When we think of resource-dependent economies, we normally think of the Middle East, and economies like Saudi Arabia. Where does Papua New Guinea fit in?

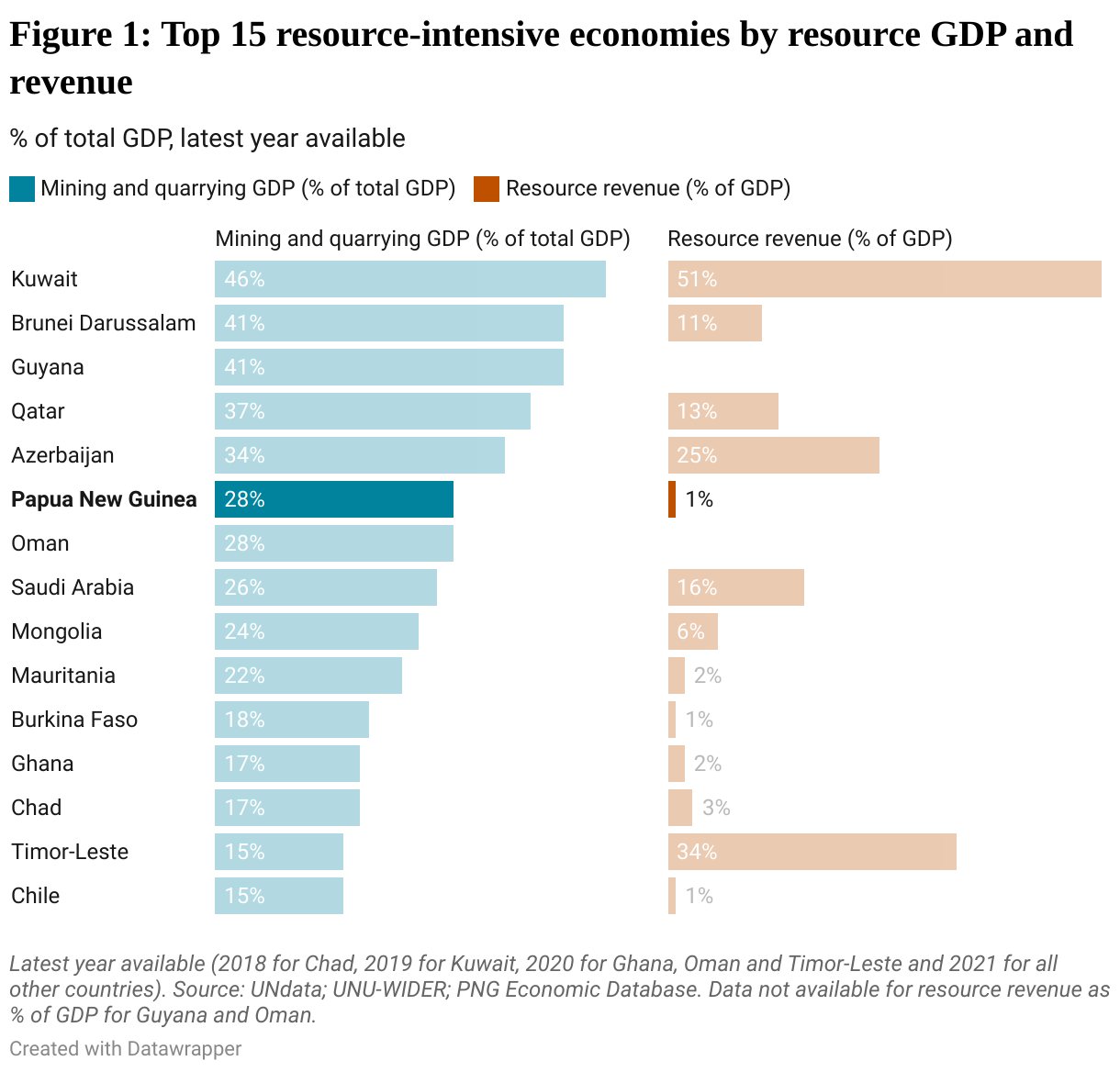

Data available from the UN allows us to isolate value added in the resources sector from the rest of the economy (resource GDP). The ratio of resource to total GDP is a measure of resource dependency. This is available for 106 countries, and the top 15 are shown in the graph below by the blue bars (left hand side). The data is for the latest available year, which for most countries, including PNG, is 2021.

PNG comes in sixth place, just above Saudi Arabia.

We’ve told this story before using a different data set, based on World Bank data on resource rents. Writing in 2019, this indicator had PNG in tenth place, actually just below Saudi Arabia. But the resource rent measure is difficult to estimate as it requires estimates of the cost of production. Resource GDP is a more reliable measure as it comes straight from the national accounts. That said, some countries are missing from the UN data set: Democratic Republic of the Congo, Iraq and Angola for example.

Whatever its precise ranking, the overall message is clear: PNG is one of the most resource-dependent economies in the world.

How did this happen?

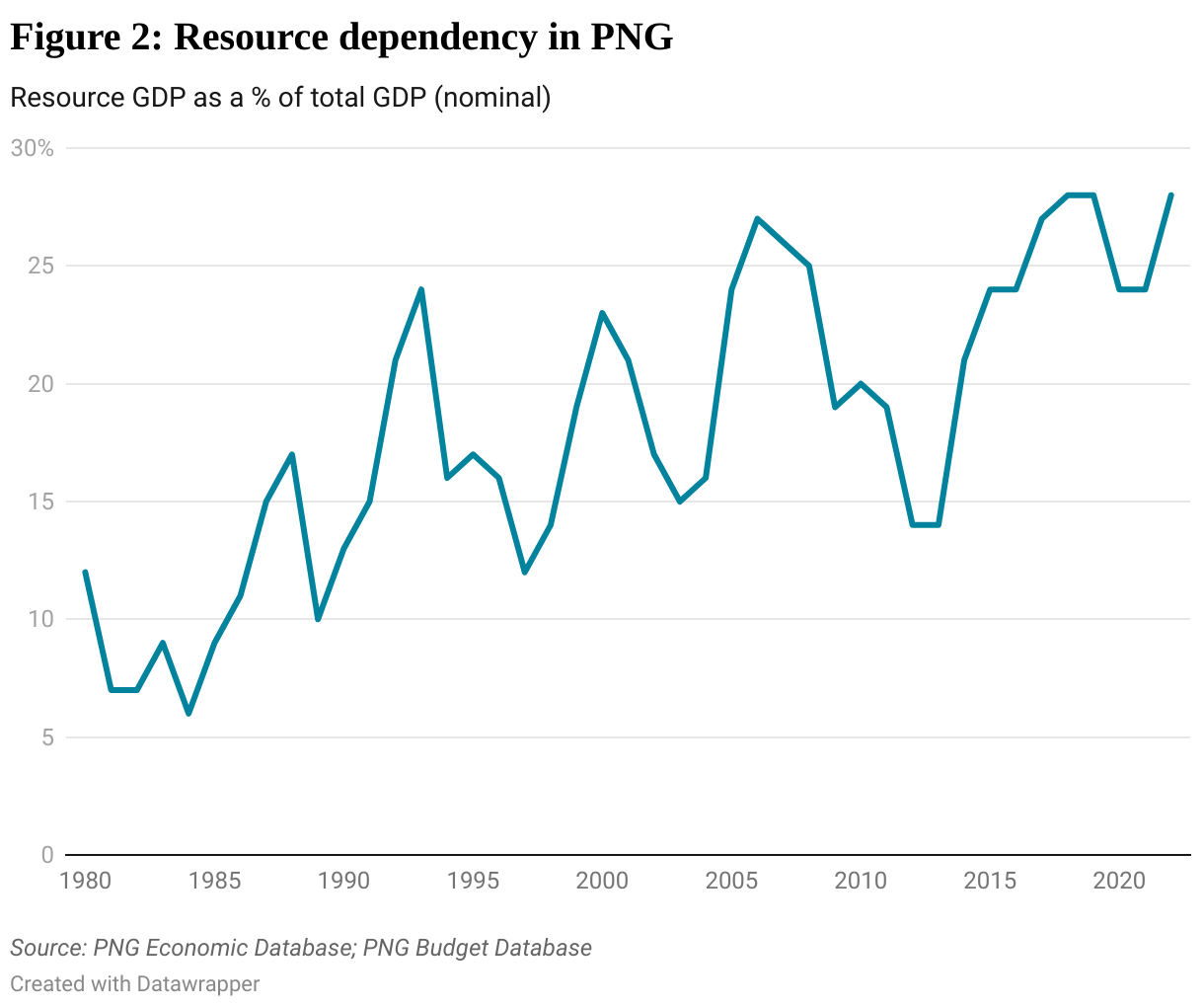

At independence, PNG’s resource sector was represented by a single mine, the now-closed Panguna copper mine in Bougainville. Looking at a graph of resource dependency over time traces out many of the key developments in PNG’s recent history (Figure 2). The ratio fell in the early 1980s as copper prices fell, but rose in the late 1980s as those prices recovered and as the second mine, Ok Tedi, opened. The resource-dependency ratio fell again sharply in 1989 when Panguna closed due to conflict in Bougainville, but soon hit a new high in the mini-boom of 1993 – of 24% – due to new oil projects and the new Porgera gold mine.

Resource dependency then fell as oil production declined, but increased again in the late 1990s with new oil fields and the Lihir gold mine. The 24% record of 1993 wasn’t broken though until the resource boom years of the 2000s when commodity prices skyrocketed. A new record of 27% was set in 2006. Then the ratio fell as commodity prices eased and as PNG LNG construction boosted the rest of the economy. (Construction of a resource project is not counted as part of resource output.)

The dependency ratio started on another upward cycle when liquified natural gas exports began in 2014 and reached a new record of 28% in 2019. COVID-19 caused commodity prices to fall, and Porgera was closed, so the ratio fell again, but now the Ukraine war has pushed oil prices up and the ratio is back up to 28%.

In summary, the resource sector is a bigger part of the PNG economy than ever, and a bigger part of it than nearly all other economies. PNG really is the Saudi Arabia of the Pacific. This important finding has several implications and raises some important questions.

First, GDP is an increasingly meaningless indicator for PNG, given the high foreign ownership of the increasingly important resource sector. We should focus on non-resource GDP as a better measure of national economic activity.

Second, it helps explain many other features of the PNG economy. For example, the ‘Dutch disease‘ associated with resource dependency helps explain why PNG is a high-cost economy. When this high level of resource dependency is also combined with PNG’s low level of urbanisation (the lowest in the world), it also becomes clear why income inequality in PNG is among the highest in the world. The benefits of resource dependency are not widely shared.

Third, one benefit of resource dependency should be government revenue generated from the resource sector. Figure 1 also shows resource revenue (the brown bars on the right hand side), using data from UNU-WIDER. It’s clear that the amount of resource revenue collected by resource-intensive economies varies significantly.

Yet PNG’s resource revenue is noticeably low considering the size of its resource sector. It appears to be getting less out of its resource sector compared to other countries. Why this is needs to be urgently understood.

While the resource sector is no doubt important to PNG’s future, the historical trend and international comparisons shown in this blog suggest that it is unlikely that the secret to economic success in PNG is more resource projects. If it was, the country’s economic success would be obvious for all to see.

Yes, it really is a an odd misnomer that PNG is one of the most resource dependent economies in the world, when ( unlike say in Saudi Arabia et al) relatively few in PNG are directly or even indirectly employed or dependent upon these extractive industries. Yes, some are,largely in enclaves but also those supplying the mines through the supply chain, but most formal and informal employment, plus household livelihoods, comes from agriculture and related activities, which really provide PNG’s backbone.

If the revenue flow from the resource sector was solid and consistent, and public expenditure well targeted and much more accountable, the State could support the needs of rest of the economy and household welfare needs better, but the Dutch disease in various forms has been making a discretionary effect for a long time, but with govt policies so misguided and uncoordinated over the past decade or so the potential beneficial effects have been subsumed… rather than a Sovereign Wealth Fund, for example, to ameliorate negative resource sector impacts, we have a combination of costly debt and accumulating public funds concentrated in the same sector from which that revenue is sourced, rather than invested in diversification, or used to sanitise exchange rate pressure into the future…

A major factor is that extractive resources are there, which provide opportunities and temptation and lure the wrong people into politics.. self-serving rather than serving people. But another factor is a relative weak and ill-informed civil society, which is perhaps surprisingly respectful or submissive to leadership. This isnt really so surprising, as there is a commendable respect for traditional leadership, but now also because so much of public funds and appointments have been coveted by political leaders, including under remarkable discretionary constituency gra tks, that people gain opportunities not from merit but from allegiance..