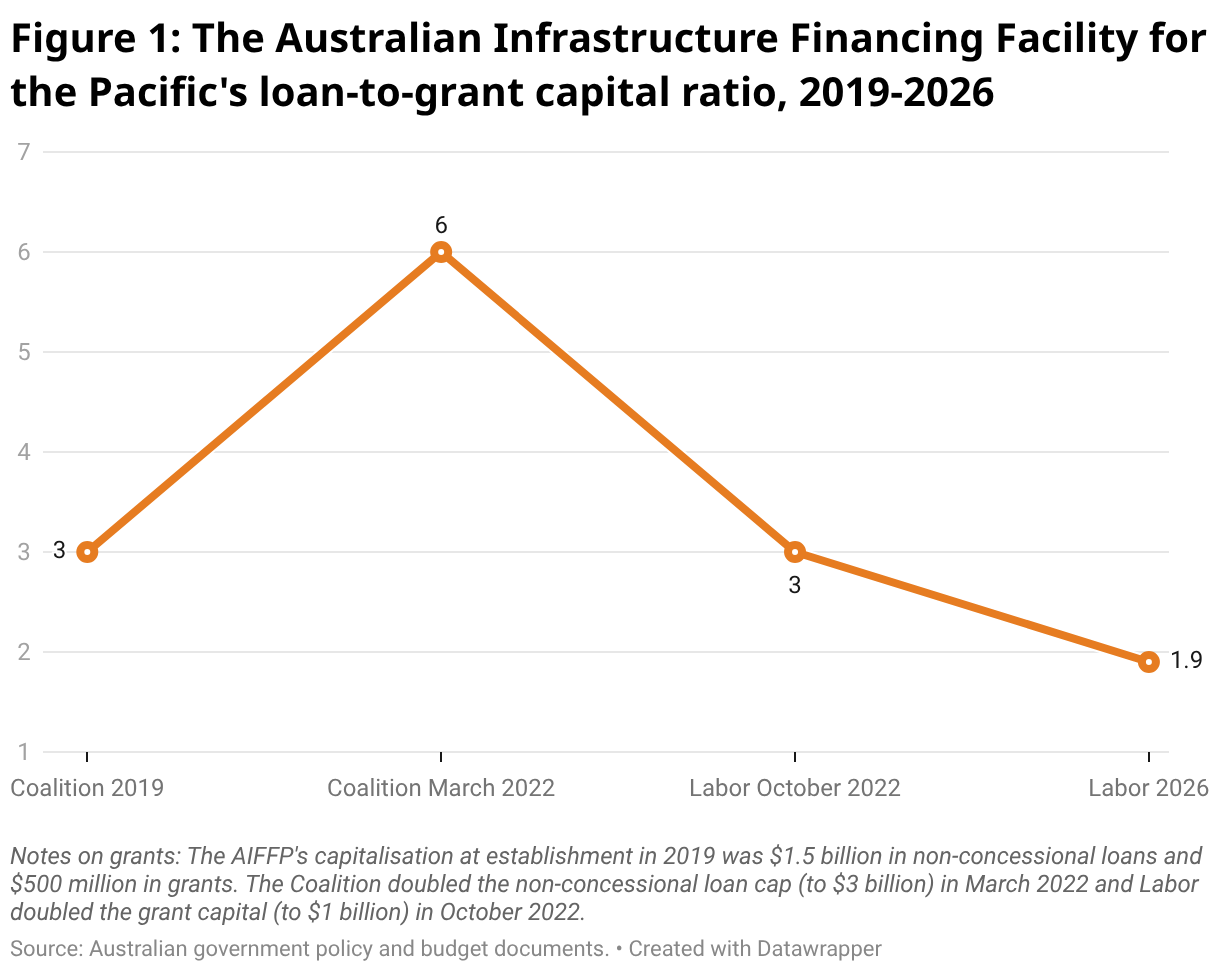

The decision to allocate another $550 million in Official Development Assistance (ODA) grants to the Australian Infrastructure Financing Facility for the Pacific (AIFFP) was announced by Australian government in January with little fanfare and has received only limited attention. This announcement was significant, however, because it confirms the change in the AIFFP’s character from primarily a non-concessional lending facility to one that has become increasingly reliant on more expensive (for Australia) — and scarcer — grant capital. Since its establishment in 2019, the AIFFP’s loan-to-grant ratio has declined by more than two thirds, from a peak of 6:1 ($3 billion in loans, $500 million in grants) under the Coalition in 2022 to 1.9:1 ($3 billion in loans, $1.55 billion in grants) under Labor in 2026 (Figure 1).

This change in the composition of the AIFFP’s funding illustrates two underlying shifts. The first is the long overdue recognition that a heavy reliance on non-concessional lending was never going to be a viable infrastructure financing strategy in most Pacific Island countries. This was the case even before the regional economic and fiscal shocks that accompanied the COVID-19 pandemic. China has learned this lesson too and aid competition in the Pacific has changed. China decreased its focus on large-scale, sovereign infrastructure lending to the Pacific almost a decade ago, before the AIFFP was established, as it has in Africa and other regions.

The second, related shift is that, despite its origins in geopolitical competition, AIFFP is looking more and more like the rest of Australia’s development program in the Pacific — that is, a collection of mainly small to medium-sized, grant-funded projects. The majority of the AIFFP’s projects are now exclusively grant funded and its lending portfolio remains heavily concentrated (77% by value) in just one country, Papua New Guinea. With few exceptions, AIFFP projects now also must conform to the spending and performance targets — around climate change, gender equality and disability equity — that apply to the rest of the ODA program. In 2022-23, the Labor government passed up the opportunity to pursue ambitious reform of the AIFFP — for example, by establishing a dedicated Development Finance Institution through which Australia could cross-subsidise the provision of concessional finance to the Pacific via non-concessional development lending and investments in higher income countries — as part of DFAT’s development finance review.

The combined result of these two shifts is that the AIFFP’s additional funding will come from within the government’s existing ODA envelope. The Labor government, so far at least, has “locked-in” a 2.5% annual nominal increase (currently, less than the rate of inflation) to this envelope from 2026-27 to 2036-37. Based on the AIFFP’s current grant spending rate, the $550 million allocation equates to around four to five years’ worth of these nominal increases.

The shift to an increased emphasis on grants means that AIFFP finance will be more attractive to Pacific governments and that the demand for projects will be higher. But this increased demand will be accompanied by a critical, high probability risk — that is, unless measures to ensure that the recurrent costs of operating and maintaining completed projects are implemented, Australian financed infrastructure investments may be neglected, may degrade and, as a result, may fail to deliver on their intended development benefits. There is a long and sorry history of donors and governments in the Pacific, as well as in other regions, focusing on building new roads, ports and energy facilities without adequate thought given to the costs of operations and maintenance, with predictable results.

So, what are the options for meeting the AIFFP’s financial sustainability challenge? I set out several potential options below. These options are not exhaustive. Nor are they mutually exclusive. None is perfect and each comes with trade-offs. But they are canvassed here in the spirit of debate and discussion.

The first option would be to use AIFFP finance to reward those Pacific borrowers that have a strong record when it comes to provisioning for operations and maintenance costs. This performance-based approach has been advocated by experts from the Lowy Institute who argue that it would be “a way of channelling investments to where they will be most effective and incentivising partner governments to undertake reforms that would improve the benefit and sustainability of AIFFP investments”. Of course, a performance-based approach presumes an existing pipeline of high-quality projects across the Pacific that would generate the necessary financial returns to cover sustainment costs and/or that the incentive of AIFFP funding itself would be sufficient to drive policy reform. It is also blind to geopolitical considerations.

A second, conditionality-based option would be to link partner commitments to sustainment of AIFFP-funded and other infrastructure to the provision of Australian debt relief and grant-funded budget support. On debt relief, PNG is now repaying over $200 million per year on the five non-concessional general budget support loans that Australia has provided since COVID. Australia could offer to relieve some of this debt on the condition that the foregone repayments are directed toward agreed operations and maintenance costs of AIFFP-financed projects, as well as wider asset management reforms. In relation to grant-funded budget support, the provision of such support to countries such as Fiji and Nauru could also be more directly linked to helping co-finance the sustainment costs of infrastructure assets that have been mutually designated as high priority.

These kinds of conditionalities would involve sensitive and complex bilateral negotiations. In the case of linking sustainment funding to budget support, this would also need to be carefully calibrated to Pacific states’ individual fiscal circumstances. In the case of PNG debt relief, there would be a (relatively small) additional cost to the budget. This option may also require changes to Australia’s International Monetary Agreements Act, the legislation that governs budget support to PNG. And it would raise the thorny question of whether debt relief would be better linked to increased PNG development spending in other important areas, such as health or education.

A third, simpler and less controversial option would be for the AIFFP to pursue more co-financing opportunities with the multilateral development banks and other like-minded bilateral donors providing grant finance for infrastructure projects in the Pacific. This could help free up scarce AIFFP grant funding for sustainment costs by helping share the up-front investment burden across one or more other external finance providers. If implemented effectively, increased co-financing would have the added advantage of helping address donor fragmentation in the Pacific. But this option would not address the core challenge of increasing AIFFP clients’ responsibility for meeting future infrastructure sustainment costs.

A final option would be for the AIFFP to maintain its focus on capitalising new investments and to place the burden of meeting future sustainment costs onto DFAT’s regular bilateral and regional programs in the Pacific. While shifting these costs to other parts of the Pacific aid program would be the easiest option, it would also be the worst. Like option three, it would not address the broader sustainment challenges associated with meeting the recurrent costs of infrastructure operations and maintenance. Instead, it would simply shift these costs to a different line item in DFAT’s ODA budget. Given that Labor has mirrored the Coalition’s preference for favouring governance programs, this option would also likely have the added disadvantage of further reducing DFAT’s already relatively low proportion of spending on health and basic education in the Pacific.

As others have observed, with the allocation of more than half a billion dollars in new grant funding for the AIFFP, Australia has “doubled down” on infrastructure investment in the Pacific. The motivations for this are mixed, but this is not a reason for it to compromise the effectiveness of its development programs, particularly where it involves the spending of increasingly scarce ODA grant funding. While there is no silver bullet, the challenge is how to learn the lessons and to avoid the mistakes of the past when it comes to ensuring the financial sustainability of these investments.

Good article. Of course project sustainability is a key issue – especially for AIFFP projects – and this consideration should be right at the front of shaping projects. According to one source, nearly half of ADB transport projects (2015-2019) across the region were rated as less than likely sustainable. My experience suggests that change is needed at the infrastructure portfolio level (not just project level). Filling the sustainability gap with external funding is a temporary solution which could possibly allow a build-up of economic and fiscal headroom. However, there is a more a structural shift needed that can only happen by strengthening of mechanisms to locate accountability properly within the system. Strategic asset management mechanisms enable infrastructure managers to measure the sustainability gap, and convey to their decision-makers the value-based implications of not filling the gap – is the infrastructure being spent-down, steady-state, or appreciating and what are the economic and social consequences. While fiscal situations might dictate things, this would at least enable more transparent, outcome orientated, decision making to take place. This can be achieved by supporting infrastructure managers to think outside the project-orientated box and take a more portfolio-orientated financially-orientated approach. In my experience none of this can be sustainably fixed at the project-level. Incentive mechanisms risk being gamed to just divert funds across the portfolio.