In Papua New Guinea, special support grants (SSGs) are allocated by the national government to provinces with resource projects to fund capital projects. Introduced in 1990, in the context of the Porgera negotiations, SSGs were intended to compensate provinces (initially Enga) for the fact that, following the Bougainville uprising and closure by landowners of the Panguna mine, it was deemed necessary to give a greater share of royalties to landowners rather than the provincial government (see p.66 of this report).

Benefits from the resource sector are substantial. In 2021 (the latest year for which resource revenue data is available), K5.8 billion (6.3% of GDP) was paid to PNG from the resource sector. Of this, K766 million in the form of levies, dividends from equity in resource projects, and royalties were paid to provincial governments, local level governments (LLGs), and landowners. For the provinces, not much is known about levies and dividends because these are not consistently reported. Royalties, however, have better reporting. In 2021, K311 million in royalties was paid, with K77.7 million going to resource provinces.

In 2022, five provinces received royalties: Eastern Highlands (K2.1 million), Madang (K2.8 million), Morobe (K2.3 million), New Ireland (K8.9 million), and Western (K25.8 million). Royalties make up a significant share of total revenue for Western and New Ireland (53% and 24% respectively), but a much lower share for the other three provinces.

Royalties are calculated at a rate of 2% of the gross revenue of resource sales, with royalty-sharing between provinces, LLGs and landowners varying by project. The royalty share received ranges from the 34% that the Ramu Nico mine pays Madang to the 91% that Kainantu gold mine pays Eastern Highlands. This means that provinces effectively receive between 0.7% and 1.8% of resource project sales as royalties.

Similar to royalties, SSGs were initially calculated at 1% of annual resource sales in 1990, before the SSG rate was reduced to 0.5% in 2002, and finally to 0.25% in 2005. SSGs form part of the national government’s capital expenditure under its Public Investment Program (PIP). In 1990, SSGs were allocated to four provinces: Western (Ok Tedi mine), Enga (Porgera mine), Milne Bay (Misima mine) and Bougainville (Panguna mine). Unfortunately, historical data on SSGs isn’t available.

In 2022, K26 million in SSGs was disbursed to the provinces, comprising 1.8% of provincial capital spending. SSGs in 2022 were allocated to five provinces: Western (K4 million), Gulf (K1 million), Southern Highlands (K10 million), Enga (K4 million), and New Ireland (K7 million). Gulf receives SSGs even though it doesn’t have a resource project because under the Kutubu oil project agreement, 30% of Southern Highland’s SSGs are to be paid to Gulf. Enga continued to receive SSGs even after the Porgera mine closed in 2020, and it is unclear why.

The first problem with SSGs is that they are confined to capital spending, whereas royalties primarily fund service delivery. This means SSGs cannot address gaps in service delivery. SSGs would be more efficient if they were converted to something similar to the function grants provinces receive from the national government to fund service delivery.

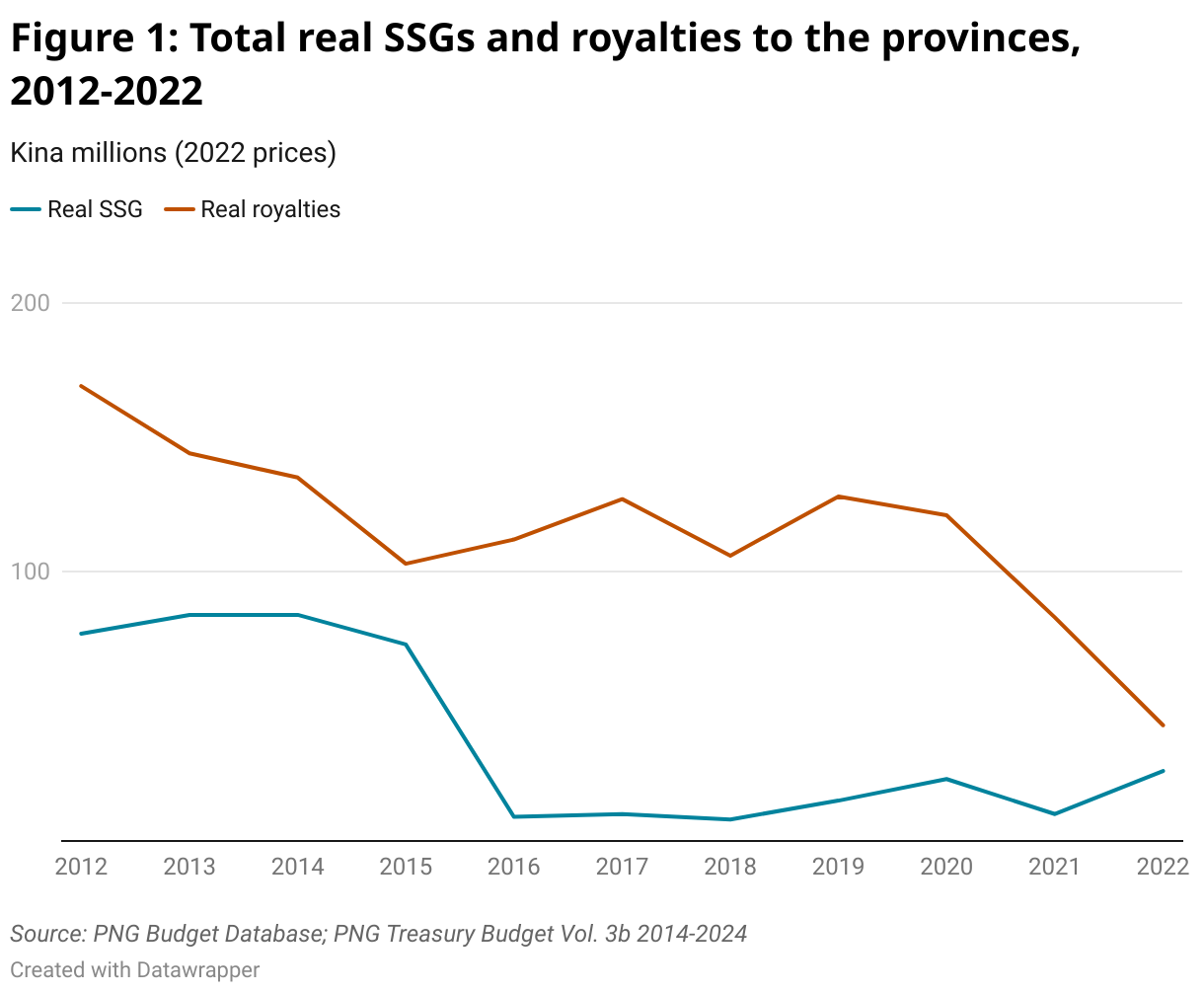

Second, over time, SSG disbursement has become discretionary. Real (adjusting for inflation) SSGs and royalties have trended differently since 2012 (the earliest year for which data is available), contrary to what one would expect given both are calculated from resource sales (See Figure 1). This is because while royalties are paid monthly from project resource sales, SSG levels are budgeted by national government in the year prior. As SSGs are part of the national government’s PIP, they are reduced in years when national government revenues fail to meet budget targets. This explains the fall in SSGs in 2016, following the 2015 collapse in national government revenue when a drought hit and oil prices fell. Adjusting for inflation, SSGs haven’t recovered to their 2015 levels since.

In fact, adjusting for inflation, both royalties to the provinces and SSG payment were much lower in 2022 than they were in 2012. The steady decline between 2012 and 2015, and the stagnation in real royalty levels between 2016 and 2020 reflects trends in resource sales. Real royalties to the provinces collapsed following the closure of the Porgera gold mine in Enga in 2020 and the 2021 change in New Ireland’s royalty sharing to include districts. The lack of a clear relationship between royalties and SSGs shows how discretionary the latter have become.

The third problem with SSGs is that they are inequitable because they are allocated to already wealthy provinces with resource projects. The two provinces – New Ireland and Western – who received royalties (and SSGs) in 2022 were certainly among PNG’s better-off provinces, generating K37 million and K49 million in revenue respectively, way above the provincial median revenue of K25 million.

A fourth and final problem with SSGs is that their governance arrangements are poor. According to Treasury, the status of all projects funded by SSGs is unknown. This is because provinces fail to report on and monitor SSG projects, making SSG funding unaccountable.

In summary, SSGs are inefficient, discretionary, inequitable, and unaccountable. They should be abolished.