Papua New Guinea’s provinces raise their own revenue to help fund the services they deliver. Though reported by the Department of Treasury and the National Economic and Fiscal Commission (NEFC), not much is known about how provincial revenue has performed over time. In this post, I discuss how provincial revenue has performed since 2007, and assess the extent to which provincial revenue has been able to meet costs.

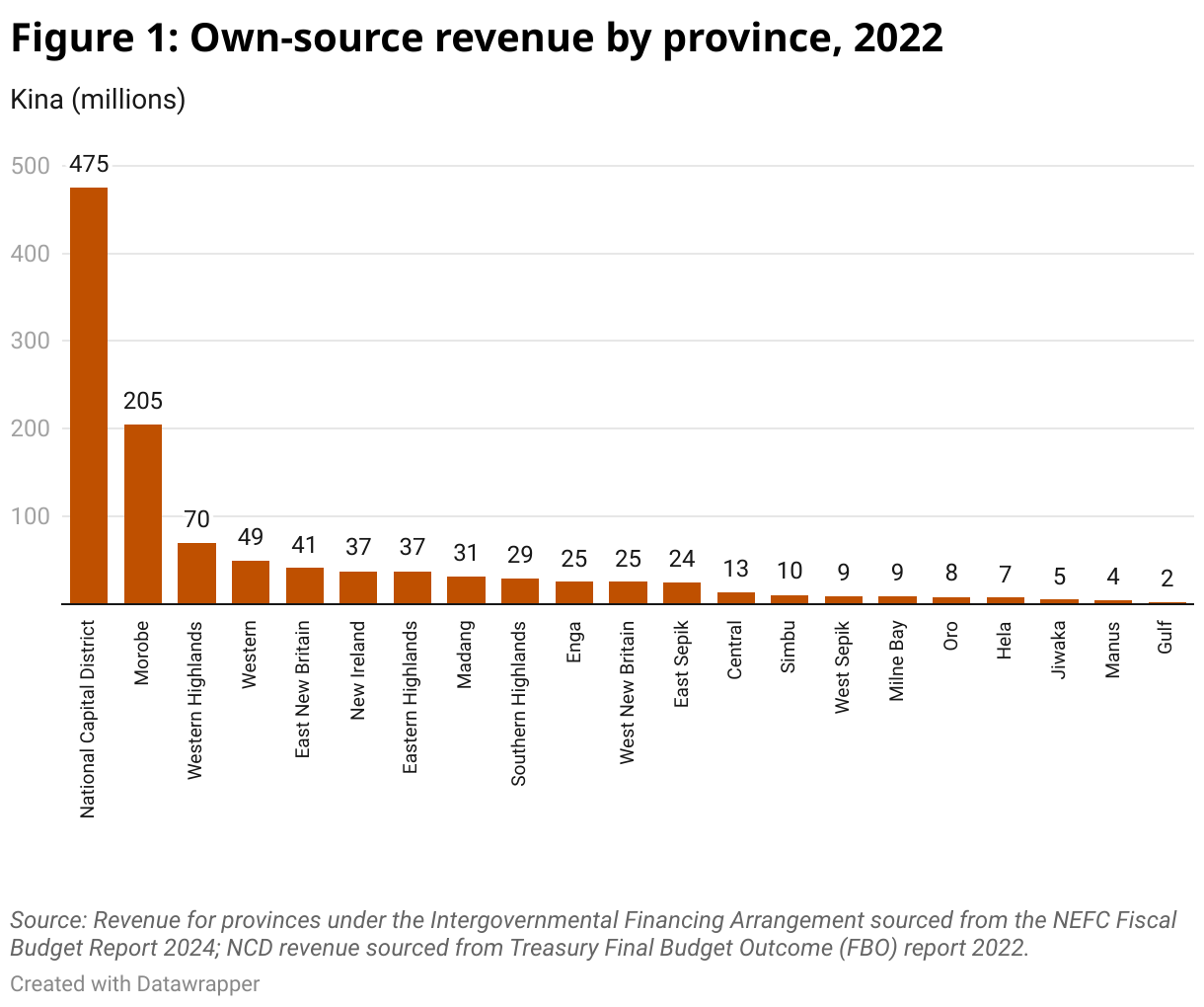

Real (adjusted for inflation) revenue raised by all provinces in 2022 was K1.1 billion, 6% of total government revenue. As shown by the chart below, more than half of this revenue was raised by two provinces: National Capital District (NCD) and Morobe. In 2022, Gulf raised the lowest level of real revenue, revealing the large inequity that exists between provinces. Low levels of revenue collected in many provinces have affected their capacity to meet spending needs, raising their dependence on national government.

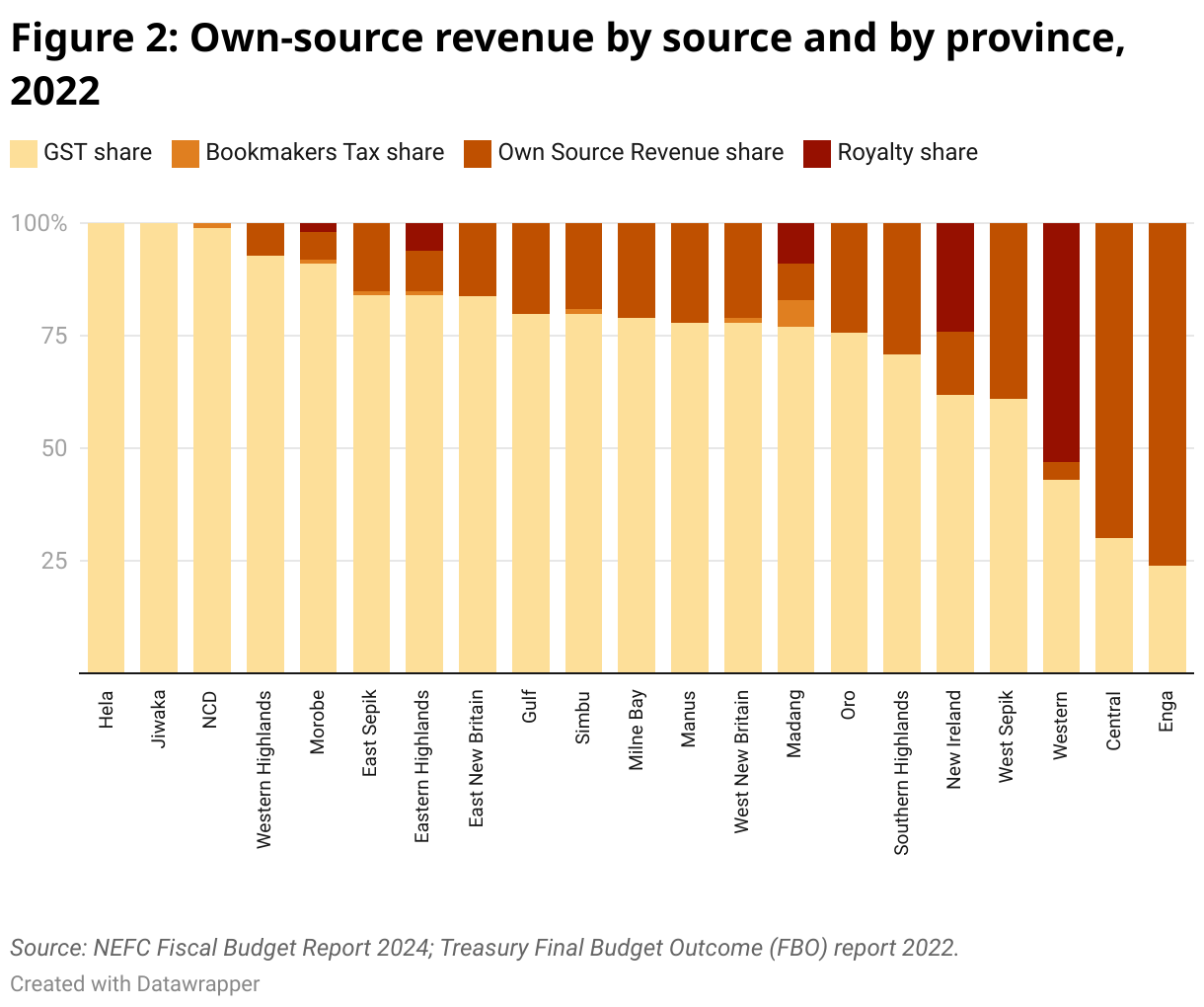

Provincial governments have limited revenue raising powers and are mostly dependent on the Goods and Services Tax (GST). The national government, through the Internal Revenue Commission (IRC), is responsible for collecting GST (remitting to the provinces 60% of GST excluding on imports) and bookmakers’ tax (remitting 40%). Provinces have three other sources of finance. They receive the provincial share of royalties from resource projects. They can also raise revenue directly through dividends on profits from investments, but few have investments or the capacity to invest. The third provincial revenue source, called own-source revenues, comprises income from licenses for liquor outlets and gambling establishments, motor vehicle registration and license fees, proceeds from business activities, rents and asset sales, provincial road user taxes, court fees and fines and other fees and charges.

In 2022, GST contributed 87% of total own-source revenue for all the provinces together. For 18 provinces, GST contributed all or most of their revenue. Hela and Jiwaka were solely dependent on the GST, while Enga and Central were the least dependent on the GST. While Department of Petroleum and Energy receives royalties from the PNG Liquefied Natural Gas project on behalf of Hela, it is unclear whether Hela receives them — the NEFC does not report royalties for Hela. It is also unclear why Enga and Central do well on own-source revenue.

Although PNG has launched several resource projects over the years, royalties from these haven’t become a big contributor, adding at best 4% to total provincial revenue. Own-source revenue collection generated 9% of all provincial revenue. No province reported receiving any dividends in 2022 and bookmaker revenue contributed only 1% of total provincial revenue.

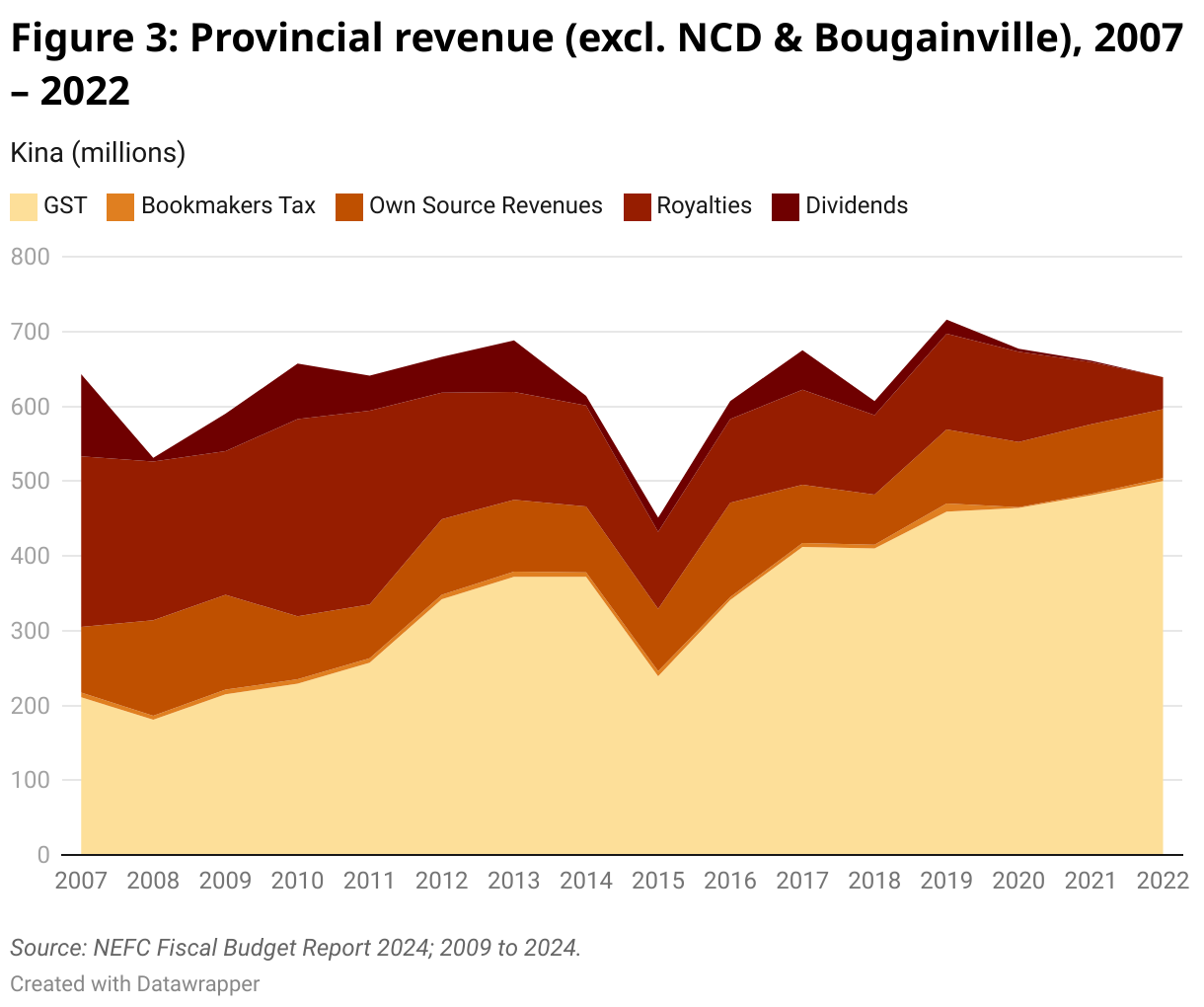

Provincial revenue also hasn’t performed strongly over time. Excluding the NCD and Bougainville, for which data is not available in some years, provincial real revenue has fallen since its peak in 2019. By 2022, real revenue at K640 million was similar to the 2007 level (K643.3 million). PNG’s resource boom (lasting from 2003 to 2013) explains the steady increase in provincial revenue from 2008 to 2013. The sharp fall in real revenue in 2015 reflects a fall in commodity prices and a drought resulting in a fall in consumption, which led to declines in royalties, dividends, and GST revenue. The fall in revenue in 2018 was caused by the Southern Highlands earthquake which saw a contraction in the extractive sector and led to a fall in dividends, royalties and own-source revenue. Provincial real revenue then recovered in 2019, before falling during the pandemic years and afterwards.

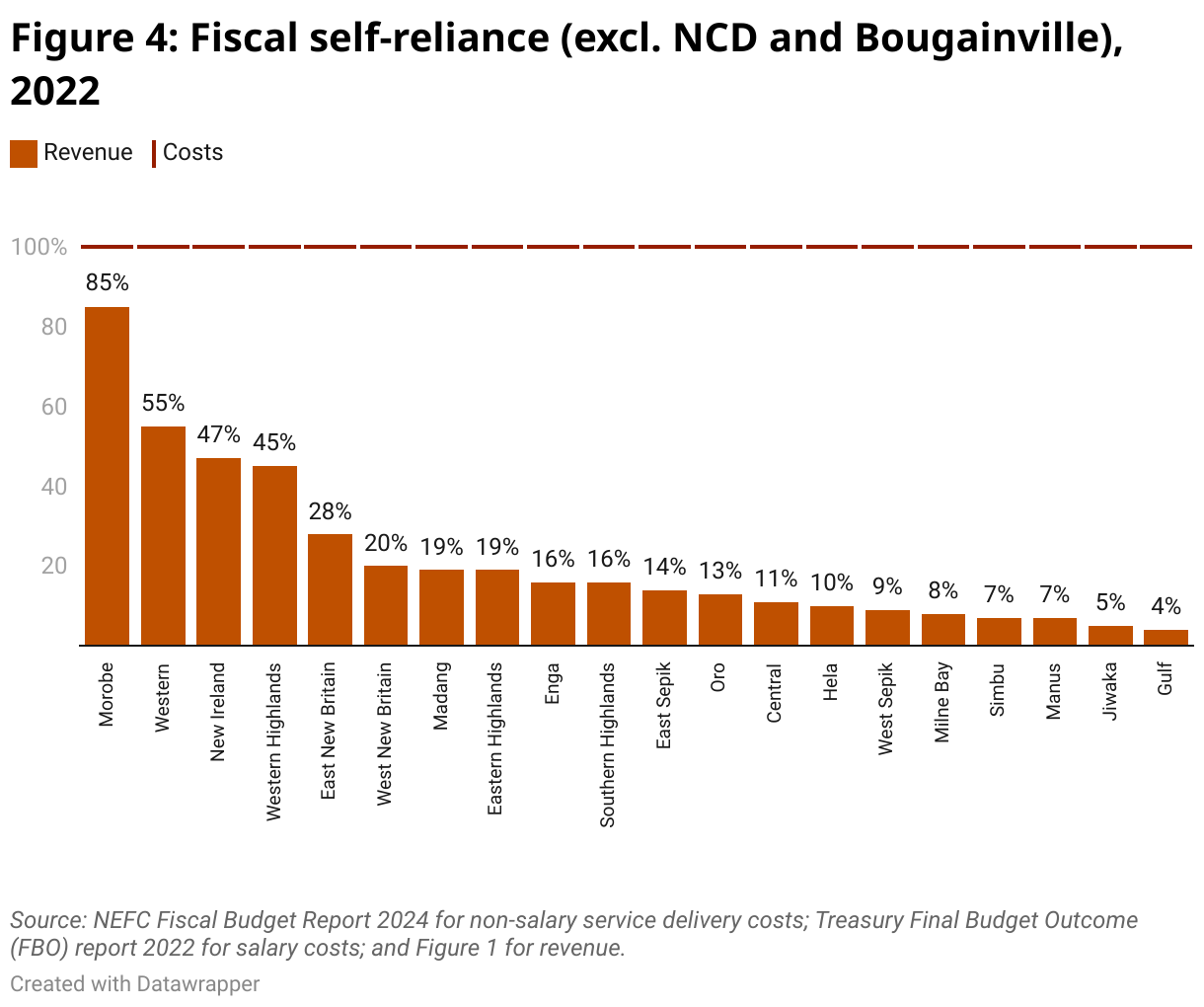

Stagnant revenues over time have reduced most provinces’ ability to become fiscally self-reliant — that is, their ability to fully finance operational costs such as staff salaries and service delivery costs. As things stand, the central government pays provincial salaries directly, but many provinces want more fiscal autonomy and responsibility. However, as shown in the chart below, no province in 2022 would have been able to meet all its operational costs (NCD and Bougainville are not part of the Intergovernmental Financing Arrangements meaning they report costs differently). Only Morobe and Western generated enough revenue to cover more than half of their operational costs, while the other 18 remained heavily dependent on transfers from the national government.

Assessing the levels of revenue raised in the provinces is important given that three provinces — Enga, East New Britain, and New Ireland — are working towards greater autonomy and have asked for more revenue-raising powers. However, even if all GST and bookmaker’s tax were remitted (instead of the current 60% and 40% respectively) in 2022, only Morobe of all the provinces (again excluding NCD and Bougainville) would be able to meet its operational costs. The rest would still be reliant on transfers from the national government. More work needs to be done to increase provincial revenue bases before progress can be made on autonomy.

In summary, revenue stagnation over time has eroded the capacity of many of PNG’s provinces to meet spending needs, increasing their reliance on the national government. In addition, provincial revenue has been inequitably distributed because provinces with the greatest level of economic activity, including resource projects, have inevitably raised more revenue. GST has grown to become the most important contributor to provincial revenue and most provinces lack a diversified revenue base, raising the risk of revenue collapse if an economic shock affects consumption patterns, as the drought did in 2015.

The Papua New Guinea’s fiscal decentralisation: A way forward report is available on the Lowy Institute website. This report is part of the Lowy Institute’s Pacific Fellow Project, funded by the Foundation for Development Cooperation (FDC), and was undertaken while the author was the inaugural FDC Pacific Fellow at the Lowy Institute.

This is the first blog in a three-part series on fiscal decentralisation.

Data from the three blogs is available at the PNG Budget Database.

Very informative information.

Excellent piece of data and evidence on the disparity across sub-nationaal levels.

A rethink of intergovernmental financing is critical.

Funding formula needs to be reviewed.

Can I get copy of your report?

Report link: https://www.lowyinstitute.org/publications/papua-new-guinea-s-fiscal-decentralisation-way-forward

thankyou for such informative note

Very informative giving the public a good understanding of Govt’s revenue generation avenues. I think it’s equally important to hold departmental heads (spenders) accountable. Provinces must be tasked to improve their internal revenue collection. They must create business entities and invest in major projects and business ventures for a good ROI.

I have been busy working on internal revenue raising opportunities provided by law for 2 LLGs in Oro Province. It is apparent in my view that manpower capacity shortfalls is a very serious problem with LLGs. This is further compounded by Provincial Governments who themselves fail to understand that they have internal revenue raising powers allowed under the Organic Law on Provincial and LLGs. The Department of Provincial Government Affairs has miserably failed the government in enabling the provinces via the OLLIPAC internal Provisions. But of course internal streams are occurring on provincial merits.

Very insightful piece. Coupled with NEFC’s Scorecard should invoke provinces to reassess their revenue raising capacities and options to generate aggressivly so that the most basic services can be internally supported when needed as deserved by the people. The provincial SEZs as an intervention should support Provincial revenue collection as well, if managed well.

very informative. Resource rich province’s seems to be worse affected. need to revisit laws to give back what provinces deserve.

Thank you for the insight into our provincial economic growth and management..

Very good commentary

A very good piece

very informative.

Powerful Bro, very informative and thankyou.