A recent chart from a G20 independent expert panel report on multilateral reform, reproduced by the well-known commentator Adam Tooze, caught our eye. Of all the countries that qualify for concessional support from the World Bank (basically the 70 or so poorest), PNG was shown to have had the second largest economic contraction over the pandemic. The figure showed that PNG had suffered a massive 27% reduction measured in terms of GDP per person (at constant prices and in international dollars) between 2019 and 2023. This was second only to Sudan, which suffered a 30% contraction.

Moreover, Timor-Leste was in third place with a contraction of 19% between 2019 and 2023, worse than Yemen at 16%.

We knew that things had been tough in both PNG and Timor-Leste, but surely not that bad? And, actually, no, the distinguished expert panel had got things wrong. Don’t blame the panel though; blame the IMF, its data source.

Let’s take PNG first. The IMF shows PNG’s population increasing from 8.8 million in 2020 to 11.8 million in 2021. That’s a 35% increase in a single year, and clearly that sort of increase in population is going to make your per-person growth crash.

It is true that PNG has recently increased its own estimate of its population size, but obviously no-one is saying that the extra three million people were added in a single year. The IMF says it addresses structural breaks by splicing, but not yet in this case.

What about Timor-Leste? Again investigations suggest problems with the IMF’s figures. First, it is worth noting that the IMF’s own estimate of per-person growth in Timor-Leste between 2019 and 2023 has changed from the -18.7% in its October 2023 World Economic Outlook (WEO) to -10.2% in its April 2024 WEO.

But neither the October nor the April numbers add up. Calculated and reported GDP per person bear no relationship to each other over the pandemic period, with the latter being always larger than the former, by varying amounts. You can’t find this out from the source itself, but the WEO’s current GDP series is consistent with what Timor-Leste reports as “non-oil” GDP, whereas the current GDP-per-person series, if multiplied by population, is consistent with what the country reports as GDP including petroleum production. (That something is wrong with the IMF’s Timor-Leste numbers is shown by the fact that its GDP current-price national currency and USD figures diverge between 2019 and 2023, even though the country’s currency is the USD. In fact the former is non-oil GDP, and the latter, which is used for the per-person calculations, GDP including oil.)

Since oil production has been in decline (and in fact has now actually halted), it is not surprising that a GDP-derived measure including oil shows a sharp contraction. But Timor-Leste’s GDP-including-oil series is extremely unreliable. Petroleum production wasn’t even counted in Timor-Leste’s GDP before 2019, and was only fully counted in 2020. Moreover, petroleum production is offshore, and only impacts the economy through the government revenue it generates. In its own reports, the IMF sensibly focuses exclusively on non-oil GDP, recognising the impact of oil revenue only when it is expended from the country’s sovereign wealth fund. Non-oil GDP per person contracts between 2019 and 2023, but by less than GDP-including-oil (6.4% vs 10.2%).

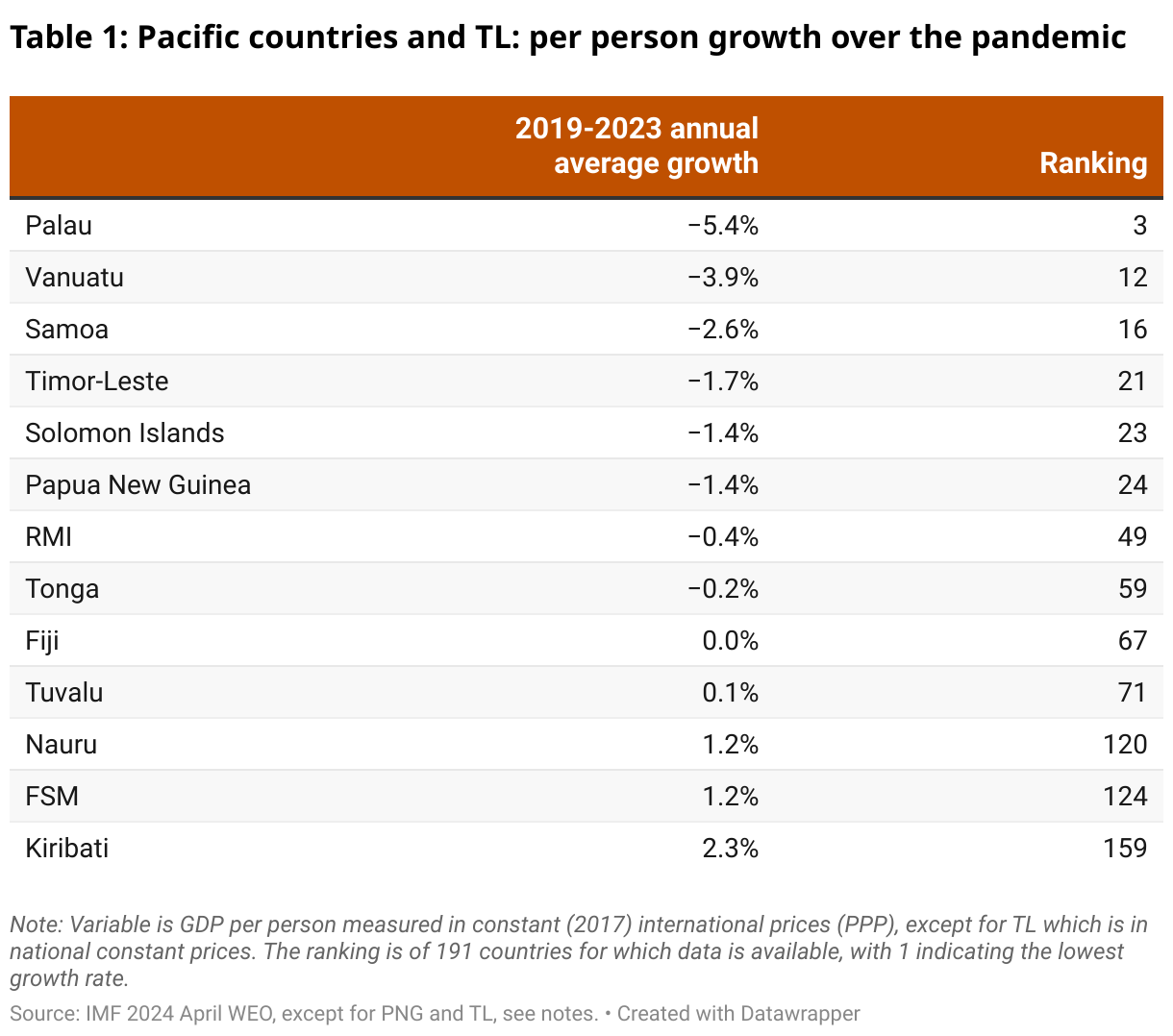

All this is not to deny that Timor-Leste and PNG, and indeed other Pacific economies, have been hit hard by the pandemic. Here is a list of all the countries from the region for which we could get data, along with their annual average growth between 2019 and 2023, from the April 2024 WEO, and their ranking among all the world’s economies, with 1 being the slowest growing country in the world, and 192 the fastest. We take all our data from the WEO, except for PNG, where we replace a 35% population growth rate in 2021 by a 3% one, and for Timor-Leste, where we use non-oil GDP per person figures.

Palau is actually the hardest-hit Pacific economy, and the fourth hardest hit in the world. Vanuatu comes next and then Samoa. These are all tourism-dependent economies. Timor-Leste comes 21st and PNG 24th — not great, but not disastrous. Solomon Islands is bracketed with these two. The Republic of the Marshall Islands (RMI), Tonga, Fiji and Tuvalu did better than one-third of the world’s economies over the pandemic, but worse than the other two-thirds. Nauru, the Federated States of Micronesia (FSM) and Kiribati all do better than the typical economy.

Not all these rankings are easy to explain. Fiji has clearly bounced back well from its tourism shut-down. Aid- and fisheries-revenue-dependent economies like Kiribati and FSM were relatively unaffected by COVID, but why FSM did much better than RMI requires more digging.

That said, this table would have made much less sense if Timor-Leste or PNG, neither a tourism destination, were at the top of it. Of course, the IMF has a big job managing data for some 200 countries. But a few basic checks would have identified the errors pointed out in this blog.

A colleague pointed out that FSM is listed as Micronesia in the WEO database (why did I miss that?). Anyway, doing the same calculations on national currency GDP – increase of 16.8%, converted into real terms to allow for CPI average inflation – 14.6% – and then population loss of 3.1%, FSM/Micronesia ends up at -1.3%. This is considerably lower than the +1.2% in the article – so FSM joins Solomon Islands and Tonga doing considerable worse with a different methodology. As Nik suggests, at best, there is indeed a need for important caveats when making comparisons. There are huge challenges as highlighted by the article – PNG has had a major revision in its population estimates. Hopefully, the current census will shed some light on the actual population. Worth remembering that in 2018, PNG’s National Statistics Office did a recalculation of PNG’s GDP. For 2006, this led a to a 50% increase in measured GDP in 2006. As an economic historian, just makes analysis of economic performance through time difficult.

Hi Paul. Thanks for the comment and analysis. It is helpful to get these results for comparison and I am interested in looking further into this. Your approach probably fits the Pacific better, but we opted for purchasing power parity for global comparisons. But as you and Nik point out, the key message from this blog is to emphasize the importance of holding data accountable to facts. Admittedly, international comparisons of economic performance through time are difficult. Therefore, it is important that people can keep in mind the difficulties and limitations to interpret data in a more sensible way.

International comparisons of economic performance through time are difficult. This article appropriately focuses on Timor-Leste’s non-oil economy performance. The same logic can also be applied to PNG’s non-resource economy, as once again, the resource sector is primarily foreign-owned with the primary impacts coming through resource revenues, which are captured in non-resource GDP anyway. The Purchasing Power Parity calculations are also vexed, especially for economies with large resource sectors. My preference when trying to measure changes in living standards is to look at real disposable household incomes – my interpretation of the outcomes of the 2009 Stiglitz-Sen-Fitoussi “Report by the Commission on the Measurement of Economic Performance and Social Progress.” For PNG, this is best done by taking nominal growth in non-resource GDP, discounting by the Consumer Price Index, and dividing by population growth. Over this four-year period, PNG’s non-resource economy grew by 39.8%, inflation grew by 18%, and population assumed to grow by 11.6% (using the 2020 IMF base and growing by 3% a year). The overall result was an improvement in living standards in PNG of 6.2% over this period – an average of 1.5%. When using the same methodology for other countries above (although I could not see FSM in the WEO database I downloaded), the average annual rates were as follows: Palau -6.4%, Solomon Islands -4.4%, Timor-Leste -3.8% (based on the article, and as local currency GDP was used, this is probably non-oil), Vanuatu -3.8%, Samoa -3.3%, Tonga -2.3%, Tuvalu -1.5%, Fiji -0.3%, Kiribati +1.4%, PNG +1.5%, Nauru +1.7% and RMI +1.7%. Some quite significant variations, with Solomon Islands and Tonga doing considerably worse, and PNG and RMI doing considerably better. I repeat the opening sentence.

Well done Sharon and Stephen.

This is lazy from the IMF and we have seen this repeatedly – even their own AIV reports for most countries in the Pacific are now flawed and that has deep implications for economic analysis and policy in the region.

Just one example of how this permeates – in your own blog, you continue to repeat the nonsense about tourism being a major economic factor for countries like Vanuatu and Samoa – absolute nonsense. The economic facts have never shown this.

The actual GDP rates for these countries are out now and again show an overly pessimistic analysis from the IMF during this period – despite many revisions throughout the period -which are then parroted by the WB and ADB and subsequently filter through to all of the reports of the development partners.

So, well done on calling it out – but will it have any impact on institutions like PFTAC – it remains to be seen but the Pacific needs better service in terms of economic analysis, now more than ever and the IMF’s need to be held to account for their poor economic coverage of the region.

Hi Nik, good to hear from you! I like your comment and would love to learn more about the “nonsense” including the role played by tourism in the economy of Vanuatu and Samoa. It’d be even better if you could write us some blogs 🙂 That would be very helpful to improve the quality of my economic analysis.