Many, but not all, developing countries have experienced a loss of foreign exchange reserves as a result of the pandemic. The IMF has reported that developing countries outside of Asia lost USD95 billion in reserves in 2020. This is hardly surprising given the disruption of COVID-19 to trade and tourism. What is more surprising perhaps is that developing countries in Asia have actually increased their reserves (by USD180 billion).

Neither the increases nor the reductions are huge. Based on World Bank data, the USD180 billion increase is only about 4% of total reserves of developing countries in Asia in 2019, while the USD95 billion reduction is only 3% for developing countries outside Asia.

One reason for the increase in Asia, and why the fall outside of Asia hasn’t been larger, might be risk aversion: things have been bad the last two years, but governments and central banks might be worried that they could get worse.

How are foreign reserves tracking in the Pacific?

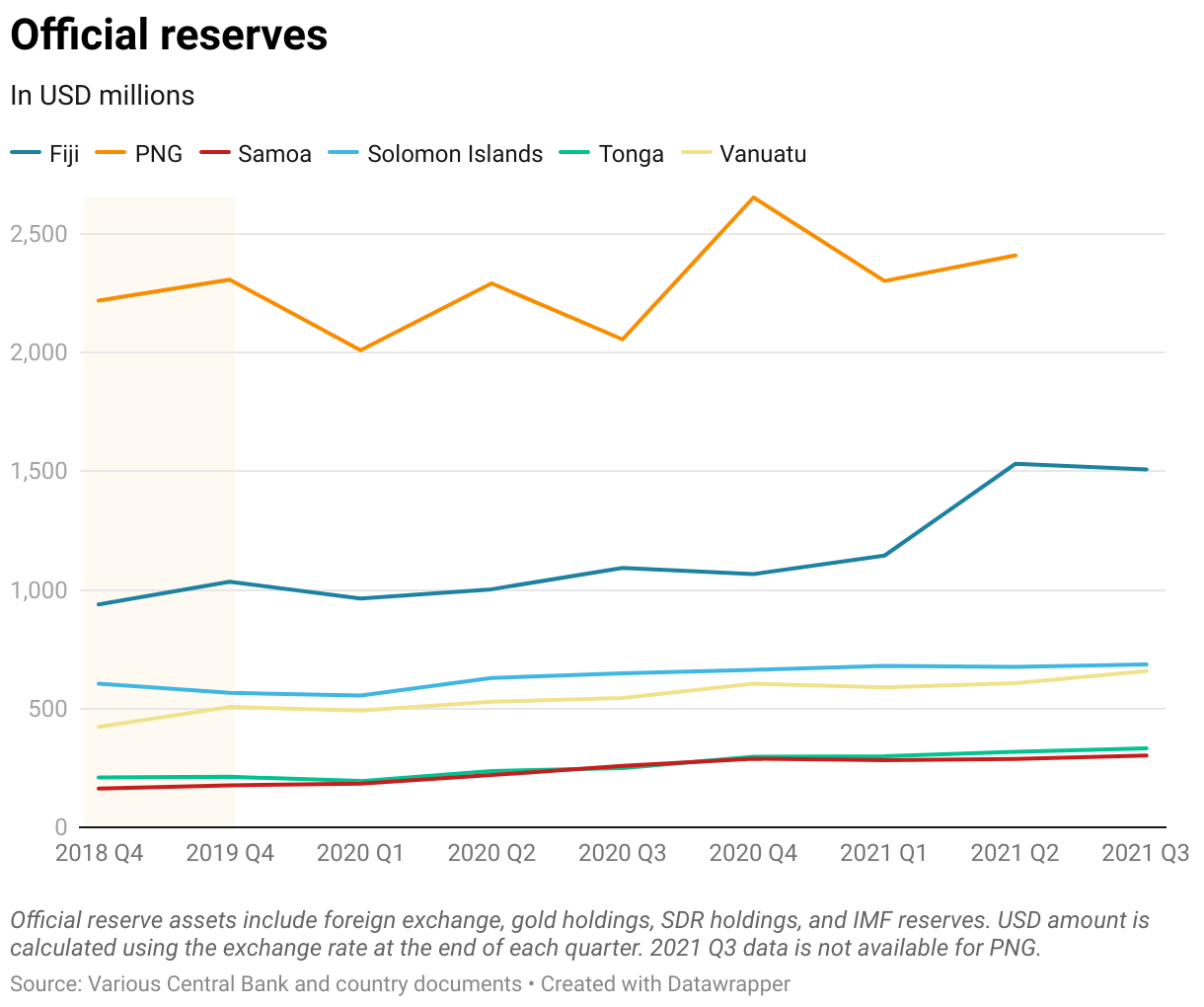

From 2019 Q4 to 2021 Q3, official reserves for Fiji, Samoa, Solomon Islands, Tonga and Vanuatu all increased by more than 20%, with Samoa’s increasing by 71%. PNG’s reserves also increased, but by much less, just 4% from 2019 Q4 to 2021 Q2. The average increase across the six economies is 34% (that is to Q2, since Q3 data is not available for PNG).

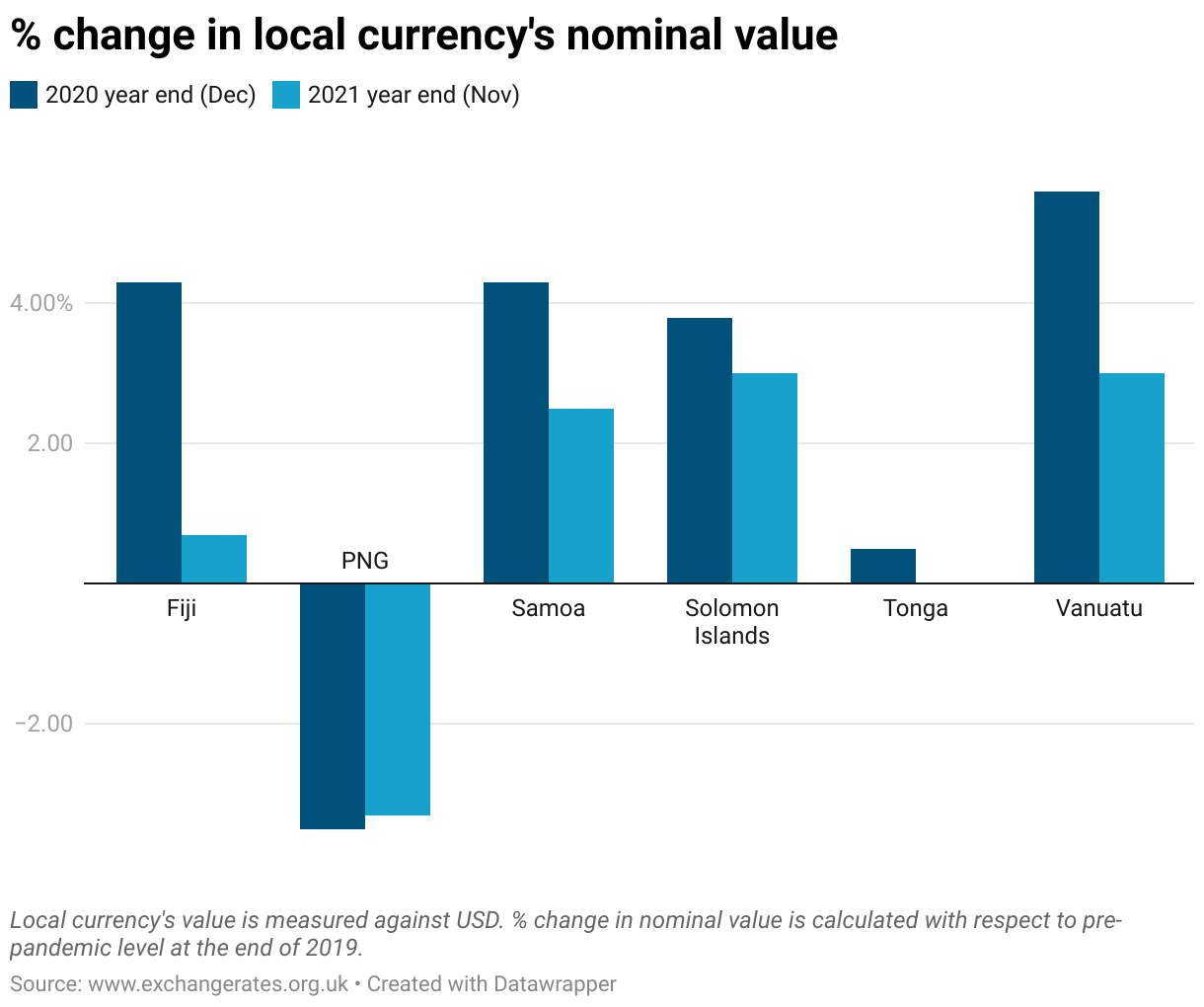

In addition, most Pacific currencies have actually appreciated slightly during the pandemic against the USD. These currencies are set by government, and the appreciation is likely caused by cross-currency movement (of other currencies in these countries’ baskets, against the USD). The PNG kina fell only slightly in 2020, and not at all in 2021.

Why are the Pacific countries facing such a comfortable external position? It’s a surprising result given the reliance of these economies on tourism (Fiji, Samoa, Vanuatu) which has disappeared, seasonal labour (Samoa, Vanuatu) which has fallen, and commodity exports (PNG, Solomon Islands) which have seen price falls.

We should start with aid, since the Pacific is the most aid-dependent region in the world. Major donors such as Australia and the multilaterals have stepped up with special support packages (both aid and non-concessional) during COVID-19. The additional Special Drawing Rights (SDR) allocation from the IMF would also have helped, though the amount is relatively small, less than 10% of pre-COVID reserves in these countries. PNG, Fiji, Samoa and Tonga have also all benefited from signing onto the Debt Service Suspension Initiative.

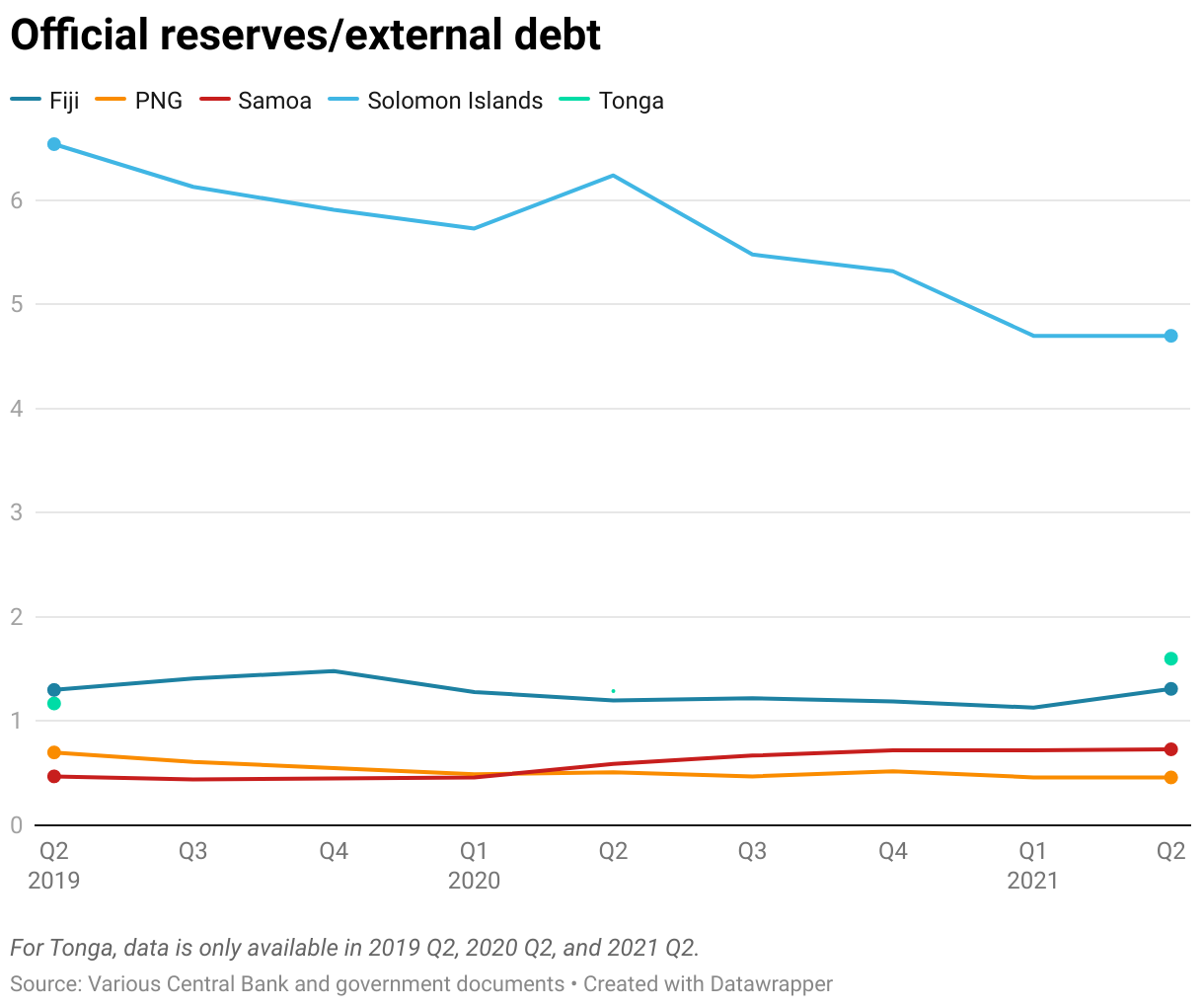

To the extent that the build-up in reserves is debt-financed, there would be an increased risk of debt crisis. Yet official reserves to external government debt increased from 2019 Q2 to 2021 Q2 in Fiji, Samoa and Tonga, meaning these countries have become more capable of finding the foreign exchange to repay their debts. Solomon Islands and PNG, on the other hand, saw decreases in official reserves relative to external debt. This is not a problem for Solomon Islands, as the ratio remains the highest among all five countries. And for PNG, most of the debt incurred has been either highly concessional or very cheap.

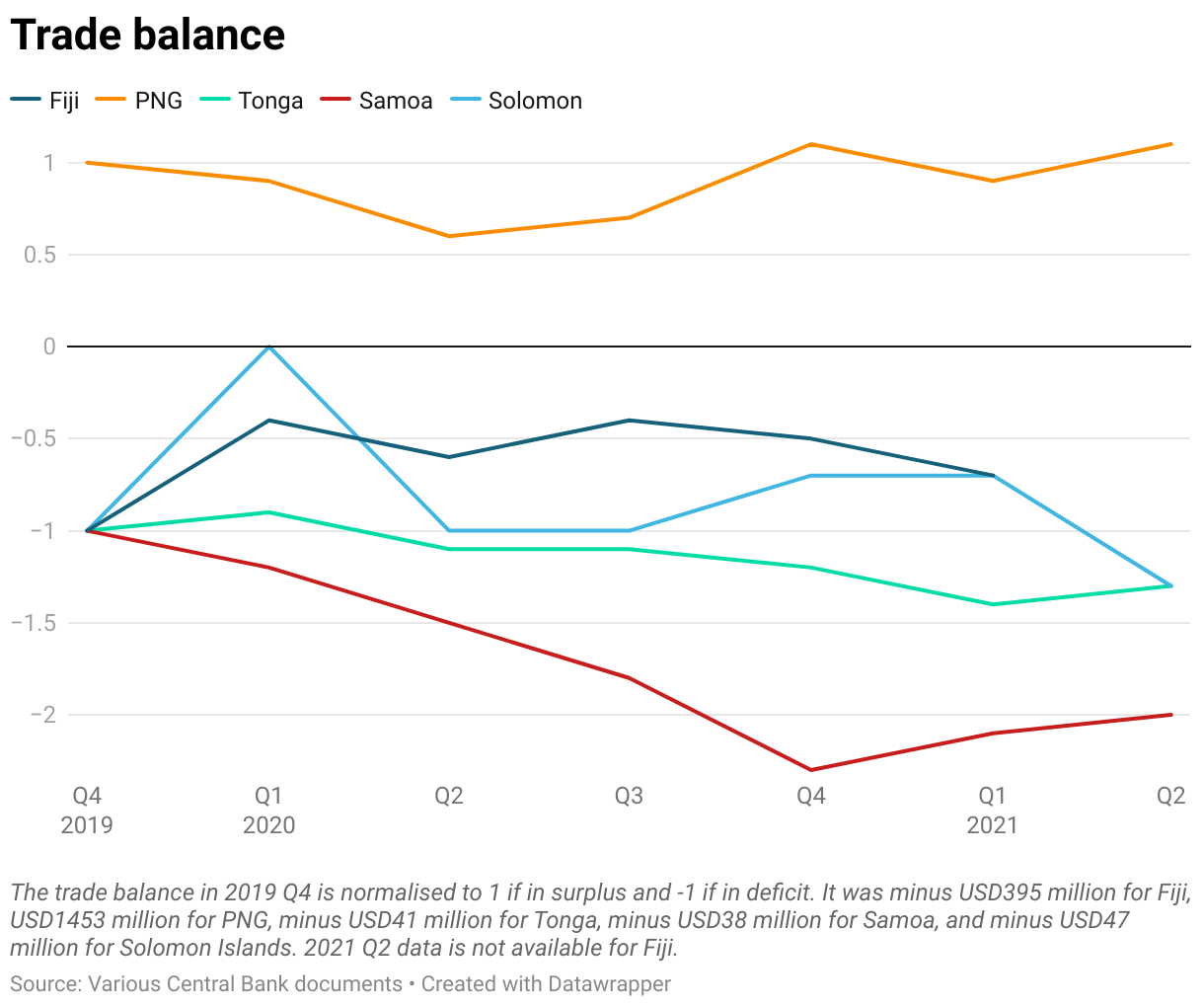

Surprisingly, trade balances in the Pacific countries have not deteriorated that much. Though Fiji and Samoa in particular are earning much less from tourism as compared to their pre-COVID levels, their imports have also dropped. Only Samoa’s trade balance has significantly worsened. PNG’s massive trade surplus fell at the beginning of 2020 due to falling commodity exports, but it recovered with the rebound in commodity prices and fall in imports.

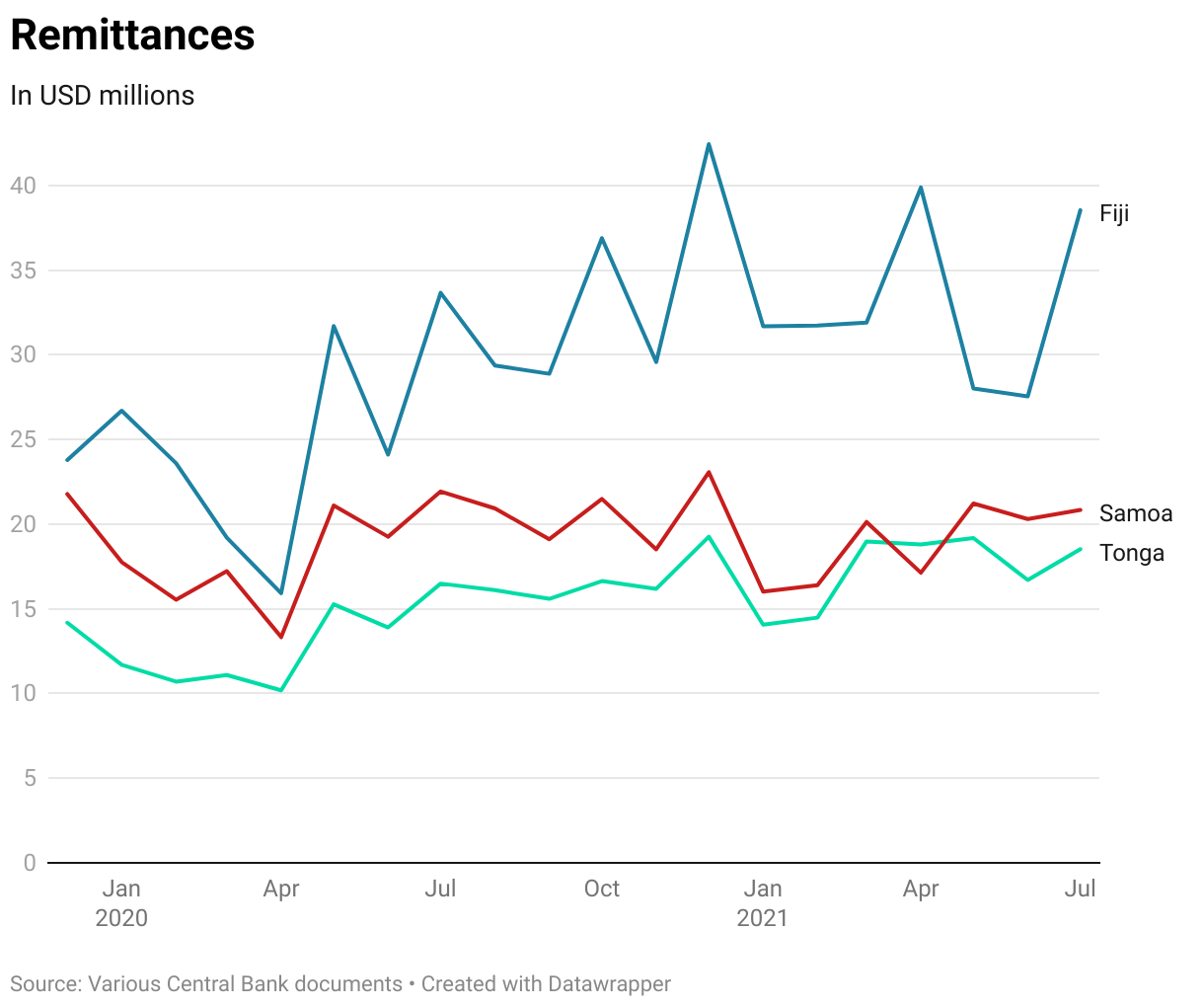

As explained in a previous blog, remittances have defied the odds and increased during the pandemic. As we’ve cautioned before, it is unclear whether reported or total remittances have increased. Even if it is the former, this would make it more likely that remittances end up with the central bank.

There are also individual country-specific factors. PNG continues to ration foreign exchange to protect its reserves. And Vanuatu’s citizenship program has continued to boom.

Overall, whatever other economic problems the Pacific faces, a looming balance of payments crisis is not one of them.