debt servicing as a % of reserves (right)

This makes it harder to buy BPNG’s argument that external debt servicing is a major barrier to releasing more forex into the market. Although repayment obligations are expected to rise, especially with the repayment of the USD500 million Eurobond principal in 2028, it certainly appears that there is room for BPNG to supply more dollars to the foreign exchange market. Rather than looking like a threat, using more dollars to pay external debt obligations appears to be a reversion to more normal circumstances.

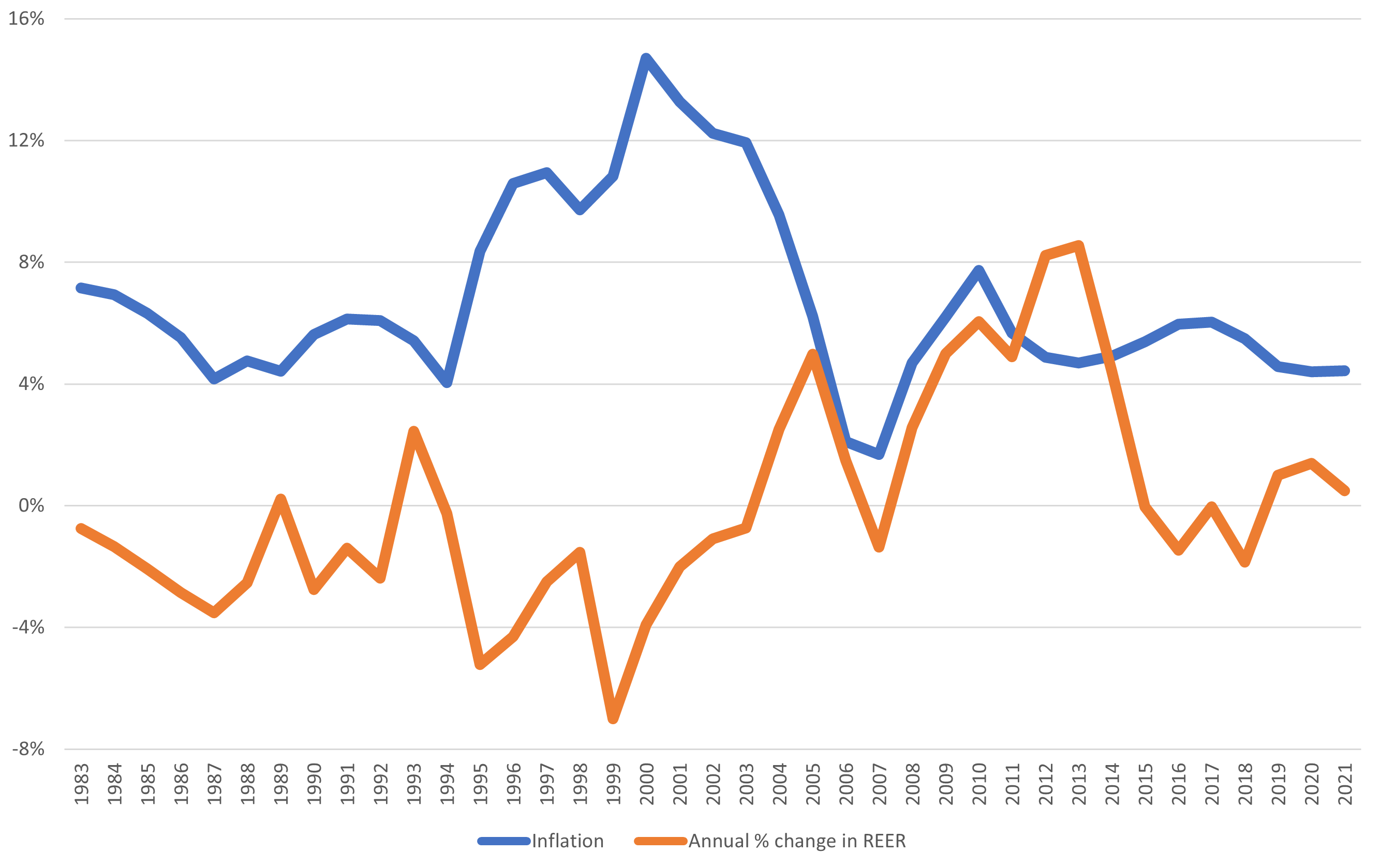

BPNG also expressed apprehension in the MPS (page 10) regarding the inflationary impact of allowing the exchange rate to depreciate. This could reflect concern around repeating PNG’s experience in the 1990s, where multiple large declines in the value of the kina were highly inflationary. However, not all depreciations in PNG’s history had the same effect (Figure 3). Inflation was relatively steady while the kina slowly depreciated in the 1980s, while the devaluation of the kina by 10% in January 1990 did not lead to a major spike in inflation.

Figure 3: Inflation and changes in the real effective exchange rate (REER)

Despite the apparent reluctance within the bank to move away from rationing, and whatever the root causes, the IMF program PNG has entered into makes it clear that BPNG is changing its thinking on these issues. The program requires BPNG (in consultation with IMF staff) to develop a roadmap towards kina convertibility and flexibility by August, and increase the monthly supply of foreign exchange to the market. In line with this, the special feature article attached to the March MPS concludes by saying that “the Bank will help address imbalance in the FX market and allow for kina exchange rate flexibility”. In recent months, BPNG has been reported to have released more dollars to the market than it normally does, and the kina which was unchanged against the US dollar for more than a year has been allowed to depreciate, albeit minimally (just 1%).

Clearly, much more will be needed, and presumably will be revealed once the roadmap has been prepared. The good news is that restoring convertibility does not necessarily jeopardise PNG’s ability to meet its foreign debt obligations, and therefore should not be seen as a barrier towards liberalisation. Furthermore, adopting a managed approach towards any devaluation of the kina may help alleviate concerns surrounding inflation.

Since the demand for Kina is low in the foreign exchange market, the Kina will certainly depreciate under the flexible regime. The immediate impact is that the price of imports will increase. Another wave of inflation is on the way for PNG, on top of the current high prices. Without any doubt, this will severely affect the welfare of our ordinary people. The idea of moving the Kina towards convertibility is good but timing in not right.