Employer demand for short-term seasonal workers under Australia’s Pacific Australia Labour Mobility (PALM) scheme is in decline, according to recent analysis by Richard Curtain. This has been attributed to two factors. First, more stringent conditions are being placed on Approved Employers, including plans to require employers to guarantee payment for a minimum of 30 hours of work per week. This makes employing short-term PALM workers more expensive than in previous years when hours could be averaged over the duration of the contract. Second, working holiday makers (backpackers) in Australia offer employers a less costly, alternative source of seasonal labour – and their numbers are rising.

Australia’s plan to introduce a minimum 30 hour per week guarantee follows New Zealand’s practice. New Zealand imposed this requirement on Recognised Seasonal Employer (RSE) scheme employers in late 2021 during the COVID pandemic to ensure RSE workers who could not return home had sufficient earnings to cover their living costs.

Backpacker numbers have also been on the rise in New Zealand post-COVID, though the absolute numbers are much smaller than in Australia. At the end of February 2024, there were around 34,000 backpackers in New Zealand, compared to more than 181,000 in Australia.

Backpackers make up around 13% of New Zealand’s horticultural seasonal workforce, although some regions make more extensive use of them than others. Anecdotal reports from RSE employers suggest backpackers were readily available for seasonal work around the country during the 2023-24 peak harvest period, providing an additional source of labour alongside New Zealand locals and RSE workers.

With the same influencing factors at play in the New Zealand context – more backpackers seeking work, the requirement for RSE employers to guarantee pay for 30 hours per week regardless of work availability (e.g. on wet days), and other measures making the scheme more expensive (see below) – the question is whether employer demand under the RSE scheme is also dropping.

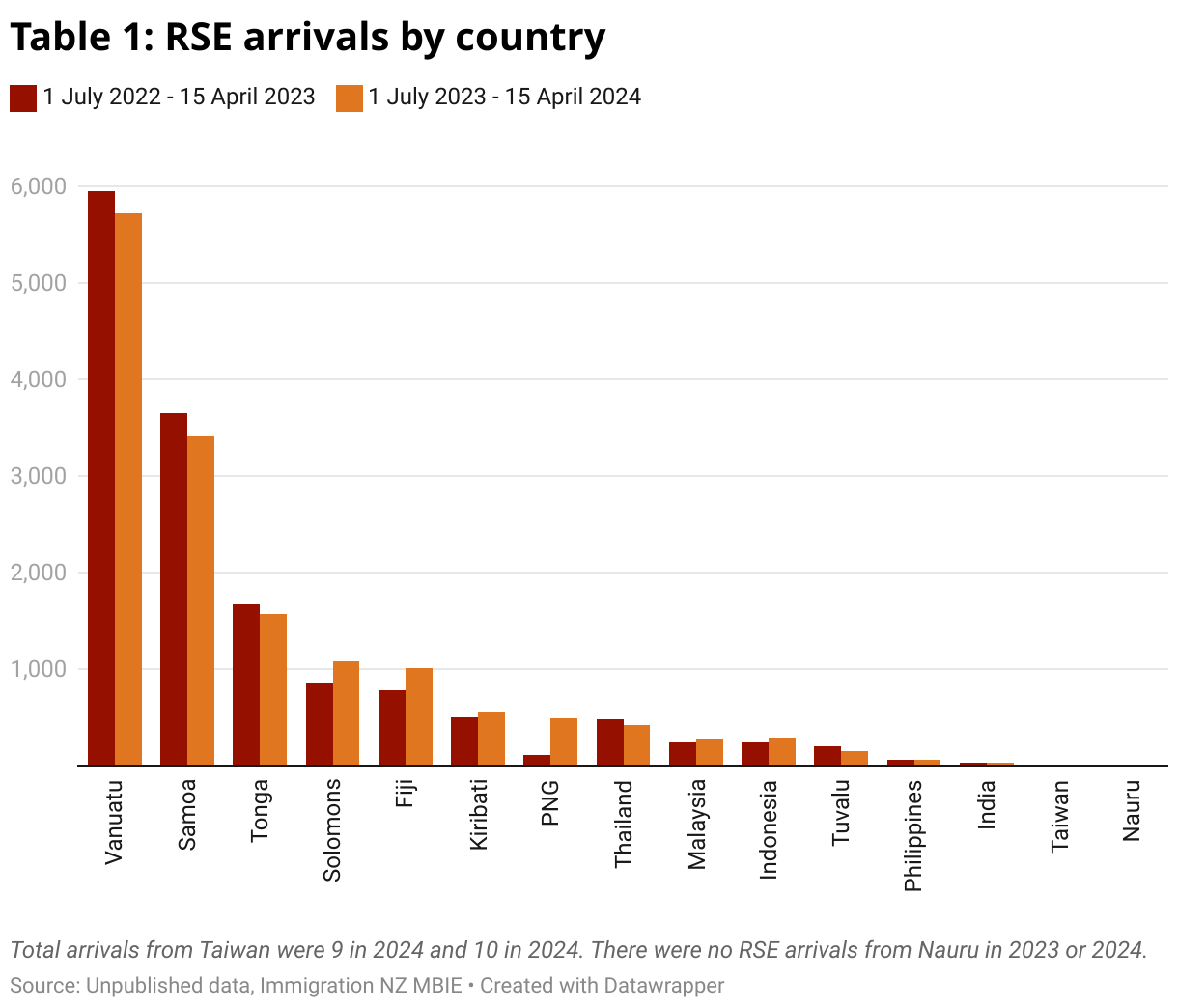

RSE arrivals data for the ten months to mid-April 2024 suggest something of a plateau in demand. A total of 15,102 RSE workers arrived in the country between 1 July 2023 and 15 April 2024, an increase of 2.2% over the same period in the previous year (14,782 workers).

An interesting feature of recruitment in 2023-24 compared to the previous year is the shift in employers’ recruitment patterns. RSE employers are moving away from Vanuatu, Samoa, and Tonga – historically the three main sources of RSE labour – and instead looking to other countries for their workers (Figure 1).

Vanuatu (-4%), Samoa (-7%) and Tonga (-6%) all experienced a drop in numbers between 2022-23 and 2023-24 – likely a response by RSE employers to concerns raised by Pacific governments in these countries about the damaging economic and societal effects of the regular exodus of men and women to New Zealand and Australia for temporary work.

Tuvalu also saw a significant decline, down 25% on the total recruited (197) in the previous year to 15 April 2023. Almost half of the RSE enterprises who recruit from Tuvalu are located in Gisborne-Tairāwhiti and Hawke’s Bay – two of the primary horticultural growing regions that bore the brunt of Cyclone Gabrielle in 2023. Recovery efforts are ongoing with orchards being re-worked and replanted, but trees take several years to reach full production. Consequently, for some RSE enterprises, short-term demand for RSE workers has reduced.

As RSE employers’ recruitment patterns have shifted, the big winner has been Papua New Guinea. Recruitment from PNG grew 326% between mid-April 2023 and 2024, with an additional 375 RSE workers recruited. Fiji (31%) and Solomon Islands (26%) also saw increases. For Fiji and Solomon Islands, 2024 was the first year in which they supplied over 1,000 workers under the RSE scheme. This is positive evidence of the continued efforts by RSE government officials to encourage employers to diversify away from traditional source countries and recruit from countries with much larger working age populations.

With the end of the 2023-24 financial year (30 June) approaching, total RSE arrivals are unlikely to reach the current annual cap of 19,500 places.

An estimate of total arrivals for 2023-24 can be approximated by looking at RSE arrivals in the preceding year, and by assuming that over both years the same proportions of workers arrived between 1 July and 15 April, and in the last 2.5 months of the financial year (15 April – 30 June). In 2022-23, these proportions were 85% and 15% respectively.

If the 15,102 workers who arrived between 1 July 2023 and 15 April 2024 account for 85% of the total for the financial year, then the remaining 15% will be around 2,700, giving an approximate total for the year of 17,800. This is a shortfall of 1,700 workers against the cap of 19,500.

Feedback from industry representatives suggests cost pressures are creating some strong headwinds for RSE employers. Recent changes to minimum pay requirements mean RSE employers must pay 10% above minimum wage for their RSE workers, even though this is not a requirement for their New Zealand workers. This comes on top of the obligation to guarantee pay for 30 hours per week, every week, even when work is not available due to bad weather or crop-related factors.

A freeze on increases to RSE worker accommodation rates has been in place since late 2022 which means RSE employers continue to charge rents at 2022 levels, despite rising inflation. Employers also face rising audit and compliance costs. For smaller enterprises, these cost pressures may well see some exit the RSE scheme.

Shortfalls of suitable accommodation to house RSE workers in some regions, and logistical constraints on recruitment in some Pacific countries are added burdens. The current predicament facing Air Vanuatu is a prime example of the disruption that employers and workers can face to recruitment and travel plans.

Looking ahead to the 2024-25 season, industry has requested an increase to the annual RSE cap, but (subject to government approval) the increase is likely to be relatively small. Continual expansion in the kiwifruit industry, and post-cyclone recovery in the pipfruit industry – which includes the consolidation of some RSE enterprises – is pushing up labour demand, but the increased regulation is pushing in the opposite direction.

Industry is asking for the accommodation freeze to be lifted, and for the guaranteed 30 hour per week requirement to be re-considered. Industry is not seeking a return to the original policy settings which allowed 30 hours per week to be averaged over the duration of the contract. Rather, they are seeking something of a compromise; guaranteed 30 hours per week averaged over a four-week period. This is the current setting for PALM Approved Employers, following concerns expressed by Australian employers, will now remain in place for at least the next 12 months, if not longer.

In the meantime, the re-establishment of the RSE National Labour Governance Group (NLGG) in early 2024, which sits above the 11 Regional Labour Governance Groups, is a positive development. The NLGG provides a critical forum for direct industry-government engagement on RSE strategy and operational matters. With a clear governance structure and lines of industry-government communication in place, now is an opportune time to reassess some of the RSE policy settings to ensure employers’ participation remains financially viable.

I am interested in working for a company which recruits RSE workers.I have been going to New Zealand for two years working under the program and would like to know if there’s some company that would recruit me to work for them in Australia. I have Two years experience in working in the horticulture sector and interested to try out new working environments.

I am interested in working for the program