Recent media coverage has touted the rise of Chinese aid and lending as a threat to Pacific nations’ sovereignty and to the West’s influence in the Pacific. China, so the narrative goes, is aggressively lending to smaller nations who do not have the capacity to pay back the loans. Some commentators have even described such lending as “debt-trap diplomacy”, implying that lending forms part of an intentional strategy by the Chinese state to pressure Pacific island governments.

Political discussion in Australia seems to have shifted up a gear in response. As Foreign Minister, Julie Bishop made clear that she wanted Australia to continue to be the region’s “partner of choice”. And just last week, Labor leader Bill Shorten announced that a Labor government would set up an Australian Pacific infrastructure investment bank – an announcement he also framed in terms of Australia’s status as “partner of choice”.

But is it fair to claim that China is engaged in “debt-trap diplomacy” in the Pacific?

Most advocates of this argument have pointed to anecdotal evidence – high debt levels in Tonga, the case of the Hambantota port in Sri Lanka – rather than to hard data. In this piece, we look at international debt data to explore: (i) whether Pacific island countries are in debt distress, and (ii) whether this is the result of lending from China.

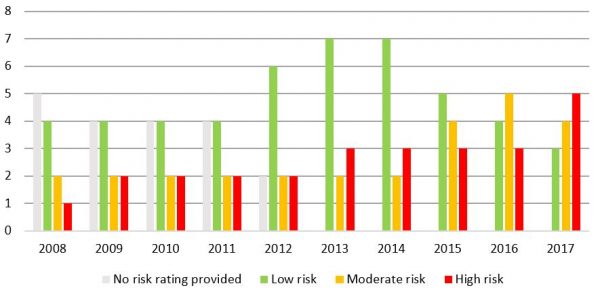

One issue we consider is whether Pacific island countries are at greater risk of debt distress than in the past. Using IMF and Asian Development Bank (ADB) risk ratings, we do see a rise in debt distress over the last five years (see Figure 1). We also see that over 40% of Pacific island countries are now classified as being at high risk of debt distress (see Figure 2, with countries singled out). So debt certainly appears to be a problem in the region.

Figure 1: IMF/ADB debt distress ratings 2008-2017 for Pacific island countries and Timor-Leste

Note: IMF article IV’s are not conducted every year – for these years we code the risk rating as the same in the most recent article IV report. All countries use IMF ratings except for Cook Islands, which uses ADB. Countries included are Fiji, Palau, Papua New Guinea, Solomon Islands, Timor-Leste, Vanuatu, Kiribati, Marshall Islands, Micronesia, Samoa, Tonga and Tuvalu. Tuvalu and Nauru are excluded as they were not IMF members in 2008 (they joined in 2010 and 2017 respectively), and no ADB risk ratings were found.

Figure 2: Debt distress rating by country (using most recent data)

Now for the second question: is this debt distress the result of lending by China?

The short answer is “no”.

Although it is the largest bilateral lender, Chinese lending comprises less than half of lending in any single country, with the exception of Tonga. In fact, half of those countries in the “high risk” category do not even recognise China (PRC), meaning they have no access to Chinese concessional finance (they instead have a relationship with Taiwan). China has also provided significant sums to countries where debt is not an issue (i.e. to countries classified as being at “low risk” of debt distress).

Let’s look at lending to the region in more detail.

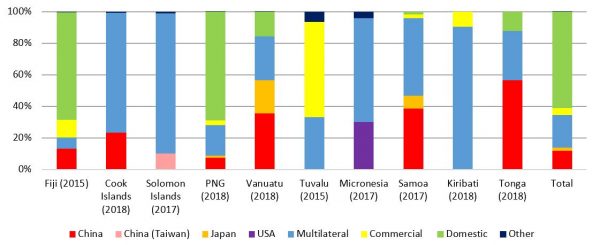

China holds around 12% of the total debt owed by Pacific nations, or US $1.3 billion out of US $11.2 billion in debt in the years in question (see Figure 3). Australia does not feature in this graph, as currently all its aid is given as grants rather than concessional loans – though it does contribute to multilateral funds that are lent to the region (e.g. by the World Bank).

Aggregate figures for the region are driven by Papua New Guinea and Fiji, the economies of which dwarf the rest of the Pacific. Borrowing by these two countries alone makes up 88% of the region’s total debt. However, in both countries, domestic debt dominates government borrowing – something that is explained in part by the activities of domestic pension funds.

Figure 3: Break up of national debt owed, by lender

Note: Timor-Leste, Nauru and Palau have been excluded from the graph as no information was found on the break down of their debt. Timor has signed up to China’s Belt and Road Initiative (BRI), and has committed to receiving loans for projects, but these have not yet commenced and Timor-Leste currently does not owe money to China. The total figure was calculated by converting all sums into US dollars and converting into 2018 prices using US CPI data.

It is only in Tonga, Samoa and Vanuatu that Chinese lending comprises over one-third of total debt. In Samoa, lending by the multilateral development banks has been greater than lending by China. In Vanuatu, which is not at high risk of debt distress, the rise in debt to China is a recent phenomenon – and if government statements are anything to go by, appears to have come to an end.

That leaves Tonga as the only country where the “debt-trap diplomacy” narrative has some basis. Tonga is in a high level of debt distress, and Chinese lending dominates – the result of two large concessional loans provided by China Eximbank in 2008 and 2010.

However, anyone with knowledge of how those loans came about would argue that the Chinese state-centric “debt-trap diplomacy” narrative is a far stretch (see a 2014 article by Matt Dornan and Philippa Brant for a detailed description). The first loan came about in exceptional circumstances: the 2006 Nuku’alofa riots had destroyed a good portion of the CBD, and the government wanted to fund rapid reconstruction. The second loan for road re-development was driven by political machinations: MPs from outside of Nuku’alofa sought to attract loan-financed spending in their electorates outside of the CBD. In the background, (for-profit) Chinese construction firms which would implement the projects sought to ensure that both loans went ahead. In other words, the Chinese state did not drive either loan. In fact, given current tensions resulting from their repayment (the Tongan PM has made various contradictory remarks on the subject), it would be fair to argue that the loans have come to pose a headache for Chinese engagement with Tonga.

What can we conclude? Our analysis of debt in the Pacific strongly suggests that the “debt-trap diplomacy” argument is without foundation. Debt is a problem in the region, and one that appears to be increasing in importance. But for most countries it is not debt to China that is of concern. Keep that in mind next time you hear that the Pacific is drowning in Chinese debt.

For more on China’s engagement with the Pacific, see Matthew Dornan and Sachini Muller’s blog on the China shift in Pacific trade.

Solomon’s $100bn loans scandal: It hasn’t taken long for things to take a rather dramatic turn: to revisit the issue and my earlier observations, it’s risky to make far-reaching conclusions on a limited set of data bound by time; ‘debt is not static; some Pacific Island governments quite unpredictable and defy norms, and the situation can change in a blink – and so it has come to pass, it seems, with the Solomons changing allegiance from Taiwan to China, and seeking 100bn loan from ever-willing lenders, or so it seems from the following report. As I had mentioned, ‘China in the Pacific is a complex, multi-faceted, evolving phenomena not easy to keep abreast of, or fully comprehend.’ It’ll be interesting to see how this far-fetched sounding scheme unfolds now that the cat is out of the bag.

https://www.reuters.com/article/us-china-solomonislands/solomon-islands-seeks-100-billion-loan-from-chinese-interests-documents-idUSKBN20F12I

It seems authors are making assumptions and far-reaching conclusions based on methodologies and data that are quite limited in scope. Authors say Pacific is ‘not drowning in Chinese debt’. They should have added ‘for now’. Also, are we only concerned about the ‘now’? Good analysis should predict future trends. Data ‘strongly suggests that the “debt-trap diplomacy” argument is without foundation’. So nothing to see? Nothing too worry about? No danger of current situation changing for the worse? So many unanswered questions.

Hi Sheldon – thanks for the comment. However, commentary from the Lowy Institute suggests that we have likely seen the peak in Chinese lending to the Pacific (except for PNG) –

https://www.smh.com.au/politics/federal/china-makes-inroads-on-pacific-aid-but-australia-remains-the-stalwart-study-finds-20180808-p4zw8b.html

As Matt commented below – we don’t make any analysis of project quality, or other geopolitical issues – though we do hope what we have done contributes to the broader discussion.

This is an excellent and long-overdue piece. Thanks Matt and Rohan for putting the debt figures together. Data quality is a perennial problem in the Pacific, but this article allows others to build on the figures provided. I would also like to see rates of return on public investment by source, and issue that requires disaggregated data. Any help on this would be greatly appreciated.

Thanks for the comment Satish. It would be excellent to have that data – though unfortunately I don’t know anyone who has it either – and I don’t think it is the kind of thing that gets reported on – as you probably know Lowy looked at bilateral aid to the Pacific – which has data at the project level. But calculating returns would be a whole other project entirely. But Jono Pryke, Alexandre Dayant or Philippa Brant from Lowy might have some more info.

Vanuatu Daily Post also posted a similar story – http://dailypost.vu/business/the-debt-trap-myth/article_54428acb-4e7e-5e51-8f3d-8b06586821a4.html

But they also pointed to the citizenship and passport sale scheme for Asia, I assume China. I just found out that Vanuatu citizenship and passport is more attractive as they offer visa free to the EU – http://nomadcapitalist.com/2015/07/15/how-to-get-second-residency-citizenship-in-vanuatu/?fbclid=IwAR2zOJkHHKyuie4VoR6jJ-yZovg8ni4h3hXegKbbS5Aoa_LfE-OuMT51l_Q

thanks Rieko

Does PNG debt include SOE borrowings and other off-balance-sheet debt?

Hi Mark – good question – no it doesn’t – though according to 2017 IMF Article IV – total government debt (which is what the figures are based on – data taken from the MTFS 2018-2022) – were projected to be 27 053 million Kina, unfunded super liabilities were 2 311 million Kina, and SOE borrowing was 390 million Kina – of which there is no data I’ve found on how much is owed to China – though if you added both liabilities in to the graph it is likely you would get a smaller % of debt out of the total owed to China as all the super liabilities are domestic – so wouldn’t change the story much.

Solid, well-researched, thoughtful piece by colleagues Matt and Fox, although not all the details are always in the data/numbers alone and media reports should not be pooh-poohed out of hand. Moreover, should the Pacific be studied in isolation, or in comparison with other countries/regions to to provide a more complete picture?

Hot the heels of the Dornan-Fox report a news item from the South Morning China Post about the Maldives’ Chinese experience:

The Maldives owed Chinese government US$3 billion, not US$1.5 billion as widely estimated. Nearly all the deals secret, at inflated prices, potentially corrupt.

Is corruption a variable in the Pacific and was it/should it be considered in drawing conclusions?

In the Maldives case, the liabilities are greater than initially believed and will soon outpace the islands’ ability to pay. Any future lessons here?

If all above board with Chinese loans, why did Malaysia cancel two projects worth US$22 billion? Why is Pakistan trying to delay or revisit some projects worth US$60 billion?

Are these developments relevant to the Pacific or not? What can we learn from them? Should they be part of any review on the subject to provide broader conclusions? For example, is it relevant to the Pacific that Sri Lanka, after failing to renegotiate loan payments, ceded a port to China under a 99-year lease?

The full news item is here. Is it media speculation or are we lulled in a false sense of security?

‘Debt-trap claims unfounded. Pacific NOT drowning in Chinese debt’. Question is consequence of continued borrowing at current/accelerated rate. Any long-term financial risks or not? Should we look at Pacific in isolation? Do Sri Lanka, Africa hold any lessons for us or not?

Hi Shailendra,

Thanks as always for your comments. In this blog, we’re solely focused on aggregate debt and the portion owed to China. We don’t consider other questions, admittedly also important, such as: the quality of projects for which loans are made (an issue in the Malaysian case, and also in some projects in the Pacific), and the related issue of corruption and impacts on governance. I agree a comparative study would be interesting. Also interesting would be a debt analysis in which PIC debt is contextualised as part of the global trend, which has also (as a result of low interest rates) seen other developing countries increasing their debt. Thanks again. matt

Thank you for the clarification Matt. So much research, so little time! As we know, debt is not static. The situation can change- for better or worse – in a blink, so hard to pass definite judgements/firm conclusions.

China in the Pacific is a complex, multi-faceted, evolving phenomena not easy to keep abreast of, or fully comprehend.

Your research is helping understand the puzzle better. I look forward to more.