Government revenues from Papua New Guinea’s mining, oil and gas sector have essentially dried up. With the ongoing effects of the devastating earthquake in Hela province, the eruption of election-related violence in the Southern Highlands, a significant budget shortfall, and a foreign exchange crisis driving business confidence down, the resources of the government are severely stretched… and the massively expensive APEC meeting looms in November.

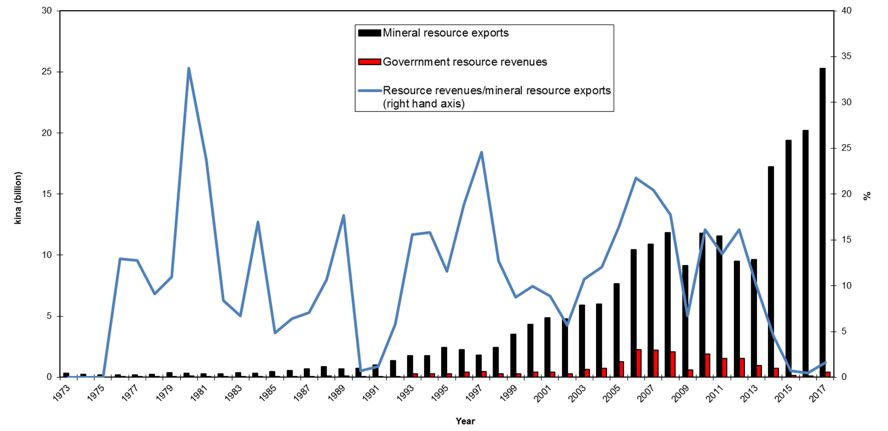

In this context, the drop in government revenue from the resource sector is staggering, and accounts in significant part for the growing fiscal stress. Figure 1 shows the extent of the issue: in 2006-2008, according to BPNG figures, the government collected more than K2 billion annually from the sector by way of taxes and dividends, on mineral exports that had just topped K10 billion for the first time. In 2017, the figure is just K400 million on exports of K25 billion – a revenue reduction of more than 80% in the same time that exports have increase by 150%! Government dividends and corporate taxes made up just 1.6% of the value of exports in 2017 (and that was a significant increase over 2015 and 2016). If we take the long-term average share of the value of exports that the government has received (at a little over ten percent), this points to a potential ‘hole’ of at least K8 billion over the past four years, an amount that would go a long way to covering the current fiscal deficit.

Figure 1

Source: BPNG. Resource revenues are defined as “MRSF receipts,” that is, the receipts that used to go into the Mineral Resource Stabilisation fund. Even though the MRSF no longer exists, BPNG still records resource revenues, which include corporate tax and dividend payments from resource companies.

There are some precedents for the rapid drop in government revenues from the sector, as Figure 1 show. In 1990 and 1991 – just as the ‘resources boom’ triggered by the Porgera gold mine and oil production at the Kutubu oilfield began – revenues collapsed, largely due to the closure of the Bougainville copper mine in 1989; and again, briefly in 2009 due to the onset of the global financial crisis in 2008. But neither of these has been as deep or as sustained as the current hole.

A full explanation of the precipitous decline in resource revenues is beyond the scope of this analysis. Clearly, a number of factors are involved, including a fall in commodity prices, major construction and expansion costs (which attract accelerated depreciation provisions) and generous tax deals. The revenue dry-up of the past four years also reveals that the State bears a disproportionate share of the risks associated with resource projects and investments. If we go back to the original intent of the post-Independence mineral policy, it was to translate mineral wealth into broad-based development across the whole country:

‘…known mineral resources should be developed for the revenue they can provide to the Government’ (PNG Department of Finance 1977: 2).

This clearly has not happened in the last four years. And certainly the Treasurer can’t be critiqued for commissioning yet another fiscal review: this seems appropriate, although whether it effectively addresses broader issues of a ‘fair share’ of mineral wealth remaining in PNG remains to be seen.

While there is much less money coming from the resources sector, there is at least better data than there used to be. The Extractive Industries Transparency Initiative (EITI) is a global initiative begun in 2002 to give transparency to what were regarded as often opaque flows of resource revenues from multinational companies in the extractives sector (especially oil) to the state in the countries in which they were operating. It is a voluntary initiative in which countries (and companies) can elect to become a ‘candidate’ country, and so long as they are able to be compliant with EITI standards, they can be admitted as a full member of EITI. The key requirement is to be able to report in a reliable way (through third party audits) on the revenues paid by companies, and reconcile these with payments received by the different arms of the state. The involvement of all parties – companies, governments and civil society – and public communication around the event and its products is also seen as central to both transparency and raising awareness of the nature of resource revenues and their destination.

PNG initiated its involvement in EITI in 2012. Four annual EITI reports have so far been produced (for the years 2013 to 2016). These reports provide an increasingly rigorous and transparent set of data on flows from the sector to the government, and identify additional revenue streams to the government than what BPNG use (and have used for the past 40 years). When all the additional revenue streams that EITI identify are included, the total share of the value of mineral exports rises to around 6.5% for 2017, up from the 1.6% based on the BPNG data. EITI is not without its problems and the most recent PNG country report identifies areas where it needs to be strengthened in PNG, and a focus on companies rather than operations can lead to the obfuscation of total flows and payments from each mine, oil and gasfield. In the PNG context, an examination of the sub-national flows and audit trails is also significant, and an initial study into this is underway.

One surprising revelation from EITI is that the single largest revenue stream from the mining, oil and gas sector to the government for at least the last two years has been so-called “group taxes”: the taxes paid on the wages and salaries earned by employees in the sector (Figure 2). These were worth more than K500 million in both 2016 and 2017, and in 2016 represented 34% of the revenue streams from the sector to the government, as identified by EITI. This is significantly more than the K46-88 million in corporate income taxes, K200 million in dividends paid to the State, or the almost K200 million paid in royalties in 2017. These group taxes are likely to be a more stable revenue stream than taxes or dividends – the workforce is unlikely to expand and contract to the extent that it impacts on the taxes they pay (leaving aside construction phases), or at least not as much as global commodity prices and profitability. But – and here we come back to the issue of PNG securing a fair share of its mineral endowment – this is a tax on the labour used to extract the resource, not a means of necessarily securing a direct share of the value of the resource itself.

Figure 2

The second area where EITI has revealed some interesting questions is around the operation of the Infrastructure Tax Credits (ITC). ITC originated in the sector in 1992 when the Porgera Joint Venture negotiated with the state to use a portion of their taxable income to directly provide infrastructure for surrounding local and provincial governments in exchange for a tax credit on this spend. Over the years the value and the uses of the ITC have varied, including at times supporting various national projects, and has been the subject of debates in various reviews as to its value. In 2016, four companies reported expenditures of K135 million in tax credit projects to DNPM[i], a significant amount that could well have contributed significantly to local and provincial development aspirations… but we don’t really know given the relatively poor reporting of the outcomes of these expenditures. More significantly, though, it is difficult to reconcile the size of these expenditures with the actual taxes paid by the four companies, which come in at well under K100m in total. That tax credits have come to exceed tax payments should ring alarm bells, and would explain why the government has in fact put a temporary stop on them.

Going forward, we would suggest two additional areas of focus, based on the above analysis. This first is local procurement. What is clear from the EITI reports (and earlier work by Banks (1990) on BCL) is that extraction of minerals is an expensive process, and a significant amount of the value of the mineral resource is spent by the companies on the labour, machinery, fuel, food, and the multitude of other costs needed to extract and export the mineral resource. An analysis from the last year of the Bougainville Copper Ltd mine at Panguna revealed that an estimated two thirds of the value of the mine accumulated directly outside Papua New Guinea, and indirect or second round spending would increase this (Banks 1990: 108). Imported materials and services made up 23% of the total value of the gross revenue of the minerals exported, cost of sales (all spent offshore) another 13%, depreciation 8% and dividends to non-PNG shareholders 12%. Local content spend on materials and services sat at just 5.5%, less than a quarter of the equivalent imported costs, while in total local wages and salaries were around two-thirds of the expatriate salary costs, despite the much greater numbers of local employees.

A long-standing objective and challenge for the State has been to find ways to ensure a larger proportion of these capital and operating costs are spent on PNG-based labour and other inputs. Plans at most of the major operations have been successful in localising the workforce significantly, hence reducing imported labour (and costs) at operations over time, although foreign labour continues to be important during construction. In terms of the goods, services and materials used to construct and operate a mine though, there appears to be scope to increase the proportion that is spent and retained locally. In large part this is tied to corporate and state support for a stronger local small business sector that can effectively service these mines (and potentially service the growing extractives industry across the Pacific).

The second area to which attention needs to return is the Sovereign Wealth Fund (SWF). This Fund, which would serve the dual function of saving a component of the resource revenues and having a portion committed to developmental needs through the budget, is in place (in terms of the legislation for it) but has not yet been implemented by the government. This well-proven mechanism for translating immediate resource revenue into a long-term sustainable fund can play a critical role in reducing the volatility of flows to the government. Ironically it may be that the factor holding back the government from moving on its implementation is the dire need for all the resource revenues right now. But neither is it sensible to wait for revenues to return to high levels before initiating the SWF: it will almost be certain that political and bureaucratic processes would delay the first flow of revenue to such an extent that several years’ worth of revenues that could kick start the fund would be lost. In other words, in many ways this period of low revenue is an excellent time for the Fund to begin.

So, the answer to the question of where have all the resource revenues gone, is not a simple one. The EITI reports show that a range of factors at the different operations (accelerated depreciation, tax holidays, ITC and re-capitalisation in plant expansions etc), have impacted on the revenue flows to government. To this we can add global commodity price drops, a compromised fiscal regime and some less-than-transparent governance structures and processes. The fact remains though, that over the past four critical years in its development, Papua New Guinea has missed out on a ‘fair share’ of the value of its mineral resources that have been extracted.

[1] Although confusingly there are different figures recorded as tax credits claimed by the companies from IRC – where the total credit offset against tax from three of the four companies come to K54million.

References:

PNG Department of Finance (1977), Financial Policies Relating to Mining and Mining Tax Legislation: Statement of Intent. Waigani: October.

Banks, G. (1990), Minerals and Development in Papua New Guinea. Unpublished MSc Thesis, Department of Geography, University of Canterbury.

It may be useful if I add a few more comments on the issue of the ‘fair’ return that PNG gets from resource development. These comments are additional to those made on August 21.

That there is a significant amount of reveue derived from sectoral employment taxation should come as no surprise. This revenue stream comes off the front end of all resource development projects and is unaffected by the CAPEX debt amortisation and interest payment arrangements of any of the co-venturers for all kinds of projects.

When analysing the aggregated BPNG figures for both company tax and dividend payments it needs to be kept in mind that these two sources of GoPNG income are subject to various influences which include not only commodity price variation but also production variation from a wide variety of causes including, for example the influence of drought on Ok Tedi output in 2014, the reconfiguration of mining operations from underground to pit, the reconfiguration of Kutubu for gas (gas re-injection has been taking place for many years), the closure of Mananda, the Lihir construction of a geothermal power plant, to name a few.

At present the PNG LNG Project is a dominating influence because of its very large CAPEX and relatively thin income stream (no big ‘windfalls’ as there is from oil). This makes the financing of the project of considerable significance. The financing arrangements extend over 15 years for the licence share owners, except for the GoPNG interest which is said to be for 12 years. So how do the financing arrangements affect the rate of return to GoPNG? The short answer is that we don’t know but we can get a partial picture from OSL reports published on the ASX (http://www.openbriefing.com/AsxDownload.aspx?pdfUrl=Report%2FComNews%2F20180501%2F01977352.pdf)

The OSL report gives us a chart on page 21 for an ‘Indicative PNG LNG Repayment Profile’, distinguishing between interest and principal repayments. For 2018 principal repayments are about USD$ 375 million, interest payments about USD$ 175 million. Interest rates are not stated. Perhaps they are about Libor + 4%.

A chart on page 24 shows the Oil Search PNG LNG debt amortisation falling from a 2017 high of about USD$ 3 billion to zero in 2026.

GoPNG LNG Project equity (Kumul plus MRDC) is about half that of OSL. Term finance is for 12 years and the rate may be Libor + 6% or less. It is possible that the Kumul loan repayment obligations may also end c. 2026. However, from 2021 Kumul debt service obligations may well rise above current projections as it incurs new obligations in respect of the PNG LNG expansion and the new Papua LNG Project. Accordingly, it seems likely that a significant upward lift in company tax and equity dividends from the enormous LNG resource development projects will not occur at least until the early 2030s.

PNG has joined with major oil companies in the making of some very large long term bets. But we should be very grateful that GoPNG participation in resource development has created a ‘front-end load’ of benefits for citizen beneficiaries. An unusual form for a Sovereign Wealth Fund.

Perhaps GoPNG should seek to source its forthcoming LNG project development equity funding through the AIIB where it may be granted a rate of Libor + 1.5%.

Vailala

I thank the authors for this interesting blog-post. As the authors say the BPNG statistics that follow the old MRSF reporting model (BPNG Table 7.2 (https://www.bankpng.gov.pg/statistics/quarterly-economic-bulletin-statistical-tables/) show a marked discrepancy between the posted value of mineral resource exports and the aggregated value of resource company taxes and resource development SOEs dividend payments.

But the BPNG tables are only a small part of the overall picture as the recent EITI report makes clear. GoPNG has, following the Bougainville crisis, for many years pursued a strategy of increasing the value of both direct cash payments and quasi-fiscal sub-national payments to resource project-affected landowners, LLGs and PGs, especially so in relation to petroleum projects.

The balance that was struck between the national interest and the local interest has moved from the initial Bougainville point of about, say 98:2 to somewhere near 70:30 in terms of benefit flows. In population terms the perimeter fence that establishes who will receive both direct (cash payments) and less direct local area benefits from resource development has greatly expanded beyond the confines of the original Special Mining Lease context. For example, the expansion of Ok Tedi benefits to encompass downstream project-affected landowners. This expansion has proceeded apace in the petroleum projects with the PDL concept of large graticular blocks and petroleum pools that extend over several such blocks. The PNG LNG project and the ‘unitisation’ concept has further enhanced this tendency. In the interests of resource contract stability and the creation of a social licence to operate GoPNG has increasingly found ways to divert resource project benefit streams into the hands of landowner beneficiaries, LLGs and PGs. There has been an evolution of the PNG legal regime for resource development. Under the Petroleum legal regime the royalty, development levy and landowner/PG equity shares, are taken off the front-end of the project and are the property of the recipients, held in trust accounts, and are not part of the GoPNG project-derived central government revenue stream, at least not in the form of taxes and SOE dividends.

In addition to these changes, all of which have an impact on the quantum of the GoPNG benefit stream, there are other public goods investments derived from resource development projects. The easiest of these to quantify are the Infrastructure Tax Credit (ITC) arrangements to which Paul Flanagan relevantly draws to our attention. At present ITC arrangements are only to be found in the PNG LNG Project and they are specified and described in Exhibit F of the PNG LNG FID (https://www.banktrack.org/download/png_lng_gas_agreement/080522_pnglngagreementexecutionversion.pdf). For the LNG Project GoPNG has allocated K1.2 billion divided over two five year periods. The scheme covers 107 km of public roads, including 23 bridges and about 7000 metres of culverts. The construction cost is offset against the LNG Project companies tax liabilities so the effect is of a direct transfer of benefits from the national to the local/regional interests. It is also, of course, revenue foregone by GoPNG. The ITC arrangements are currently the subject of GoPNG review. It may be that the better GoPNG option is not to finance these projects by way of tax credits but to bring them ‘shovel ready’ to the AIIB for concessional financing. Certainly the funding of rural roads is difficult to justify using conventional World Bank/ADB assessments in terms of EIRR and FIRR measures. Recourse to Chinese development thinking may be an effective way around these conventional economic road-blocks.

As the EITI report notes (p. 142), in order to understand the economic effect of resource projects in PNG, it is necessary to develop a much better understanding of the role of sub-national payments in both mining and petroleum projects. There also needs to be improved reporting. For example there needs to be better analysis of the quasi-fiscal payments made by OSL and ExxonMobil. Listed payments for 2016 were K43 million (OSL) and K 80 million (ExxonMobil, this later figure is garbled in the EITI report). The EITI report lists these items as discretionary social expenditure but information is not available to fully assess the infrastructure and socioeconomic development impact of these expenditures. However, it should be noted that both companies employ PNG staff who are actively engaged in responding to community welfare and development proposals. ExxonMobil’s focus on local economic growth appears to be both well-thought out and well-implemented by its PNG staff.

My point is that all of these various expenditures variously contribute to meeting community development needs and infrastructure development. Collectively they have not merely a local effect but also a pervasive effect on the wider area, the province and the nation as a whole, difficult though it may be to capture all this in a conventional cost/benefit analysis.

Despite the fact that many years have elapsed since the LNG Project Social Mapping and Landowners Identification Studies should have been completed it is still unclear as to exactly how many people will be directly affected by LNG Project infrastructure investments and royalty and development levy payments. Estimates vary between a low of 30,000 to a high in excess of 60,000. Assuming, as a minimum, at least 8000 households and estimating a cash equivalent for income derived from subsistence production it may be that a project-affected household will experience a doubling of their household income when the royalty benefits and other benefits are finally paid. But I attach no significance to this estimate because it is entirely speculative.

But there is an additional point here that relates to the discussion of the proposed sovereign wealth fund and the usual Norway model for the natural resource development context. Proponents of an SWF rarely refer to the World Bank’s Chad-Cameroon Pipeline debacle. What receives only a bare passing mention in the BPNG discussion paper on the PNG proposed SWF is the Alaska Permanent Fund. This Fund makes cash payments (currently USD$1,600) on an annual basis to all Alaska residents. This is the Permanent Fund Dividend. The creation and structuring of the Alaska Permanent Fund were motivated by a belief held by many citizens that at least a portion of the revenue derived from oil exploration and development that accrues to the State should fall outside of political control.

In effect PNG has created its own improved version of the Alaskan arrangement. PNG has achieved a sharper division between politically controlled resource derived expenditure and household controlled resource derived expenditure. We know that delivering cash payments into poor housholds has an effect on welfare (including nutrition, health and education) and that these improvements in turn lead to improvements in productivity, especially in a poor rural subsistence economy.

As far as GoPNG LNG Project derived equity income is concerned the arrangements are briefly summarised in the EITI report which mentions GloCo, the SPV that handles gas marketing sales proceeds and ensures repayments to the project lenders (p 103). No doubt the requirement to pay back lenders is greatly constraining the growth of the Kumul equity interest dividend. Some information on the financing of the LNG Project can be found here -http://www.gastechnology.org/Training/Documents/LNG17-proceedings/1-6-Steven_Kane.pdf

As a final comment on ‘fairness’ I think it is appropriate to point out that GoPNG embraces resource development by entering into unincorporated joint venture (UJV) arrangements with developers. A UJV arrangement is preferred in many cases because it is a risk management or mitigation device for the co-venturers. A UJV is typically not a legal entity. The relations between the co-venturers are governed by contract in the form of the Joint Venture Operating Agreement. The co-venturers obligations are to meet the project capital expenditure obligations in proportion to their respective licence shares, apportion costs across the respective licence shares and to take their profits accordingly. Generally speaking a concession made by GoPNG to the resource developers is, pro rata by licence share, benefits the SOE that holds the GoPNG equity share in the licence. With these points in mind the LNG Project is no more, or less profitable for GoPNG than it is for ExxonMobil.

Vailala

Hi Glenn and Martyn. Excellent article – thanks. Three comments. First, the input-tax credit impact is possibly more significant than you indicate. ITCs totaled K901.2m from 2013 to 2016 according to p88 of the 2018 PNG Budget. Oil Search was by far the major user (abuser?) of this scheme, accounting for 56.5% of expenditure for ITC projects from 2013 to 2016 – p89 of 2018 Budget). On top of this, Oil Search is constructing APEC Haus through a K170m ITC arrangement (p90 of 2018 Budget) without any tendering process or other usual public procurement arrangements to protect the use of scarce PNG taxpayer funds. Second, the current SWF has a very major flaw in that Kumul Petroleum can divert any dividend revenues into its own operations – this is a major risk to good use of government funds as well as the SWF’s counter-cyclical objectives and should be corrected before the fund is operationalised. Third, on low revenues, there is also the possibility of at least active tax minimisation activities by the major companies – it is hard to describe Exxon-Mobil’s PNG activities being owned through a complex chain of companies extending through well known low tax countries other than in the context of this possibility (see Jubilee Australia report on the PNG LNG project). Expansion of PNG Internal Revenue Commission’s large taxpayer office is a welcome development. Thanks again. Paul.