This blog updates the Development Policy Centre’s 2022 overview of Australian aid program procurement administered by the Department of Foreign Affairs and Trade (DFAT). In 2022, Huiyuan Liu found that, despite the aid program’s being open to international competitive bidding since 2006, Australian-registered (but largely foreign-owned) suppliers dominate DFAT’s managing contractor market, and that this market remains highly concentrated. This article supplements her analysis using the 2024-25 Australian aid program procurement data recently published via Austender. As well as updating Liu’s examination of market dynamics, we discuss locally led development via managing contractor-delivered programs.

There are three things to note at the outset.

First, in 2023-24 (the latest year for which data are available) commercial contractors delivered 25% of Australia’s total official development assistance, up from 16% a decade earlier but still significantly less than the share delivered through multilateral partners (38%).

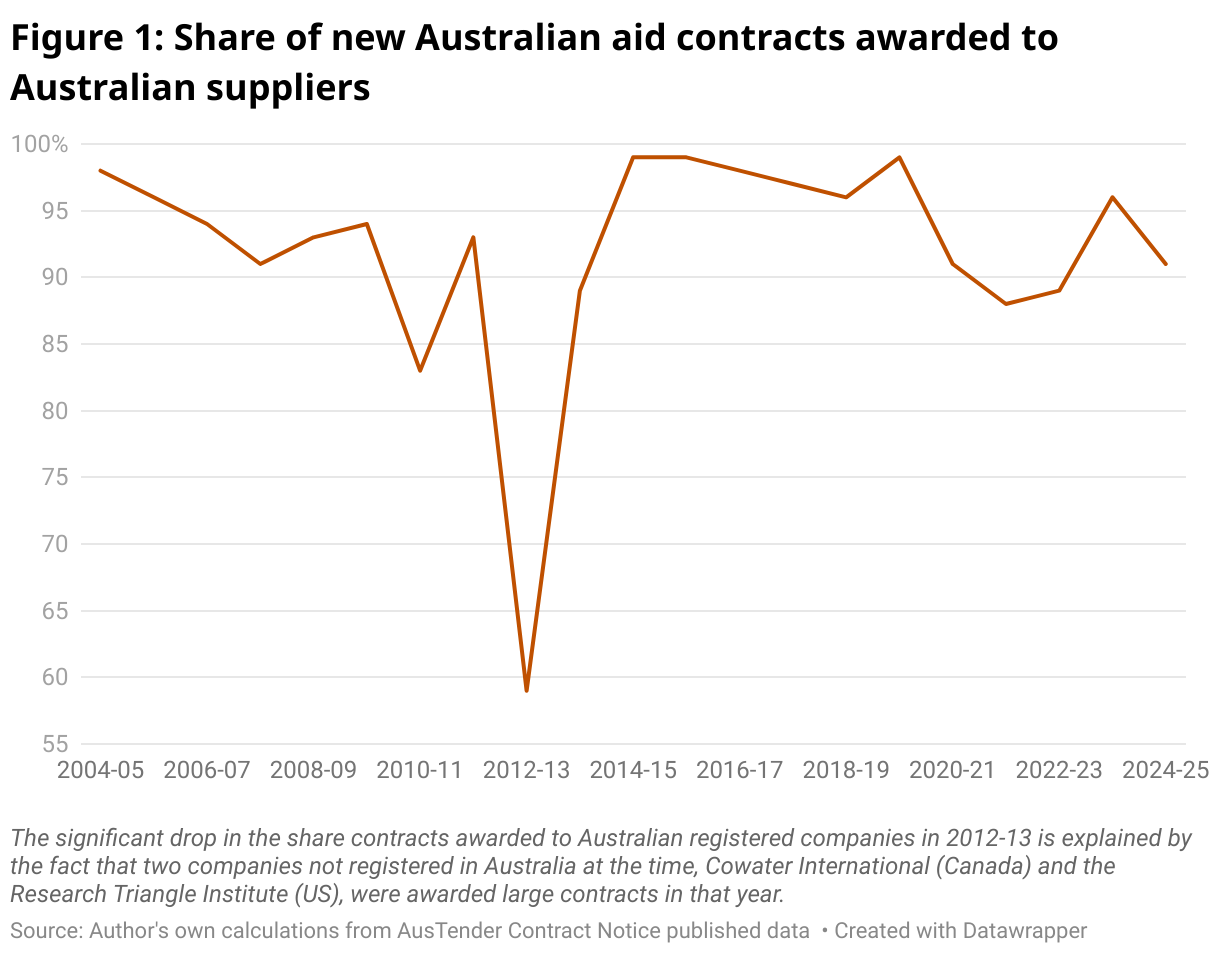

Second, the dominance of Australian-registered firms has returned after a slight dip during the COVID-19 pandemic. The share of contract awards by value to Australian-registered firms is now back at its long-term average of around 90% with recipient and third country-registered firms still largely confined to competing for sub-contracts (Figure 1).

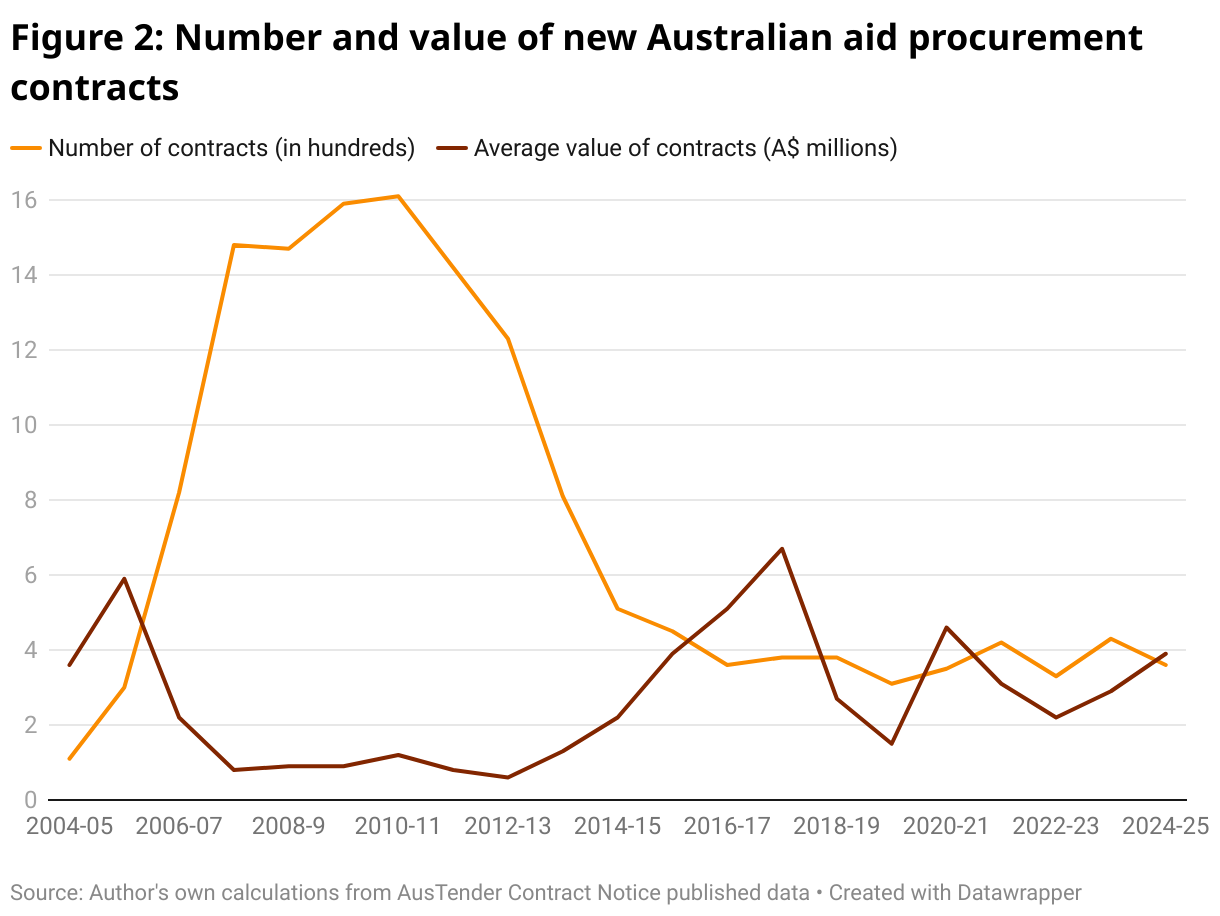

Third, the average annual number and value of awards has remained largely stable, noting the inevitable volatility in the latter category associated with multi-year contracts that often have “lumpy” payment schedules (Figure 2).

The overall trend shows a continuation of the progression toward fewer and bigger contracts, particularly when compared with the pre-2013 era, under AusAID administration. This reflects the extent to which aid management and quality functions that were once performed directly by AusAID continue to be outsourced to the private sector via large, “facility”-style programs. In at least one case DFAT has seconded its own officials into senior management roles in a commercially contracted facility that it also oversees, an approach that has had (predictably) mixed results.

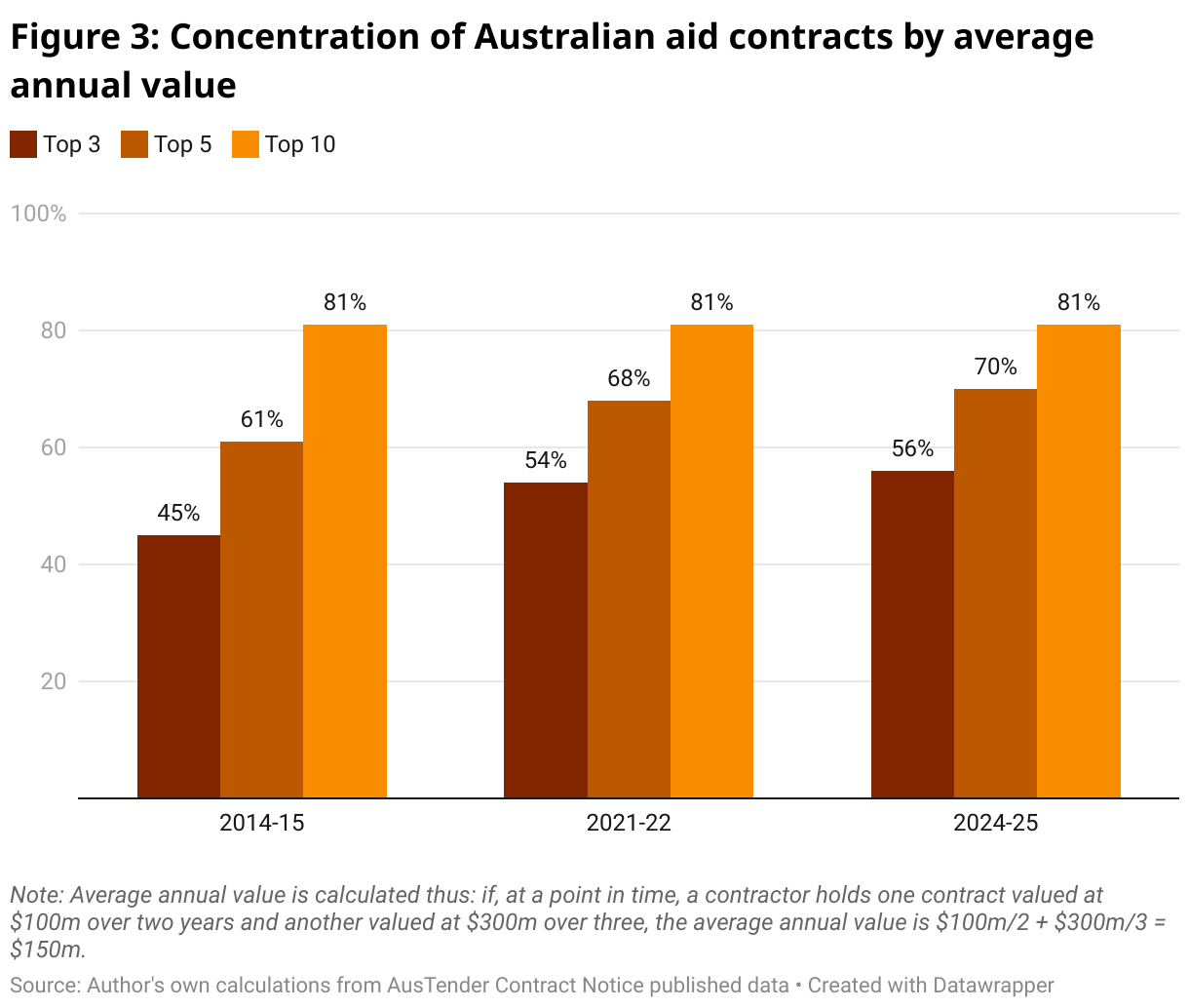

Looking at concentration — the share of contracts in terms of their average annual value held by the top firms — the trend is one of consistent annual increases in the share of awards held by the top three and top five firms. Both have steadily increased by the equivalent of around 1% per year under the Coalition (2013-22) and under Labor (2022-25) (Figure 3). The concentration among the top ten suppliers has remained around or above 80%. As Liu observed in 2022, this concentration is a function of both the larger contracts being tendered by DFAT since 2014-15 and the smaller size of the contractor market as a result of various mergers and acquisitions over the last decade.

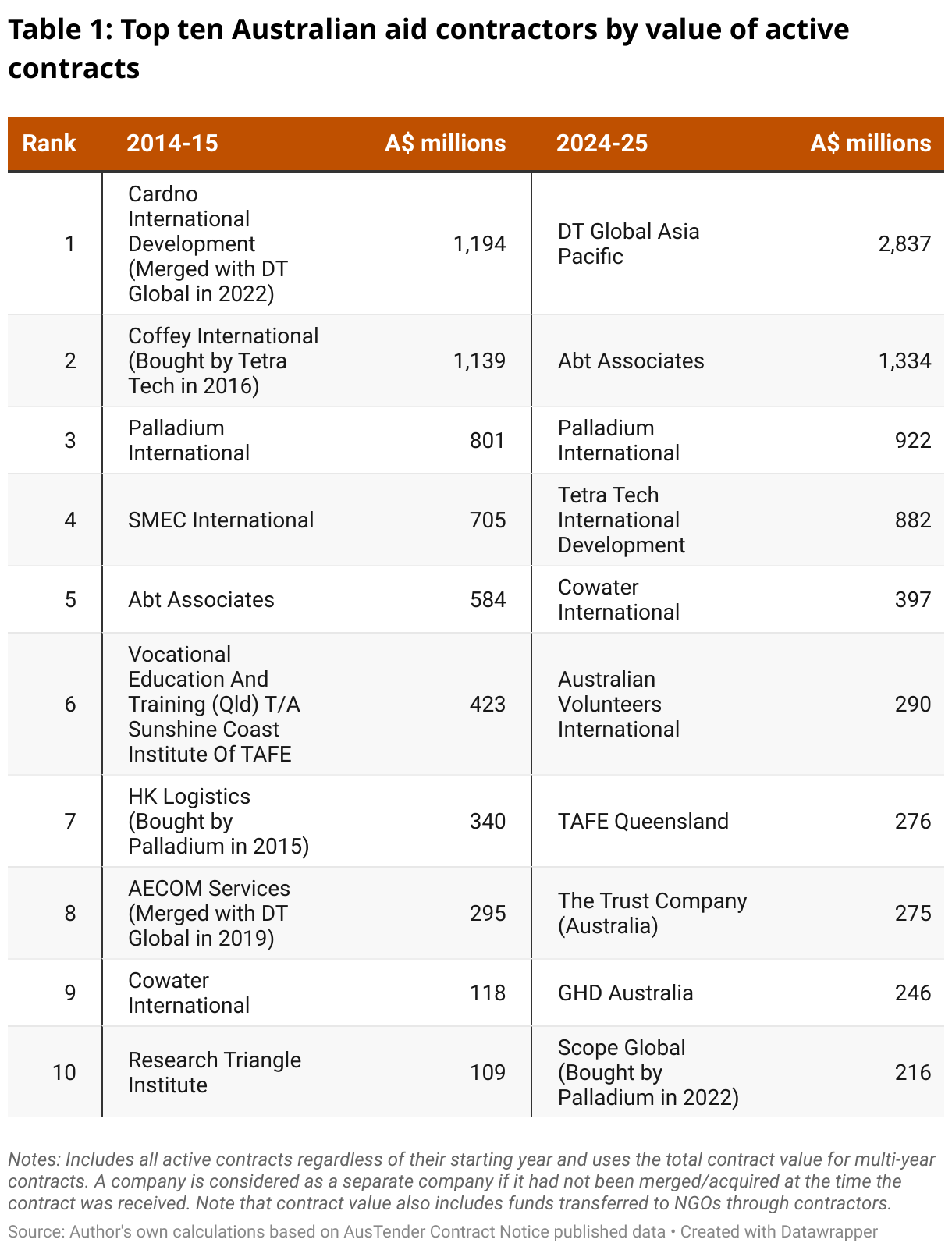

Turning to competition, there has been virtually no change in the group of firms that comprise the top five over the last decade (Table 1). In 2024-25, DT Global (formerly Cardno/AECOM) was DFAT’s largest commercial provider, holding over $2.8 billion in contracts in annual average terms, followed by Abt Associates ($1.3 billion) and Palladium ($922 million). According to one of responses to Liu’s blog (from Richard Moore) this lack of diversity might be partially explained by the fact that “profits in the industry are typically low”, discouraging new entrants.

There could well be some more competition on the way, given global aid disruptions. The Trump administration’s evisceration of the US foreign aid budget has seen the entry of several new, US-based players — Chemonics, DAI Global, the International Development Group (IDG) and the Boston Consulting Group (BCG) — into the Australian market. In December 2024, BCG won a $99 million award to administer a new seven-year phase of Australia’s economic governance program in Vietnam. Both Chemonics and IDG have been shortlisted for several current DFAT tenders, including the next phase of the Australia’s economic governance program in Indonesia, which is valued at over half a billion dollars over ten years. The arrival of these new entrants could also result in additional mergers and acquisitions.

The Labor government’s 2023 International Development Policy promised to advance “locally led development” as a core element of its wider commitment to “changing how we will deliver development assistance”. The continued dominance of foreign-owned, Australian-registered companies in DFAT’s aid contractor market raises obvious questions about how this will be reconciled with this commitment to strengthening locally led development.

One DFAT’s strategies has been to both incentivise and more systemically track the subcontracting, on-granting and employment opportunities for local companies, organisations and workers that flows from its programs via managing contractors. Earlier this year, DFAT released a new data dashboard which aggregates these statistics across the aid program. DFAT has not set any targets for these metrics but they are embedded in the 2023 policy’s performance and delivery framework and are tracked via DFAT’s annual Performance of Australian Development Cooperation (PADC) reports.

Figure 4: DFAT financial and operational data dashboard for managing contractor programs

Source: Department of Foreign Affairs and Trade, Project Electronic recording of Financial and Operational Reports Management System, 2023-24.

This quantitative approach — which could be augmented with country specific breakdowns, more detail on the seniority of contractors’ local employees and downloadable data — is useful. But it is only partial, because it risks conflating “local content” with “locally led development”. While DFAT has reported positive results against these indicators, it is hard to claim that they represent a particularly significant change in “how Australia’s development assistance is delivered” — commercial contractors have always employed local personnel and purchased local goods and services.

A more difficult set of questions concerns what demonstrable progress is being made against the qualitative dimensions of locally led development — empowerment and agency, sustainable change and mutual learning and accountability. Indeed, in focusing on local content, managing contractors might unintentionally cut across DFAT’s locally led development goals by forcing local organisations to compete against one another for project sub-contracts and grants, by artificially raising their labour costs or by subjecting them to duplicative or unnecessary administrative processes and onerous parallel systems. In addition, as Mark Moran has recently highlighted, the question of who is genuinely regarded as “local” by communities in the villages and districts of partner countries is also an important consideration.

These dimensions of Australian aid practice (both intended and unintended) are complex and cannot be captured in a dashboard. DFAT’s own policy guidance on locally led development rightly acknowledges this complexity and emphasises the importance of country context in seeking to understand what change and progress might look like — an approach that some managing contractors have mirrored in their corresponding frameworks.

As well as rigorous case studies, independent evaluations and academic research, a useful baseline against which to measure progress against these aspects of locally led development in managing contractor-delivered (as well as other) programs may come from the results of DFAT’s inaugural biennial perceptions survey. These results are expected to be published in DFAT’s next PADC, scheduled for 2026.

Another quite significant statistic is the change in nationality/ ownership of the top firms delivering the Australian Aid Program.

From 2014, where the top 7 contractors were all Australian owned – to today, where the top 4 contractors are now all U.S. owned (Palladium is owned by GISI), Cowater is Canadian, and the first Australian firm, AVI, enters the list at number 6 – delivering a mere 4.6% of the combined value of all contracts going to North American companies.