In the past two months, a raft of reports relating to Vanuatu’s economy have been released: the national government’s Half Year Economic and Fiscal Update, the International Monetary Fund’s Article IV report, the Asian Development Bank’s Pacific Economic Monitor plus government tourism and trade statistics.

When these are read together it is hard to avoid the conclusion that there is an emerging economic emergency in Vanuatu.

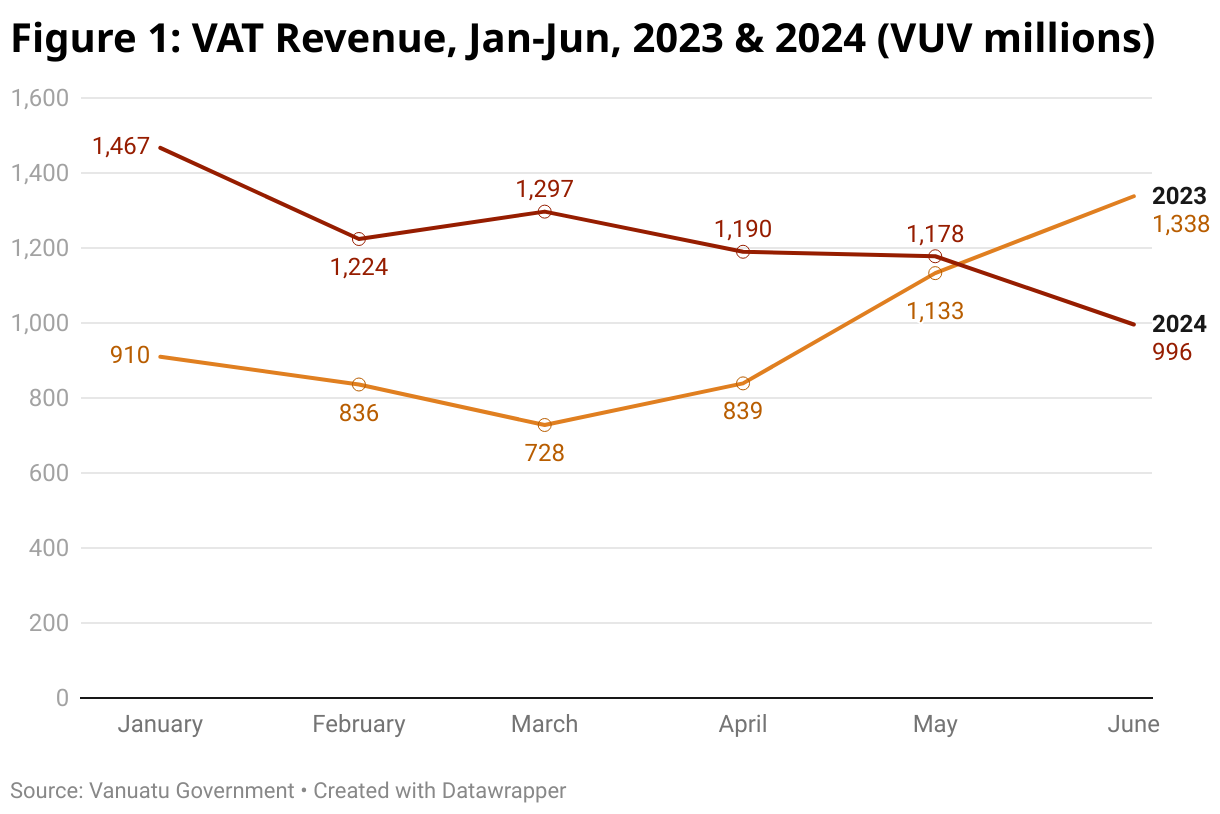

The simplest metric to measure economic activity is the quantity of Value Added Tax (VAT). This started the year off in record fashion, but the liquidation of Air Vanuatu had a clear and crushing impact. VAT returns in June (VUV996 million) were 25% lower than the year before (VUV1,388 million).

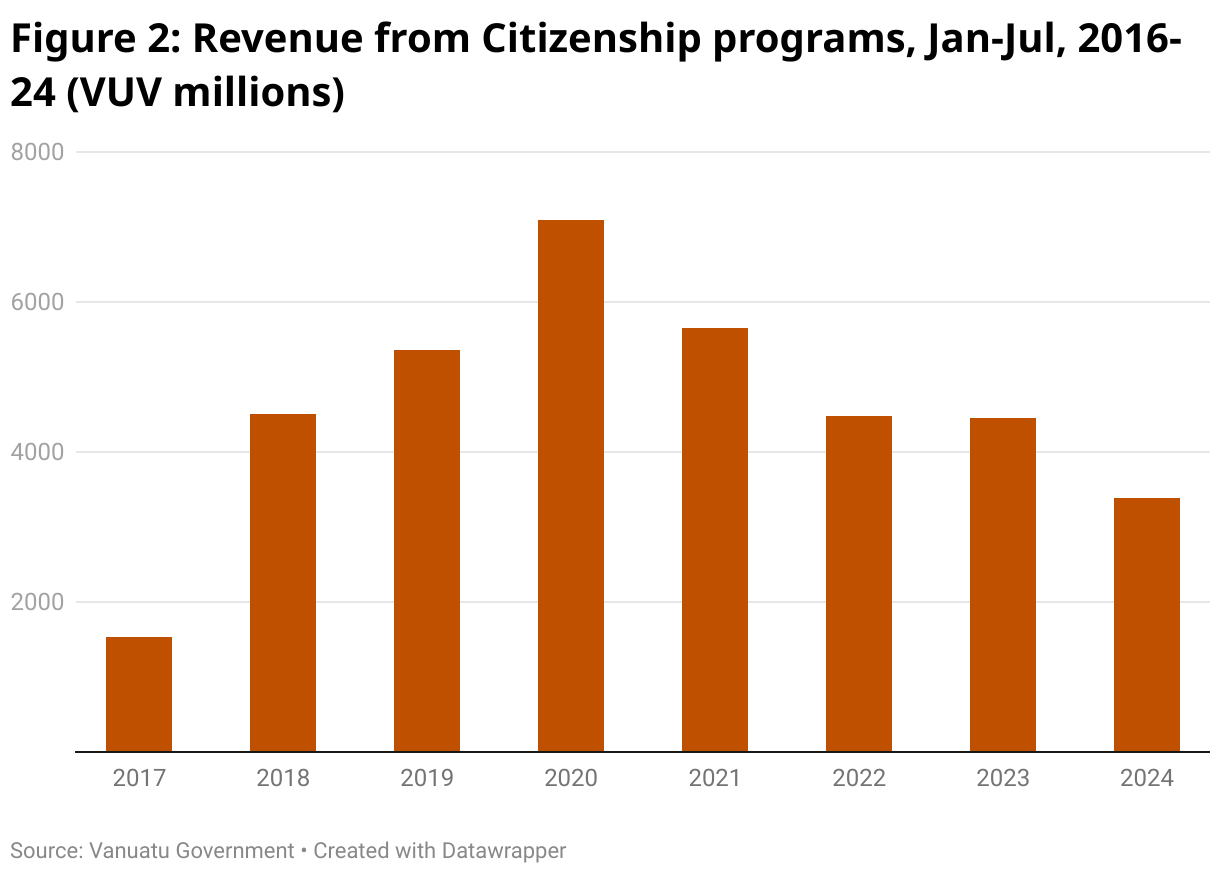

This is part of a broader crisis in government revenue, which was 23% below target from January until June, with no single revenue source meeting its target. Citizenship program revenue is the biggest concern, with revenue down 24% on 2023 and 50% on the 2020 peak. (The Citizenship By Investment Program, formally known as the Vanuatu Development Support Program, is a program which allows foreign citizens to purchase passports and gain visa-free travel to more than 80 countries.)

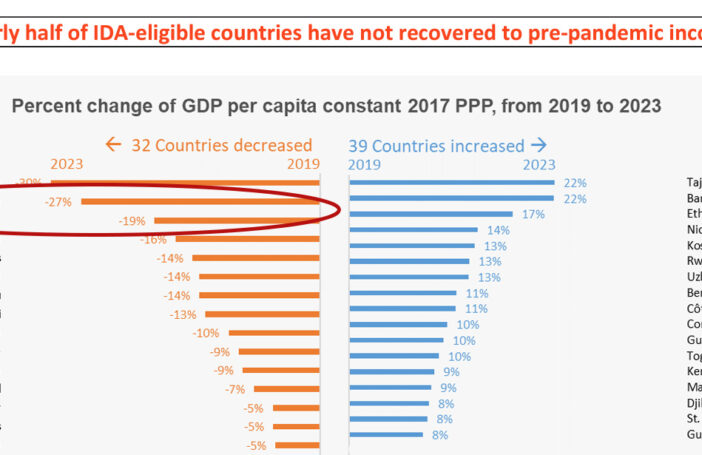

The World Bank estimates that the economy is 3% smaller than in 2019, and that real GDP per capita (approximately income per person) is US$2,517 (VUV 205,602). This is 11% lower than in 2019, and 8% lower than in 2000. There is no country at this income level which provides core government services to an acceptable quality.

The national government is forecasting annual growth of 3.8% from 2025 to 2028, and the IMF forecasts just 2% annual growth until 2044. With the population growing at roughly 2% yearly, this would mean limited improvements in the quality of life.

This would be concerning normally, but with the climate emergency looming, it is critical. The economic costs of the crisis will be huge, and the single best way to adapt to it is to get richer. Constant technological and geopolitical upheavals make it all the more important for Vanuatu to become more resilient.

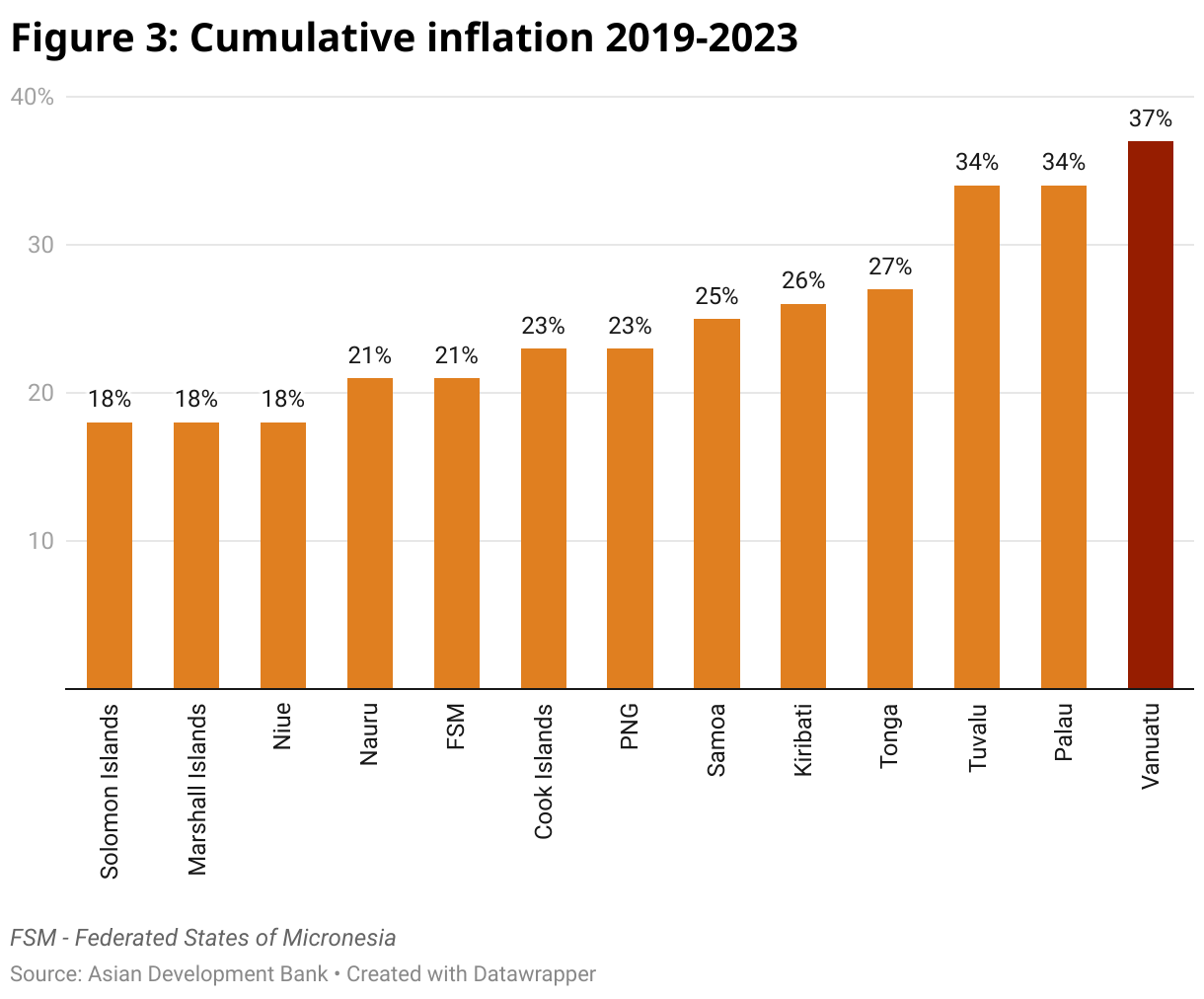

In the face of these challenges, Vanuatu should be aiming for a growth rate of at least 7% until at least 2050. To achieve this, there must be a drastic expansion in productive capacity – the amount of goods and services an economy can produce. Limited productive capacity is one of the reasons Vanuatu has had the highest inflation in the Pacific since 2019.

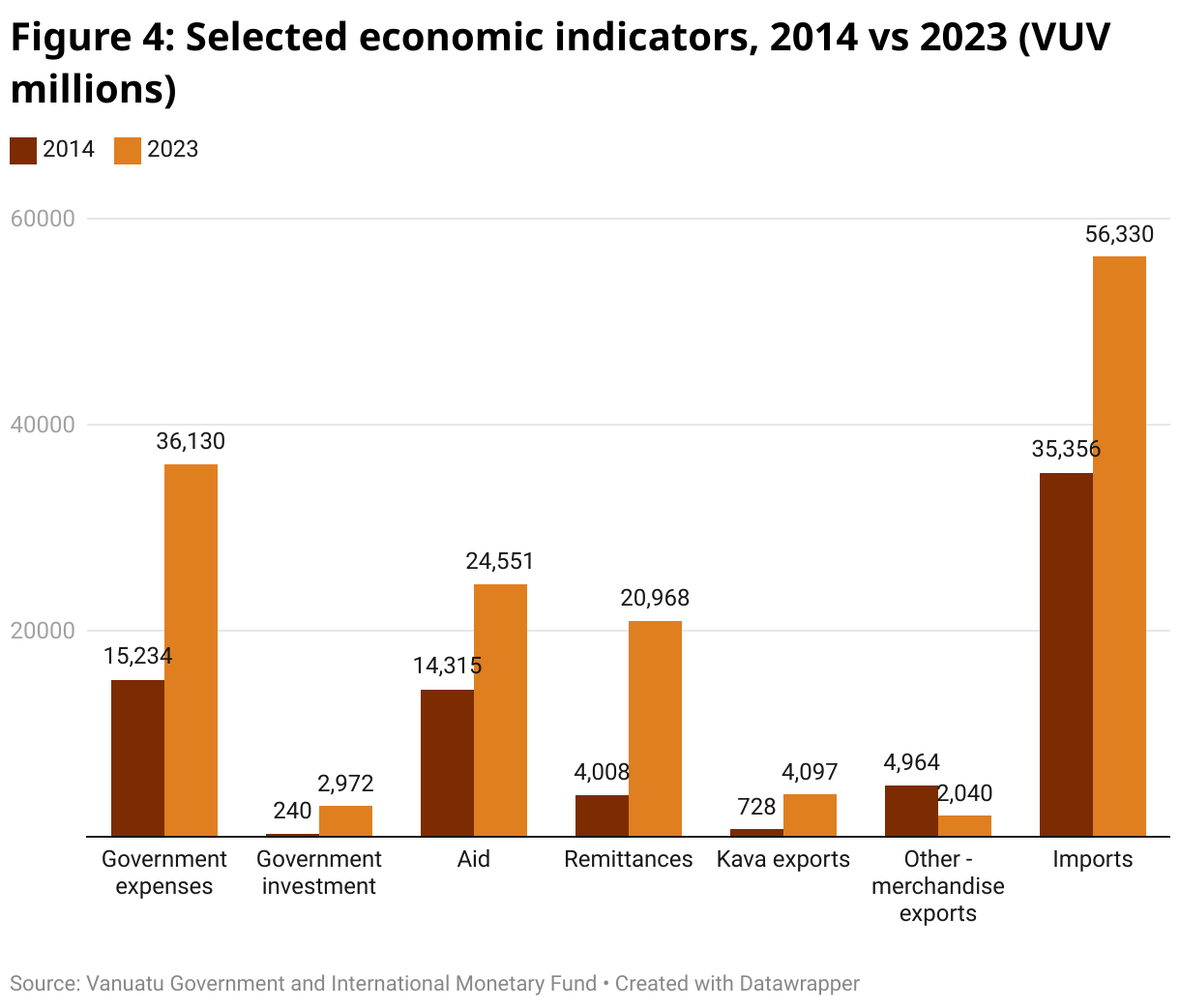

Far too much of the growth of the past decade has failed to boost productive capacity. This is particularly true of growth driven by citizenship sales, aid and remittances. Of course, these all have major positives, but they also all involve large amounts of money flowing into the economy that has not been earned within Vanuatu, much of which flows straight out again through imports.

To boost productive capacity, Vanuatu needs huge amounts of good investment — this is what builds genuine wealth and resilience over the long-term.

The government is currently spending but not investing. Expenses (day-to-day spending) hit a record high in the first half of 2024 (VUV19.7 billion), but investment remains low and slow. Just 4.6% (VUV790 million) of the capital budget for the year had been spent by June.

Forecasts for government expenses are steady, while government investment forecasts for 2025-2028 have been downgraded from VUV22 billion to VUV15 billion.

The IMF is calling for fiscal consolidation (cutting spending) in response to the revenue issues. Somehow, they have not learnt from their own long and disastrous history what awful policy this is. Following this advice has already caused major issues in the past six months in Kenya, Ghana, Sri Lanka and Bangladesh, and no-one can seriously argue that the government is spending enough to deliver the most basic services.

Over the long run, the only way that higher spending can be sustainable is if the economy is far larger. Most of this growth will have to come from the private sector. Businesses have endured a brutal decade of natural disasters, COVID, political instability and consistent air connectivity issues. As a result, private sector confidence and trust is low.

Foreign direct investment was just 0.9% of GDP in 2023, well below the historical average. There is limited data on domestic investment, but there is definitely not enough.

Merchandise exports were just 8% higher in 2023 than in 2014, far below both inflation and population growth. Food inflation has been 60% over this period, with many increasingly struggling to afford healthy food. Visitor arrivals by air were 29% lower in 2023 than in 2014 and they have fallen a further 28% this year.

The business environment remains extremely challenging, with access to skills the biggest issue. A country’s most important resource is its people but heartbreakingly the current generation of children is categorically not being given the tools needed. Three out of ten children are stunted, while eight out of ten failed to meet the minimum standard for Year 4 Literacy in the most recent Pacific-wide assessment.

But in the face of all of these challenges, there remains cause for immense optimism. The full case for this is at least a whole article in itself, but three key points are briefly made below.

First, Vanuatu is a wonderful, peaceful and friendly country, and many of its foundations are extremely strong; often more so than in richer countries.

Second, emerging technologies mean that the economic story could be completely transformed in a very short timeframe.

Third, there has been undoubtedly been rapid progress in many areas, and we must not forgot that progress.

It’s also the case that a number of good initiatives have been announced recently, such as the increasing digitalization of government and the townships project. But, of course, there is much more that must be done.

One idea is to set up an Economic and Investment Committee, chaired by the Prime Minister, with a single goal of achieving 7% economic growth. The Economic and Investment Forum in March this year generated 80 ideas for improving the business environment. Such a committee could go through these ideas and rapidly implement the best.

However, the full impact of many reforms would not be felt for years, and would not solve the immediate revenue issues.

I would therefore suggest that VAT is increased to 20%. The emerging economic emergency means that drastic action is needed, and VAT is the only lever that can provide the required revenue in the timeframe required.

Of course, this would be highly controversial and painful, particularly for those struggling the most. For the policy to work, two things must happen.

First, there must be an accompanying major improvement in how the government spends money. Inefficient and wasteful spending must be replaced by quality investment for the long-term future of Vanuatu. The devastating Off-Budget Entities Report is a clear indicator of the need for urgent reform.

Second, part of the revenue raised should be used to reform the business environment. To this end, I would also suggest that nearly every single fee and charge is completely abolished, and that a 10% VAT rate is applied to key sectors (such as shipping, Vanuatu-made goods and construction). This can be done almost immediately, and it would both make a major difference to the ease of doing business and send a strong signal that the government is serious about reform and growth.

Tankio tumas Peter. A great and timely piece. Wondering if you had run any numbers or done some analysis on the impact of the PALM and RSE? I understand there is an increase, but coupled with additional pathways being introduced that can lead to eventual out migration, not just with our current neighbours, but also with the establishment of new foriegn government embassies, it would be interesting to do some analysis on the impacts on the national economy, not to mention all the other socio economic issues.

Peter, thank you for your insightful and well-structured article addressing Vanuatu’s emerging economic challenges. You effectively highlighted critical areas of concern, particularly the decline in VAT revenue, the collapse of the Citizenship by Investment Program, and the pressing need to expand productive capacity. Your emphasis on the need for drastic action and structural reforms, such as expanding the country’s long-term growth capacity, resonates strongly given the current state of Vanuatu’s economy. The call for better public sector investment and more targeted spending is indeed timely, as these areas have long been underperforming.

Beyond the measures you have proposed, digitization and technology offer a range of benefits that can address some of Vanuatu’s critical challenges and offer transformative opportunities which Vanuatu can pioneer. I understand technology is not the only measure, but I would like to elaborate on this since it is an important one given the insufficient investment in this area. Implementing e-government solutions would streamline bureaucratic processes, reduce inefficiencies, and foster a more business-friendly environment—particularly valuable given the chronic vacancies in our public sector. As a small island nation with a limited talent pool, the more we can automate the better. Just as technology can streamline governance, it also holds vast potential to revolutionize key industries like tourism and agriculture. Leveraging digital platforms and AI-driven marketing can attract global audiences and improve customer service, while digital solutions in agriculture can increase productivity and expand access to new markets. In addition to boosting productivity in tourism and agriculture, technology can also enhance financial inclusion. Affordable mobile banking and digital payment systems could enhance financial inclusion, empowering microenterprises, especially in rural areas, to grow and thrive.

And on the topic of microenterprises, we seem to have faltered. Microenterprises in Vanuatu can play a crucial role in the local economy, particularly in rural areas where formal employment opportunities are limited. With many of the area councils now starting to build critical infrastructure, including connectivity, technology can enable microenterprises improve access to finance, market access, build skills and capacity (think Youtube), participate in developing new and innovative business models, etc.

Finally, beyond economic productivity, tech-driven innovations can also play a critical role in addressing climate challenges and could also strengthen Vanuatu’s climate resilience. Digital tools for environmental monitoring, renewable energy management, and disaster preparedness would not only protect the country from the looming climate crisis but also open access to global climate financing. Additionally, promoting innovation hubs and tech clusters can position Vanuatu as a leader in sustainable development, driving growth through homegrown solutions and international collaboration. Together with structural reforms, technology along with quality education and a healthy population could be the key to unlocking long-term resilience and prosperity for our country.

Lauro Vives

Managing Partner

Pacific Development Consulting Ltd.

Port Vila, Vanuatu

Thanks Lauro. Completely agree with what you say, and in some ways your response is the longer version of the below paragraph from my article, which I didn’t have the space to expand on.

“Second, emerging technologies mean that the economic story could be completely transformed in a very short timeframe.”

Solar + batteries mean that we can have cheap energy for the first time ever, internet connectivity opens up opportunities for eGovernment and business that simply weren’t possible before, financial inclusion can be transformed, etc. etc.

Hopefully catch up soon to talk over this in more detail!

All great comments in isolataion BUT the fact is that the country, without realising it is moving to a state of over regulation in commercial matters. VIPA is where the “P” stands for prevention to start up new businesses. Instead of promotion. VFSC now requires unnecessary documents to create a a new company, etc. Opening a bank account requires FIU and multiple pages of documentaation Most countries that are progressive have few restrictions on new businesses. Vanuatu has gone the other way.

Hi Peter, thanks for the great article. We (Vanuatu) need to move faster if we truly believe we can cut out the mindless and repetitive paperwork and the associated costs that grind this country to a halt in virtually every department. The time for studies and surveys is over and it is time for change or get left behind. We should embrace the Nomad workspace culture, not only does this bring foreign investment and spending into the country, it also highlights the great opportunities here in Vanuatu for tourism and lifestyle. To entice people to visit here and create opportunities for working abroad we should consider some of the work visas and minimal or zero tax obligations that many European countries have implemented to encourage foreign income and spending which in many cases would outweigh taxable income. There have been some previous articles on the various categories of VIPA and how they discourage this type of travelling entrepreneur or business person and the current system and mindset is likely to drive many who have chosen to live and work here to look for greener pastures. I know a few…

Thanks Peter

This discussion directly addresses the challenges and opportunities facing Vanuatu’s economy. A significant obstacle remains the ongoing land dispute, which has hindered investments. However, I believe the foundation lies in understanding our economic institutions as well. Question to think around it in terms of: Do people trust the current economic system and government ( to pay tax)? If copra and kava are our primary economic pillars, how can we boost production to enhance market confidence, for people to trust the market and continue producing? Ultimately, it depends on people’s reactions and behaviors. Do they trust healthcare to have more children ( raise the population growth rate? Do they trust education to invest in their children’s futures to be educated? These questions highlight the interconnectedness of economic institutions especially further looking at the culture, trust, and norms in Vanuatu.

Thanks Wenny. Agree with what you say about institutions, particularly healthcare and education. The ideas I raised were all simply short-term ones, but in the long-term, fixing education outweighs absolutely everything else.

The only thing I’d pick up on is copra. It is a lot of work for not much money, and exports are way down (just 195m to June, compared to VUV 1,811m in 2017 at its peak. The CRB and low prices have been devastating for this. I don’t think copra can therefore be really seen as a primary economic pillar any more.

This is a great piece by Peter Judge. Peter raises critical points regarding the economic challenges faced by Vanuatu, including the significant decline in government revenue and the impact of the liquidation of Air Vanuatu on VAT returns. His suggestions for achieving rapid economic growth through productive capacity expansion are commendable. However, as we look forward, might I add, it is important to consider Vanuatu’s unique strengths and its international commitments to biodiversity.

A. Integrating Vanuatu’s Safety Nets: Customary Land as Economic Resilience

While boosting productive capacity and foreign investments are important, the resilience of Vanuatu’s economy cannot be separated from the customary land tenure system. Indeed it may be agued that over-reliance on foreign investments exposes the economy. Over 80% of Vanuatu’s land is held under customary ownership, which provides a significant social safety net during economic crises. Access to customary land has historically protected communities during times of economic hardship, allowing them to rely on traditional agriculture and resources. This is a unique form of wealth that is not captured in traditional GDP metrics but plays a critical role in social stability and food security. Judge’s focus on productive capacity expansion should therefore be complemented by efforts to strengthen and protect customary land rights, ensuring that this vital safety net remains intact. Doing so not only preserves social cohesion but also provides an economic buffer against future crises.

B. Aligning Economic Strategy with Biodiversity Targets

Vanuatu is a global leader in environmental conservation, and any economic recovery plan must align with its role in achieving the Kunming-Montreal Global Biodiversity Framework’s 30×30 targets. These targets commit countries to protect 30% of land and marine areas by 2030, which is critical for safeguarding biodiversity and combating climate change. Intervention on Indigenous Peoples’ role in biodiversity, lands managed by indigenous communities often demonstrate better conservation outcomes than state-protected areas.

Vanuatu’s commitment to biodiversity conservation is not just an environmental issue—it’s an economic one. Healthy ecosystems provide services that underpin sectors like tourism, agriculture, and fisheries, which are cornerstones of Vanuatu’s economy. Therefore, economic responses should prioritize nature-based solutions and sustainable development that contribute to these biodiversity targets. By leveraging international financing (Green Climate Fund and Biodiversity Funds etc) Vanuatu can secure investment to both protect biodiversity and foster sustainable economic growth.

C. Developing Resilient Economies Based on New Definitions of Well-being

As the world faces increasingly complex global challenges—climate change, biodiversity loss, and economic inequality—traditional models of economic growth are becoming outdated. It might even be argued that those economic growth models are irresponsible on a planetary scale Vanuatu’s current economic difficulties should be viewed as an opportunity to pioneer a new model of well-being, one that is planetary in scale and based on the well-being of ecosystems as well as people. The Kunming-Montreal Targets emphasize the importance of preserving biodiversity and natural ecosystems. Vanuatu’s economic strategy should thus shift from a focus solely on GDP growth to a more holistic approach that values ecosystem services, social well-being, and climate resilience.

This new model would not only benefit Vanuatu but could serve as a blueprint for other nations. By integrating indigenous knowledge systems and customary land practices with modern economic policies, Vanuatu can demonstrate how small island developing states (SIDS) can build robust, resilient economies that thrive within the natural limits of the planet. This would position Vanuatu not just as a participant in global economic systems, but as a leader in redefining what true prosperity means in the 21st century.

Summary:

While Peter Judge’s recommendations for increasing productive capacity and foreign investment are valuable, they must be integrated with Vanuatu’s customary land-based safety nets and commitment to global biodiversity targets. Furthermore, the current economic challenges provide a platform for developing a new model of economic resilience that goes beyond traditional metrics like GDP, focusing instead on planetary well-being and sustainability. This holistic approach will ensure that Vanuatu emerges not only economically stronger but as a regional leader in sustainable development.

Happy biological diversity month:)

Thanks Dr Phillip. And I completely agree with what you say here. GDP is just one metric, and far too many of the world’s current problems have stemmed from an obsession with growth, often ignoring or forgetting what really matters (health, community, environment, etc.). As just one example, current extinction rates are estimated to be 100 to 1,000 times higher than natural background rates due to human activity.

At the same time, country’s need a minimum level of wealth/income to be able to provide the basic services to an acceptable standard, and Vanuatu is simply not rich enough. The literature suggests that a GDP/capita of about USD 10,000 is needed for this, and Vanuatu is only 25-30% of that. There is a good argument to be made that the customary economy (which must be preserved) means that this level would be lower in Vanuatu, but conversely the costs associated with geography and natural disasters may mean it is higher. But the main point here is that it is clear Vanuatu is not rich enough to provide these services, and so growth is needed for Vanuatu.

But it is not endless growth that is needed – indeed the only thing that keeps on growing is cancer! We must make sure that it is good growth – inclusive and fair to both people and nature.

Always happy to talk more over a coffee, and happy biological diversity month 🙂

We don’t need to raise VAT, Just cut unessary spending, implement a public sector reform to strengthen public institutions and improve quality of government spending.

Thanks Henry. I agree on the need to reduce unnecessary spending and implement public sector reform, but at the same time, I still believe more revenue is needed to a) fund core services (especially education) and investment and b) to improve the business environment to enable investment and growth.

Vanuatu is an extremely expensive country to operate in, and the Govt needs revenue. With no income tax, and with citizenship revenue falling, it has to come from somewhere.

Hi Peter, while I agree with the need to increase government revenue, I do not think we need to increase VAT. We cannot continue to put extra burden on consumers without controlling the leakages. Those leakages need to be fixed, and we need a holistic review on our current fees and charges. Four decades ago, the government budget was less than 10 billion, yet most of the basic services such as schools, hospitals, airports and etc are up and running. Four decades later, most of them are now in the verge of collapsing yet, the government budget has now increased them by nearly a 1000 percent. Why? The government has received twice, or more aid from developing partners, unfortunately, most of the citizens do not feel that their livelihood has improved. Maybe in papers and reports, but the reality seems otherwise. So, I do not think increasing VAT should be an option.

I agree Henry. It is too simplistic to point to an increased VAT without looking at the expenditures side, transfers and tax expenditures, and indeed other tax options such as digital services tax. What will be the social impacts of different tax and tax expenditure options.

Fiscal consolidation in Sri Lanka since the 2022 crisis has only marginally depended on spending cuts and mostly relied on revenue measures taking tax collections from 7.3 percent of GDP at the low point in 2022 to 9.6 percent of GDP in 2023 and heading to 12.4 percent of GDP in 2024. VAT rates at 20 percent and higher may become problematic. Perhaps Vanuatu should finally move to a more balanced tax system that includes income tax like most countries.

Thanks David. Income tax for Vanuatu is a minimum 5 year project to implement, and doesn’t solve the immediate revenue issues. The economy is also (in my opinion) too small and the business challenge too challenging for an income tax tax to make sense. Unleash the power of cheap energy (solar + battery), move as much of Government online as possible, resolve the skills issues, let the economy grow rapidly, and then I think it makes sense to introduce a well-signaled income tax.