In recent years, PNG has been running record deficits. In 2019, even before COVID-19, the budget deficit was already 5% of GDP. COVID-19 has understandably made things worse. The deficit reached 8.6% in 2020 and 7.1% of GDP this year. Borrowing more during a pandemic makes sense, but it cannot be sustained.

It was understandable, indeed commendable, that the PNG government therefore put reducing the deficit at the centre of their 2022 budget, brought down last week. Indeed, it promised to go further. Perhaps taking his cue from Australian politics, the Treasurer, Mr Ian Ling-Stuckey, undertook to eliminate the deficit by 2027, and to reduce it every year between now and then.

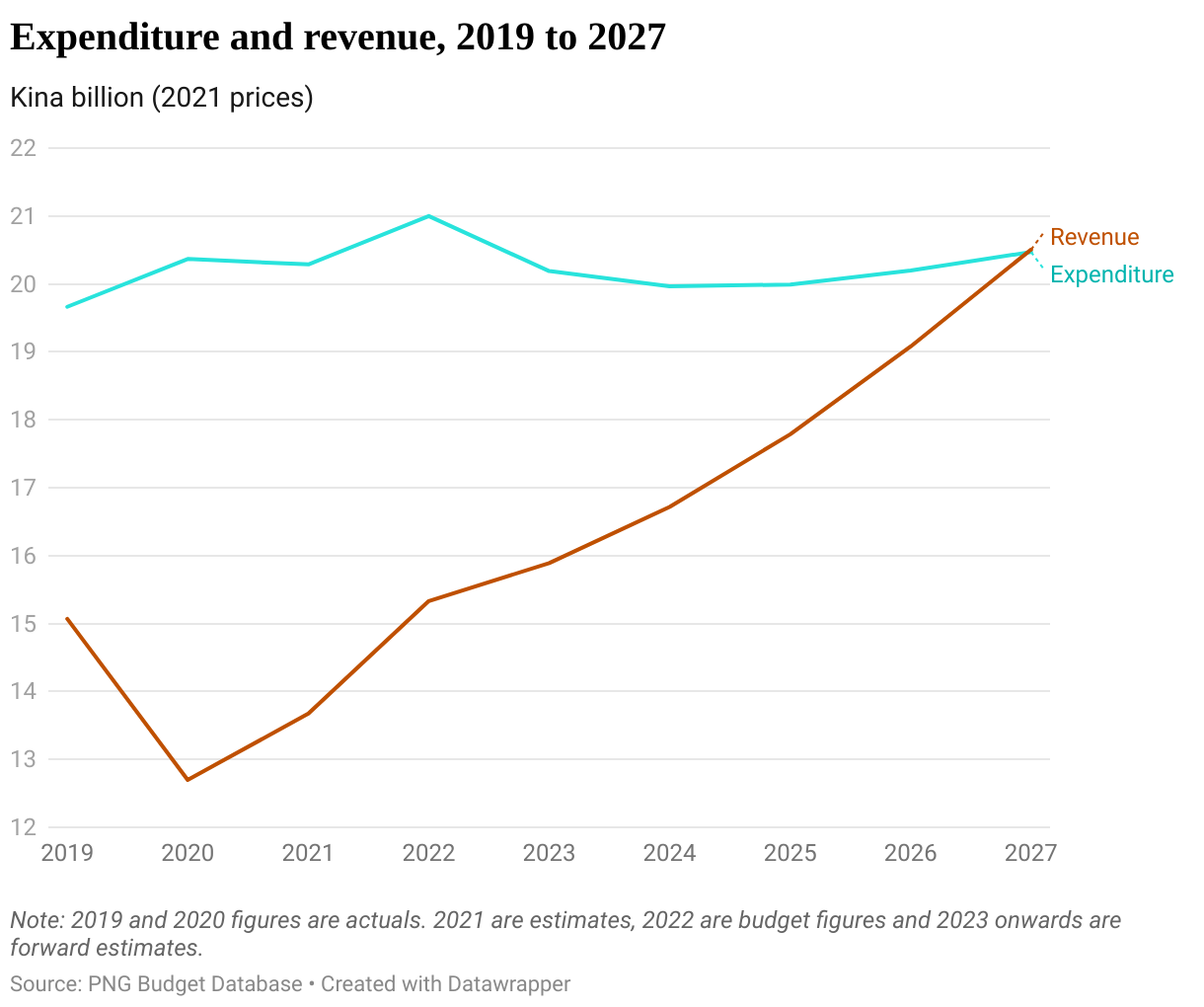

How is PNG going to achieve this? With strong revenue growth and tight constraints on expenditure. As the graph below shows, adjusting for inflation, expenditure in 2027 is budgeted to be no higher than in the current year. Revenue, however, is projected to climb rapidly, growing at an average of 7% a year in real terms. The result is an ever narrowing gap between expenditure and revenue, implying less borrowing and a lower deficit every year.

On the revenue side, much attention has been given to the controversial levies on the Bank of the South Pacific and Digicel, which the Prime Minister himself apparently deferred this week until after the election. Much more could and should be said about these levies, but there are relatively small in the scheme of things, coming to just 0.3% of GDP for 2022. More important are two other factors that have not got the same attention.

First, on the back of stronger commodity prices, the reopening of Porgera and the maturing of the PNG LNG project, a recovery in resource sector revenue is projected, from a historic low of just 3% of resource GDP in 2020 to 10% in 2027, still below the historical average of 15%, but an increase of 1% of GDP

Second, a recovery in non-resource revenue is projected from 16% of non-resource GDP in 2020 to 19% in 2027, mainly on the back of improved administration. This is an ambitious objective. Taxes on goods and services (mainly GST) are budgeted to grow at almost 10% a year in real terms between 2021 and 2027, more than twice as fast as the projected non-resource GDP growth rate. A new Goods and Service Tax Monitoring System and Tax Administration System are both scheduled to be rolled out in 2022, so we soon should have an idea of whether these new tools are up to the job.

On the expenditure side, there are tight constraints on all aspects of the budget, with both the salary bill and the development budget falling by 2-3% after inflation between 2021 and 2027.

Aggregate expenditure is budgeted to grow next year (2022) by 3.5% after inflation. About half of this is election funding itself, but there are also increases in education, infrastructure, funding to combat violence against women, and, especially, health, all funded in part by the modest increase in aggregate spending and in part by salary savings. Whether whoever wins the election in 2022 will be prepared to start on the task of cutting expenditure is a big unknown.

The government is perhaps at last getting on top of the salary bill, which grew explosively between 2013 and 2018 (by 43% after inflation), a period in which revenue growth was anaemic. But the salary bill in 2020 was only 3% more than that in 2018, again adjusting for inflation. Can the government continue to keep the lid on salaries, especially in an election year?

Perhaps the biggest question about the budget is its economic growth projections. In the five years before the pandemic, 2014 to 2019, real non-resource GDP grew on average only by 0.9% a year. The budget projects this to accelerate to an average of 4.6% from 2022 to 2027. How, especially if government spending is being restrained? The main drag to growth over most of the last decade has come from the rationing of foreign exchange and an overvalued exchange rate. Without tackling the foreign exchange regime, can PNG accelerate its growth?

PNG has been unable in the past to sustain a balanced budget. And given the country’s development needs, and the availability of cheap financing from overseas, it is hardly credible to commit to not borrowing in the distant future. That said, PNG does need to borrow less, does need to restrain expenditure, does need to increase revenue, and, most of all, does need to increase economic growth. The 2022 budget aspires to take PNG in the right direction. Whether its aspirations can be converted into reality is a much more difficult question to answer.

The PNG Budget Database has been updated to reflect the 2022 budget. All data used in this blog available in this spreadsheet.

Thank You Kelly Samof and Stephen Howes. This article is outstanding, it gave me deep insights in examining the extent to which the 2021 PNG budget met its projected revenue targets and the reasons for shortfalls.

Congratulations Kelly and Professor Stephen Howes for a comprehensive study on the 2022 budget

Honest Professionals always give a true picture of the subject of discussion, in this case the 2022 PNG Budget.

Interpretation or understanding of the subject (2022 PNG Budget) would be influenced by any Political Affiliation, I would think.

That is why this article is interesting.

I am not an Economist, so have no idea regarding the issue.

From this article, I would conclude that as always, the theory behind the PNG 2022 Budget is good, however, we have to wait for the implementation.

Great article!